Market Commentary

Considering everything going on in the world right now, you’d be forgiven for thinking the stock market is in freefall. And yet, the market seems to be taking America’s latest “excursion” (President Trump’s actual words) largely in stride, with global stocks sitting just 3% below their all-time high.¹ By now, investors should be well aware that markets often move independently of negative geopolitical events and the narratives that feel most intuitive at the time.

That said, resilience doesn’t mean the ride has been smooth. Despite holding up remarkably well in the face of yet another war in the Persian Gulf, March marked the worst monthly return for global stocks since September 2022.¹ To make matters worse, so-called “safe havens” like gold and bonds also declined, dealing an added blow to investors relying on more traditional asset allocation strategies.

One area that delivered positive returns in March was our private asset portfolio. Private asset exposure is a key differentiator of our strategies. We’ve spent the better part of a decade thoughtfully building exposure to world-class private asset strategies, with the goal of improving diversification, reducing short-term drawdowns, and gaining access to sectors and businesses that are key long-term growth drivers. The payoff from this approach was evident last month, as our portfolios materially outperformed their benchmarks.

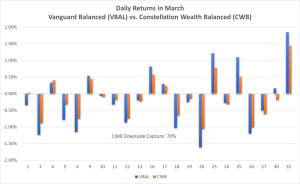

Chart of the month: Constellation Wealth Balanced Portfolio Returns in March

Our returns in March deserve a bit more attention. We believe managing risk during periods of market stress is critical for two key reasons.

First, limiting short-term losses plays a huge role in maintaining investor confidence, which in turn supports the discipline required for long-term success. Short-term losses—and the reactionary decisions that often follow—are widely recognized as some of the biggest detractors from investment outcomes. Reducing the risk of selling at the bottom is essential. At the very least, it helps everyone sleep a little better at night.

Second, math—specifically, the power of compounding. As Albert Einstein famously said, “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.” Put simply, a portfolio that falls less doesn’t need to rise as much to achieve the same overall return. That’s exactly what our portfolios accomplished in March.

On down days, our losses were meaningfully lower—we captured only 70% of the balanced benchmark (comprised of 40% bonds and 60% stocks) downside. This means when the benchmark fell by $100, portfolios only fell by $70. While we participated in a similar proportion of the upside, the compounding effect worked in our favour. As a result, Balanced portfolios outperformed their benchmark by a strong 0.78% for the month. At the peak of the sell-off, that outperformance reached as much as 2.5%. Growth portfolios showed similar behaviour, with slightly better relative performance versus their benchmark.

Content Recommendation: What’s Really Happening in Private Credit?

With so much media attention on private credit, we thought it was appropriate to provide a more thorough, informed perspective than is offered by the media

What’s Really Happening in Private Credit?

Portfolio strategy

Debt

Liquid fixed income

- U.S Treasury bonds, typically a safe haven during periods of economic and geo-political stress, regularly sold off as the conflict in the Middle East unfolded. Bolstering our opinion that over-indebtedness and other macro factors are a major long-term headwind for many developed nation’s bonds.

Private credit

- We believe redemptions are largely a function of portfolio rebalancing, as many of our peers substantially over-allocated to private credit in years past.

- The funds and the underlying assets appear to be doing exactly what they are supposed to – providing yields above traditional fixed income and limiting liquidity to protect long-term investors.

- Our allocation to private credit is small, high quality and achieving objectives. We are not concerned.

Equity

Public equity (stocks)

- It seemed everyone (ourselves included) were worried about the stock market’s concentration in tech companies.

- Tech companies have sold off considerably (Magnificent seven is down 13%) and yet global stocks are only down 3%.2

- It’s a testament to the efficacy of index investing. Sectors and companies no one was talking about a few months ago rallied massively to fill the void left by tech. I don’t recall any strategists advising to buy companies like Dow Chemical or Lyondell Basel (up 62% and 65% respectively this year) in their 2026 market outlook!

Private equity

- Delivering strong and consistent returns, helping smooth portfolio returns.

- The large, top-tier asset managers (where we are invested) seem to be the beneficiaries of the current PE cycle – they are raising more capital and achieving more successful exits.

- Success this cycle will likely depend more on manager quality and operational execution rather than market beta.

Real assets

Real estate

- Portfolios contain only minimal real estate exposure through a small allocation in Apollo Aligned Alternatives.

- Returns seem to be improving but on balance, we see better opportunities in infrastructure

Infrastructure

- Energy, defense, data centers, transportation…these are all durable, persistent growth themes globally.

- Our infrastructure investment is well-positioned to continue to benefit from these themes.

1 Vanguard Total World Stock Index Fund, VT.

2 Magnificent Seven ETF, MAGS.