Stagflation or Change: Crypto & the End of the Petrodollar

Download this article as a PDF.

“Just follow the money.” – Deep Throat, All the President’s Men

In 1972, while Carl Bernstein and Bob Woodward were investigating the break-in of the Democratic National Committee at the Watergate office complex, an informant provided the key to solving one of the most significant events in 20th century politics. The informant, known as Deep Throat, made a simple, yet provocative statement: “Just follow the money.” This would precipitate the eventual resignation of then U.S. President Richard Nixon under the infamous Watergate scandal. Yet, Nixon’s policies had already created a system shock that would bring forth a decade of stagflation – a contracting economy plagued by inflation.

Today, while the financial world continues to be consumed with talk of stagflation, we suggest that a similar system shock has been created by the Covid-19 pandemic, yet the ramifications will be much different. Still, investors may be wise to heed the words of Deep Throat and follow the money: its path forward has been intrinsically changed. We now live in an exponential age1 with an accelerating pace of change, whereby the petrodollar is being increasingly threatened by the growing prevalence of digital currencies.

Nixon’s Policies: Still Being Felt Today

Nixon may have been forced to resign over his Watergate involvement, but the consequences of his policy actions are still front and centre today. It is the 50th anniversary of what many refer to as the “Nixon shock.” At Camp David in August 1971, Nixon and his top economic advisors made the radical and momentous decision to cut the dollar loose from gold, which would fundamentally change the global monetary system. This was a departure from the Bretton Woods Agreement, birthed in Bretton Woods, New Hampshire at the end of WWII, which had pegged the U.S. dollar (USD) to the price of gold. This change was necessary, as the USD had since become overvalued. As the post WWII economy grew and the influence of European colonialism declined, the demand for USDs exploded. As a result, there were four times as many dollars in circulation than gold in reserves. This meant imports were very cheap and exports were very expensive, so the U.S. experienced their first trade deficit since the 19th century.

Nixon also shocked the world by announcing a planned visit to China, after decades of having no diplomatic relations – a move that would begin the opening up of China. In some ways, this marked the end of the golden age of capitalism. More profoundly, it began a generational shift of power from the U.S., potentially planting the seeds for the increasing dominance of China in the decades to come.

1970s: Oil Price Shock & Stagflation

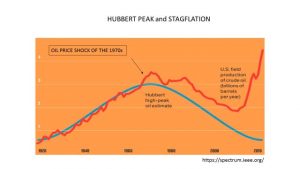

But first, the U.S. would experience a generational shift in power to the oil-developing countries. In the early 1970s, the U.S. hit the Hubbert Peak,2 whereby domestic oil production rapidly declined and the reliance on foreign oil increased. With the U.S. manufacturing base dependent on oil, the U.S. and Saudi Arabia reached an agreement to standardize the sale of crude oil based on the U.S. dollar. This implicitly tied oil to the USD. The USD would go from being explicitly backed by gold to implicitly becoming a petro-backed dollar.

Oil Price Shock of the 1970s & the Hubbert Peak

Complicating matters was the rise of resource nationalism in the Middle East, leading oil prices to spike higher.3 The sharp increase in prices of this critical factor of production would cause inflation to rapidly rise. To make matters worse, OPEC, which was formed in 1960, recognized the extent of its power and in 1973 proclaimed an oil embargo that would send oil prices quadrupling. By 1980, the price of crude was more than 10 times what it had been in 1973.

However, it wasn’t just higher oil price inputs that would prompt a period of stagflation that would last for almost a decade. There were a confluence of factors: The 1970s were wrought with slow policy responses to deregulate the natural gas industry. Regulation kept natural gas prices artificially low, meaning there was no incentive to create enough supply to allow for the substitution of natural gas for oil in western economies. The required legislative changes did not happen until the late 1970s.

The U.S. economy was also going through the early stages of structural adjustment driven by demographics when the oil shock hit. Women started to enter the work force en masse. The influence of the silent generation was beginning to wane, yet the baby boomer generation was not at the point of focusing on family formation or investing for retirement. This demographic void substantially slowed economic growth. Adding to these issues was a lack of innovation – the U.S. was quickly falling behind Japan.

