Geopolitics, Oil Prices, and Market Volatility

Only three weeks ago, markets were enjoying what many commentators described as a “Goldilocks” environment. Interest rates were trending downward, corporate earnings were rising, and the U.S. dollar remained stable. Importantly, none of these fundamental drivers have materially changed.

However, recent geopolitical developments have introduced a degree of volatility into financial markets.

Following U.S. strikes against Iran roughly ten days ago, oil prices rose sharply amid concerns about a potential disruption to global energy supplies. The Strait of Hormuz—through which approximately one-fifth of the world’s oil supply flows—has become the focal point of investor attention. Any threat to this vital shipping route naturally reverberates through energy markets and global equities.

While the situation remains fluid, financial markets appear to be signaling that investors expect the disruption to be temporary rather than structural.

Market Reaction So Far

Let us examine what the markets are actually telling us.

Since February 27—the day before the U.S. strike on Iran—the S&P 500 has declined approximately 2.5%, falling from 6,878 to about 6,710 as of March 9. In historical terms, this represents a modest pullback rather than a meaningful correction.

Energy markets experienced a sharper reaction. West Texas Intermediate (WTI) crude oil briefly surged to approximately US$119 per barrel, reflecting immediate concerns about supply disruptions. Since then, prices have retraced to roughly US$95 per barrel.

Perhaps more telling is the signal coming from the futures market. The nine-month WTI futures contract is currently trading near US$70 per barrel, suggesting that market participants expect the current price spike to be temporary.

In other words, while geopolitical tensions have created short-term uncertainty, the market consensus appears to be that oil supply disruptions will ultimately prove manageable.

Historical Perspective

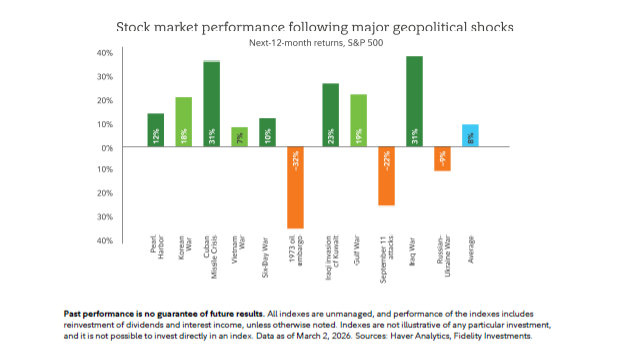

In terms of geopolitical shocks in general, history is remarkably consistent: when you line up major geopolitical events, from Pearl Harbor to the start of the Russia-Ukraine War, and look at the subsequent 12 months, average stock market returns are right around their long-term trend of around 8%.

Periods of geopolitical tension in the Middle East have historically produced similar patterns in energy markets as what we are witnessing.

A useful historical comparison is the Gulf War of 1990–1991. Prior to Iraq’s invasion of Kuwait in July 1990, oil prices were roughly US$20 per barrel. Following the invasion, fears of supply disruption drove prices sharply higher, briefly doubling to approximately US$40 per barrel.

However, once the conflict stabilized and supply concerns eased, oil prices declined rapidly. By early 1991, oil had fallen back toward US$22 per barrel, close to pre-invasion levels.

The lesson is not that every geopolitical shock resolves quickly, but rather that oil markets often react sharply in the short term and normalize once supply risks become clearer. We are of the opinion that now is the time to lighten up on energy holdings for those who may have them. We will be contacting those of you to whom this applies.

Implications for Canada

For Canada, elevated oil prices have an additional dimension.

Over the past decade, technological improvements and operational efficiencies have significantly reduced the break-even costs for Canadian oil sands producers. Today, the industry’s average break-even cost is generally estimated to be in the low-to-mid US$40 per barrel range.

For example:

- Canadian Natural Resources: estimated break-even in the low-to-mid US$40 range

- Suncor Energy: approximately US$42.90

Even with oil prices retreating from their recent peak, current levels remain highly profitable for Canadian producers.

A healthy energy sector has broader implications for the Canadian economy. Strong oil prices tend to support investment, employment, and government revenues. This strengthens overall economic conditions and reduces credit risk for financial institutions—factors that ultimately support the earnings and share prices of Canadian banks.

Short-Term Consumer Impact

While higher oil prices can benefit Canada’s resource sector, they are not without short-term consequences for consumers.

Drivers have already begun to feel the effects at the pump. Gasoline prices in the Greater Toronto Area are currently around $1.54 per litre at the time of writing. Such increases can create understandable frustration for households and businesses alike.

However, history suggests that these spikes often moderate once supply concerns stabilize.

Investment Outlook

From an investment perspective, it is important to separate short-term market volatility from longer-term economic fundamentals.

At present, the key drivers supporting markets remain intact:

- Interest rates are trending lower

- Corporate earnings remain solid

- The broader global economy continues to expand

The recent market reaction appears to be primarily a response to geopolitical uncertainty rather than a deterioration in economic fundamentals.

Financial markets have faced many similar events over time. While each situation is unique, markets have historically demonstrated a remarkable ability to absorb geopolitical shocks and refocus on underlying economic conditions.

Our Perspective

While headlines surrounding geopolitical conflict can understandably create concern, the current market reaction remains well within the range of normal volatility.

If the flow of oil through the Strait of Hormuz continues and supply disruptions remain limited—as futures markets currently suggest—energy prices should stabilize and financial markets are likely to resume focusing on the broader economic environment.

In the meantime, maintaining a disciplined, long-term investment approach remains the most effective strategy.

Final Thoughts

Periods of uncertainty are an inevitable part of investing. Market volatility can feel uncomfortable in the moment, but history repeatedly demonstrates that reacting emotionally to short-term events rarely serves investors well.

The fundamentals that supported markets just a few weeks ago remain largely intact today.

As such, our message to clients remains simple:

Keep Calm and Carry On.