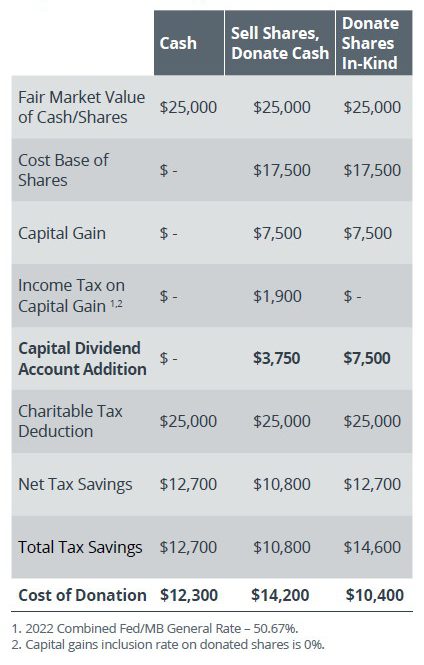

Looking at the above three scenarios, the preferred method again would be to donate shares with a fair market value of $25,000. Marija and Steve’s corporation pays no tax on the capital gain and the corporation receives the same charitable tax credit as they would have received by donating $25,000 cash. The corporation can then pay out $7,500 to Marija and Steve tax free given the Capital Dividend Account increase.

As highlighted, there are many factors to consider when contemplating a charitable donation. Please reach out to your Wellington-Altus advisor to discuss further.