2021: Not Reminiscent of Stagflation in the 1970s

Fast forward to today, and – to be clear – the global economy is not going through a repeat 1970s stagflation adjustment period. Yes, the Covid-19 pandemic has created a shock to the global system and an adjustment period will be needed, but stagflation it is not.

First and foremost, there is no parallel to the oil price shocks of the 1970s. While the move to a green economy may be commodity intensive, which may act as the catalyst for a commodities super cycle, just as the urbanization of China was a few decades ago, to suggest this is equivalent to the 1970s oil shock is simply incorrect. In fact, we now see the world’s second largest economy, China, entering a dangerous period of slowing growth in which its previous modus operandi is no longer able to support the growth touted over decades. The recent meltdown of Evergrande, China’s second biggest property company, suggests that its debt-ridden practices are no longer sustainable. Could this be China’s Lehman Brothers moment?4 Our rebuttal is a resounding no!

Current inflationary pressures caused by bottlenecks in the supply chain will eventually subside. This is a classic example of forecasters taking our current situation and extrapolating linearly into the future. We have yet to see any tangible proof that the deflationary overcapacity that existed in the global economy, which took decades to build up, has been eliminated.

The 1970s versus 2021: Where is the Stagflation?

Even the demographic situation has its differences. In the 1970s, the boomer generation had not yet progressed to the point where they could substantially generate economic growth to counterbalance the fading economic effect of the silent generation as they aged. These forces are not being replicated by the millennial generation today. Instead, millennials are entering into a period akin to the baby boomers in the late 1980s – their prime earning, family formation and savings era. However, there is one caveat: when the boomers were entering into this era, the S&P 500 valuation was reasonable, interest rates were just beginning their decade decline, housing prices were within reach and global debt levels were not at extreme levels.

Most prominently, to address the market pundits who warn of stagflation due to concerns over the influx of stimulus into global economies, we suggest that not all deficits are bad5. Yes, the invocation of modern monetary theory (MMT) to finance today’s deficits are a cause of concern for many. However, increasing the money supply is not inflationary if the velocity of money is declining. We submit that Biden’s “Build Back Better” program will be critical to driving economic growth – we need fiscal stimulus to increase aggregate demand due to the scarring effects of Covid-19. The move by world leaders to support a greener economy away from fossil fuels will ultimately usher in a new era and, we suggest, a new global monetary regime.

End of the Petrodollar? The Future of Cryptocurrency

If there is a parallel between the Nixon shock of the 1970s and stagflation to today, we would submit that it will be the Covid-19 shock and the potential for a disruption by digitization. We witnessed the evolution of the USD being explicitly backed by gold to implicitly backed by oil in the 1970s and suggest that today we stand at the brink of a new transition where technology and money intersect. Will this be the end of the petrodollar?

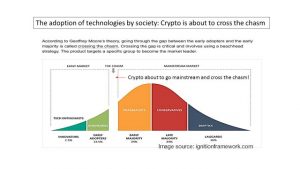

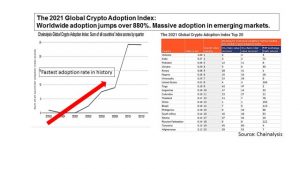

We are now living in a world where evolution can happen at an exponential pace, and the adoption of digital assets may be ready to “cross the chasm” and be accepted by the mainstream. The adoption rate of cryptocurrencies, as tracked by Chainalysis since late 2019, suggests that we are about to make this jump. One of the blockchain protocols, Bitcoin, is being viewed as a store of value, with many calling it digital gold. Ironically, cryptocurrencies reduce income inequality, and many economies are starting to take notice.

