Market Commentary

One thing is certain investing these days is not for the faint of heart. If that sounds familiar, it’s because it’s how I opened last month’s commentary. And it bears repeating—volatile markets are here to stay. Change is rapid, frequent, and often noisy. Information (and misinformation) gets amplified and circulated in near–real time, with very little filtering or editorial judgment. It’s no wonder even disciplined investors can lose confidence.

What makes this even more striking is that the global stock market is only about 3% below its all‑time high. Considering we’re in the midst of a large‑scale conflict in the Middle East, the disconnect between the geopolitical chaos we see in the headlines and the steadiness of financial markets is noteworthy. Energy prices are the main outlier—they’ve moved materially higher, and if sustained, could have broader economic implications. But so far, the overall market impact of the conflict has been surprisingly muted, highlighting the resilience of both the economy and financial markets.

It’s also worth pointing out that stocks have been trading in a tight range near record highs for nearly six months. Leadership in stocks has rotated, but indices have failed to move much beyond October highs. Bond yields have remained stable and credit spreads have tightened. A period of consolidation like this is typically considered a healthy reset.

Still, resiliency doesn’t mean predictability. We never know what’s around the next corner or how investors will react. Markets are complacent…until they’re not. This is exactly why we’ve spent the past several months tilting portfolios toward greater diversification and quality. During the worst of the recent selloff, our strategies fell only about half as much as their benchmarks—a clear sign that portfolios are doing what they’re designed to do.

We’ve never been more confident in our strategies.

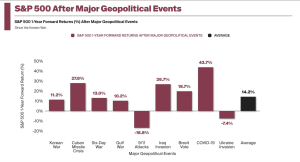

Chart of the month

It can be difficult, in the moment, to imagine how major geopolitical events could ever be positive for your portfolio—but history consistently shows that markets tend to look past these shocks. It’s not that these events don’t matter; it’s that other forces ultimately matter more to long‑term market performance.

On the accompanying chart, the two clear outliers are 9/11 and the war in Ukraine. In both cases, the events unfolded during already‑challenging economic backdrops—the unwinding of the dot‑com bubble and the global inflation shock, respectively. Those underlying conditions, not the geopolitical events themselves, were the dominant drivers of market performance.

Today, we would argue that the evolution of artificial intelligence (AI) is a more powerful force shaping economies and markets than the conflict in the Middle East. Structural shifts in productivity, corporate investment, and business models tend to outweigh even significant geopolitical noise.

Content recommendation: The case for private equity

For those who want to better understand why private equity is a valuable part of a modern diversified portfolio, here’s a comprehensive piece from KKR.

The Case for Private Equity in Individual Investor Portfolios | KKR

Portfolio strategy

Debt

Liquid fixed income

- U.S. Treasury bonds, typically a safe haven during periods of economic and geo-political stress, actually sold off as the conflict in the Middle East unfolded. Bolstering our opinion that over-indebtedness and other macro factors are a major long-term headwind for many developed nation’s bonds.

- Credit spreads remain tight as credit conditions remain healthy; however, this also means yields remain lower.

Private credit

- The widespread concerns expressed in the media seem overblown, especially amongst the high-quality managers.

- Redemptions will likely rise because of the bad press, but the fact is that defaults and write downs have been limited. No one has produced a “smoking gun” exposing rampant poor underwriting standards.

- We have improved manager and strategy quality and reduced exposure in recent months.

Equity

Public equity (stocks)

- Tech stocks seem to be suffering from fatigue; the Magnificent Seven ETF (MAGS) is basically flat over the past six months and down approximately 6% YTD.

- Last April, we began an ongoing effort to reduce concentration in mega-cap U.S. tech for better geographic and sector diversification.

- Adding to international stocks has delivered exposure to companies with lower valuations.

- Adding to active management allows for a tactical approach during these periods of leadership change.

Private equity

- Our private equity (PE) portfolio is now diversified across various strategy types (core, buyout, growth and secondaries), delivered via a handful of the world’s biggest and best private equity managers.

- We are excited to have meaningful exposure to such a high-quality private equity portfolio as we enter what could be the start of a robust PE cycle.

- PE helps diversify portfolios by owning types of companies that are not represented in the stock market. They tend to be smaller, in different industries and trade at lower valuations.

Real assets

Real estate

- Portfolios contain only minimal real estate exposure through a small allocation in Apollo Aligned Alternatives.

- Returns seem to be improving, but on balance, we see better opportunities in infrastructure.

Infrastructure

- A new investing acronym has emerged, HALO, which stands for Hard Assets Low Obsolescence. Essentially, companies that are difficult or impossible to be replaced by AI.

- Infrastructure fits the HALO narrative, but coupled with the digital infrastructure needs to power AI, we believe infrastructure is an excellent opportunity.