Download this article as a PDF.

The 2024 Federal Budget, tabled on April 16, 2024, provides a mix of expected measures and a few surprises. In line with the announcements leading up to Budget Day, Budget 2024 outlines a multitude of measures targeted at housing affordability and the cost of living. The big question was how the government was going to pay for those measures. Budget 2024 delivers the answer with an increase to capital gains inclusion rates.

Fiscal Outlook

Budget 2024 projects deficits of $40.0B for 2023-24; $39.8B for 2024-25; and $38.9B for 2025-26. As a percentage of Gross Domestic Product (GDP), the federal debt is expected to be 42.1%, 41.9%, and 41.5% for those years, respectively.

Four Key Takeaways from Budget 2024

- Increased capital gains inclusion rate

- Expanded tax shelter on the sale of a business

- New and ongoing housing affordability measures

- Updates to previously proposed changes to the Alternative Minimum Tax

Quick Facts:

- No change to personal or corporate income tax rates.

- Capital gains inclusion rate increased to 66.67%.

- No change to the principal residence exemption.

- No wealth tax introduced.

- Multiple housing and affordability measures.

- More changes to the AMT.

Changes to the Capital Gains Inclusion Rate

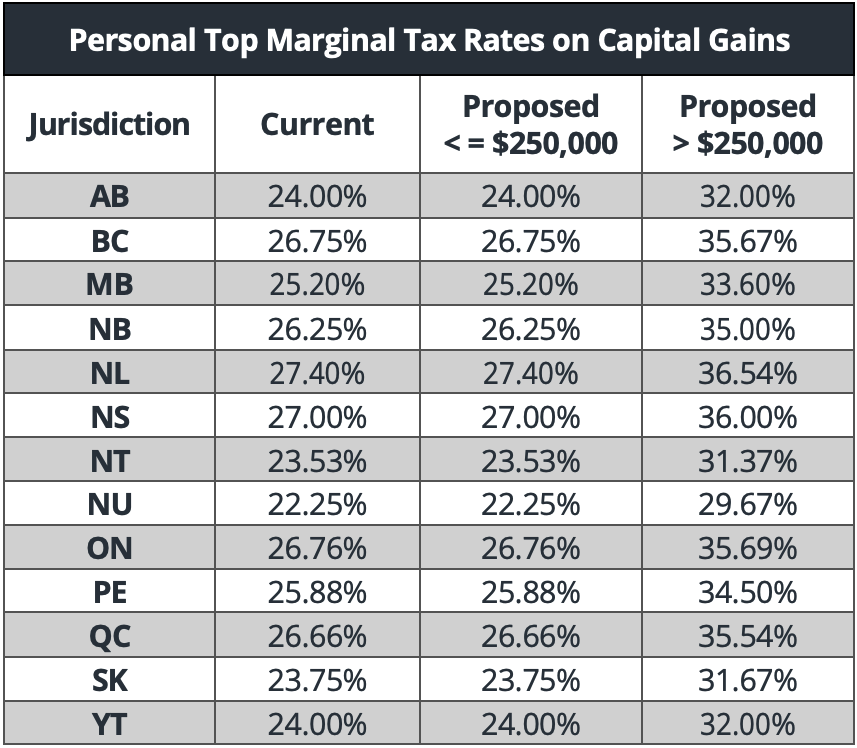

Since 2000, Canadian taxpayers have been required to include 50% of realized capital gains in their taxable income. The proportion of a realized capital gain, which must be included in taxable income, is commonly referred to as the capital gains inclusion rate. Budget 2024 has proposed an increase to the capital gains inclusion rate from 50% to 66.67% for corporations and trusts. This increased capital gains inclusion rate would also apply to individuals with realized capital gains that exceed $250,000 in the tax year. Budget 2024 states the enhanced capital gains inclusion rate would be effective June 25, 2024. Budget 2024 also provided information on specific items that will not be impacted by the proposed increase in the capital gains inclusion rates, including:

- The Principal Residence Exemption;

- Capital gains earned in registered accounts such as RRSP, RRIF, TFSA, FHSA, or RESPs; and

- Pension income or the capital gains earned by registered pension plans.

Budget 2024 states that capital gains realized prior to June 25, 2024, will have the 50% inclusion rate apply. Capital gains realized on or after June 25, 2024, would be subject to the 66.67% inclusion rate. It does not appear that the $250,000 threshold will be pro-rated for 2024, meaning the full $250,000 threshold will be available for capital gains realized on or after June 25, 2024. Budget 2024 estimates that this tax measure will add $19.4B to federal revenues over a five-year period starting in 2024. While no specific legislation regarding this proposal has been provided at this point, Budget 2024 has stated that “additional design details will be released in the coming months.”