The Adoption of Cryptocurrencies: About to Cross the Chasm

El Salvador just passed a law to become the first country to make bitcoin its official legal tender. Many have dismissed this move, but from the point of view of an economy in which almost one quarter of its GDP is derived from remittances sent from citizens working in foreign countries back home, using blockchain significantly removes transaction costs and improves transaction times. As such, it should come as no surprise that the adoption of bitcoin has been dominant within emerging markets. This is eerily reminiscent of the adoption of the USD after WWII by countries that found themselves free of European colonialism.

2021 Global Crypto Adoption Rates

Investors should expect regulators to catch up to the rapid adoption taking place, with their objective being to protect investors while at the same time not stifling innovation. Most central banks globally have already accepted the current evolution. While digital currencies threaten to take away central bank control, over 85% of central banks are looking into central bank digital currencies (CBDCs).6 China is leading this charge, and reportedly the U.S. is “not close to catching up.”7

Where to for Investors?

Will Bitcoin replace the USD as the medium for global trade? We think not. However, the desire by global policymakers to achieve a “net-zero” green economy implies declining global trade in oil and a reduction in the dominance of the petrodollar. What will fill this void? Investors shouldn’t overlook the cryptocurrency space as a catalyst for this change.

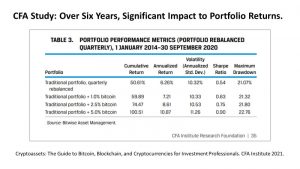

Investors who have been early to enter this space have been rewarded. A CFA study indicated that just basic exposure has historically led to a significant positive impact on long-term portfolio returns both on an absolute and risk-adjusted basis.

Crypto sits at the intersection of three forces: outdated legacy systems and industries that would benefit from an open-source environment, generational changes forced by the rise of populism which have increasingly embraced digital currencies and the need for innovation within the financial industry (consider that the banking sector hasn’t truly innovated for decades).

One protocol that may significantly disrupt the global economy is Ethereum – a decentralized, open-source blockchain platform that allows anyone to deploy decentralized applications onto it. The Ethereum protocol has a significant lead on its competition largely due to first-mover advantage, but at this point in time one can safely assume that it will continue to be the core infrastructure protocol of the internet of value.

Of course, with time, the dynamics are sure to change. However, what is indisputable is that a parallel digital economy is being built as we speak, and investors should not overlook this transition. Back in the 1990s, investors could not directly invest in the HTTP internet protocol that was about to change the world, they could only invest in applications built on top of the internet. Today, investors have the opportunity to directly own the platform and participate in its growth. Just as the first interaction of digitization that took hold in the late 1980s was met with a high degree of skepticism by the status quo, investors should not expect otherwise in this transition. However, the change we see today is happening at a faster, exponential pace.

As humans, we may not be cognitively hardwired to easily accept rapid change or exponential growth – consider how many investors fail to recognize the power of compounding when investing for retirement! This suggests that many will be surprised at how fast blockchain protocols, the building blocks of the new digital economy, will become integral in our lives. The evolution is well underway. Deep Throat reminds us to “forget the myths the media’s created…I’ll keep you in the right direction if I can, but that’s all. Just follow the money.” For investors today, stagflation is not the risk. The real risk is not following the money. Blockchain and digital monetary technologies are on the brink of mass adoption.

James E. Thorne, Ph.D.

References:

[1] “The Exponential Age will transform economics forever.” Azeem Azhar. Wired, June 2021.

[2] Given any geographical area, the rate of petroleum production trends to follow a bell-shaped curve.

[3] “The Prize: The Epic Quest for Oil, Money and Power.” Daniel Yergin. Simon and Schuster, 1990.

[4] https://www.theguardian.com/world/2021/sep/17/chinas-lehman-brothers-moment-evergrande-crisis-rattles-economy

[5] K Arrow, M Kurz, Public Investment rate of return and Optimal Fiscal Policy. 1970

[6] “Why Cryptocurrencies Are a Threat to Central Banks.” Barrons Magazine, April 30, 2021.

[7] “The U.S. Is Losing the Global Race to Decide the Future of Money and It Could Doom the Almighty Dollar,” TIME, Sept. 21, 2021.