Expanded Tax Shelter on the Sale of a Business

Lifetime Capital Gains Exemption:

The Lifetime Capital Gains Exemption (LCGE) is a tax provision which allows individuals to shelter a portion of the capital gain realized on the disposition of Qualified Small Business Corporation Shares (QSBC Shares) and Qualified Farm or Fishing Property.

The amount of capital gains that can be sheltered from tax in relation to the disposition of these specific types of assets is limited to the LCGE. Currently, the LCGE is $1,016,836. This limit has historically been indexed to inflation on an annual basis.

Budget 2024 proposes to increase the LCGE to $1.25M. This increased limit would apply to dispositions that occur on or after June 25, 2024, and would be indexed to inflation starting in 2026.

Canadian Entrepreneurs’ Incentive:

Budget 2024 introduces the Canadian Entrepreneurs’ Incentive. This measure would provide a reduced rate on capital gains arising from the disposition of qualifying shares, up to a lifetime maximum of $2M. Where the conditions are met, the capital gains inclusion rate would be one-third (33.33%), instead of the two-thirds (66.67%) proposed in Budget 2024. This measure would effectively cut the tax rate on capital gains that qualify in half, starting for dispositions occurring on or after January 1, 2025.

The $2M lifetime limit is phased in over time. The first $200,000 will become available in 2025, and an additional $200,000 will be added to the limit annually until 2034.

To qualify for the Canadian Entrepreneurs’ Incentive, both the shares being sold and the individual shareholder must meet certain criteria. The criteria for shares resemble those for the LCGE: they are shares of a small business corporation at the time of disposition, the corporation is a Canadian-controlled private corporation at all relevant times, and more than 50% of the corporation’s assets were used primarily in an active business carried on in Canada throughout the 24 months preceding the disposition. However, professional services corporations, corporations that primarily derive value from the reputation and skill of a single or several employees, consulting and personal care services businesses, and businesses operating in certain industries – financial, insurance, real estate, food and accommodation, arts, recreation, and entertainment – do not qualify for this incentive. In all cases, the shares must be disposed of for fair market value.

The individual looking to claim the Canadian Entrepreneurs’ Incentive must also have:

- Invested in the corporation when it was first capitalized (i.e., a founder);

- Held shares for at least 5 years prior to disposition;

- Held shares representing more than 10% of the votes and value of the corporation throughout the ownership period; and

- Been actively engaged in the business on a regular, continuous, and substantial basis throughout the 5 years preceding the disposition.

The proposed $250,000 threshold for the capital gains inclusion rate discussed above applies in addition to the Canadian Entrepreneurs’ Incentive, as does the LCGE. In other words, for qualifying dispositions, the first $1.25M in capital gains would be sheltered by the LCGE, and then one-third of the next $2M in capital gains, half of the next $250,000 in capital gains, and two-thirds of the remaining gains would be included in income.

Housing Affordability

Increasing housing affordability is one of Budget 2024’s main areas of focus, particularly for first-time home buyers. Budget 2024 introduces a number of measures aimed at addressing the housing crisis.

Enhancements to the Home Buyer’s Plan:

The Home Buyer’s Plan (HBP) is a program that allows eligible home buyers to withdraw from their Registered Retirement Savings Plan (RRSP) to fund a home purchase. Under the HBP, the withdrawal is not taxable, provided it is repaid into the RRSP over a period of 15 years, beginning in the second year following the year of the withdrawal. Budget 2024 proposes two enhancements to the HBP:

- Increasing the Withdrawal Limit: Budget 2024 proposes increasing the maximum HBP withdrawal from $35,000 to $60,000. This measure would apply to withdrawals made after April 16, 2024.

- Temporary Repayment Deferral: Budget 2024 also proposes temporarily deferring the 15-year prepayment schedule by an additional three years, to begin five years after the year in which the withdrawal was made. This measure would apply to withdrawals between January 1, 2022, and December 31, 2025.

Increased Amortization on Newly Built Homes:

Budget 2024 proposes to amend the Canadian Mortgage Charter and change the mortgage insurance rules to extend insured mortgage amortizations for first-time home buyers purchasing new builds to 30 years, up from the current 25-year maximum. These new insured mortgages are to become available to first-time homebuyers beginning on August 1, 2024. The government has indicated that it will consider allowing 30-year insured mortgages to become available more broadly based on supply and housing inflation.

In addition to the proposals intended to assist buyers, Budget 2024 introduces several measures aimed at increasing housing supply or reducing demand:

Secondary Suite Loan Program:

Budget 2024 proposes to launch the secondary suite loan program, which would allow homeowners to access up to $40,000 in low-interest loans to add secondary suites to their existing homes. More details will be announced in the coming months.

Other Incentives for Increasing Supply:

Budget 2024 includes a number of other proposals with the goal of creating incentives for developers, builders, and existing homeowners to create additional housing. Some are in the form of accelerated deductions, such as the Capital Cost Allowance for rental projects, the elimination of GST for certain new apartment projects, increasing the annual limit for Canada Mortgage Bonds, and low-cost loans for building apartments. Other measures target short-term rentals and underused housing.

Reducing Demand:

Budget 2024 introduces some new proposals and enhancements to existing proposals aimed at reducing housing demand. Some include a ban on foreign home buyers, anti-flipping rules, and reducing international student intake.

Updates to the Alternative Minimum Tax (AMT)

The AMT is an alternate tax calculation, done in parallel to the regular tax calculation, intended to limit taxpayers’ ability to lower their tax bill through tax preferences (i.e., exemptions, deductions and credits). AMT is paid only where it exceeds the regular tax otherwise payable.

The 2023 Federal Budget proposed significant changes that would broaden the base income on which AMT is calculated and increase the AMT rate from 15% to 20.5%. Notably, the 2023 Federal Budget proposed to include 30% of capital gains from donations of publicly listed securities in the income calculation for AMT purposes (the AMT base). Such gains are not included in income under the regular tax calculation. In addition, only 50% of non-refundable tax credits, including charitable donation credits, could be used to reduce the AMT otherwise calculated. In the consultations following these proposals, the charitable sector raised concerns that these proposed changes would disincentivize significant charitable donations because of the AMT impact.

Budget 2024 proposes additional changes to the AMT rules:

- 80% of the charitable donation tax credit could be claimed instead of the 50% proposed in the 2023 Federal Budget;

- Employee ownership trusts would be fully exempt from the AMT;

- Guaranteed Income Supplement, social assistance and workers’ compensation payments can be fully deducted;

- Certain credits that are disallowed under the AMT could be carried forward (i.e., federal political contribution tax credit, investment tax credits, and labour-sponsored funds tax credit); and

- The federal logging tax credit can be fully claimed against AMT.

Budget 2024 does not revise the 30% inclusion of capital gains on donated publicly listed securities in the AMT base.

The main thrust of the proposed 2023 AMT amendments remains unchanged: a broadened base, a higher AMT exemption amount, and an increased AMT rate. Capital gains are still proposed to be 100% included in income (the AMT base) for purposes of the AMT calculation.

Other Items:

Qualified Investments for Registered Plans:

Individuals in Canada can utilize several registered plans to facilitate various savings goals. These registered plans include accounts such as RRSPs, RRIFs, TFSAs, RESPs, RDSPs, FHSAs, etc.

Such registered plans are only able to invest in qualified investments. These qualified investments include over 40 types of assets and generally include common investments such as publicly traded securities, mutual funds, and corporate and government bonds.

Budget 2024 “invites stakeholders to provide suggestions on how the qualified investment rules could be modernized on a prospective basis to improve the clarity and coherence of the registered plans regime.”

Budget 2024 highlights several items for consideration, including:

- Whether annuities should continue to be considered qualified investments

- Whether rules for qualified investments could promote an increase in Canadian-based investments

- Whether crypto-backed assets are appropriate to be considered qualified investments

The balance of the issues highlighted by Budget 2024 appears to be aimed at further restricting the definition of “qualified investments” rather than expanding it. However, few details have been provided at this time.

Stakeholders have been invited to submit comments during the consultation period, ending July 15, 2024.

Employee Ownership Trusts

The 2023 Federal Budget introduced new rules to facilitate the use of employee ownership trusts (EOT) to purchase a business. The 2023 Fall Economic Statement then announced a temporary tax exemption on up to $10M of capital gains realized on the sale of shares to an EOT. Budget 2024 provides additional details on the exemption, including who qualifies and under what conditions. The exemption can be shared among multiple individuals, but the maximum exemption cannot exceed $10M. The exemption would apply to the qualifying disposition of shares occurring between January 2024 and December 31, 2026.