The Debasement Trade Amid Geopolitical Tensions

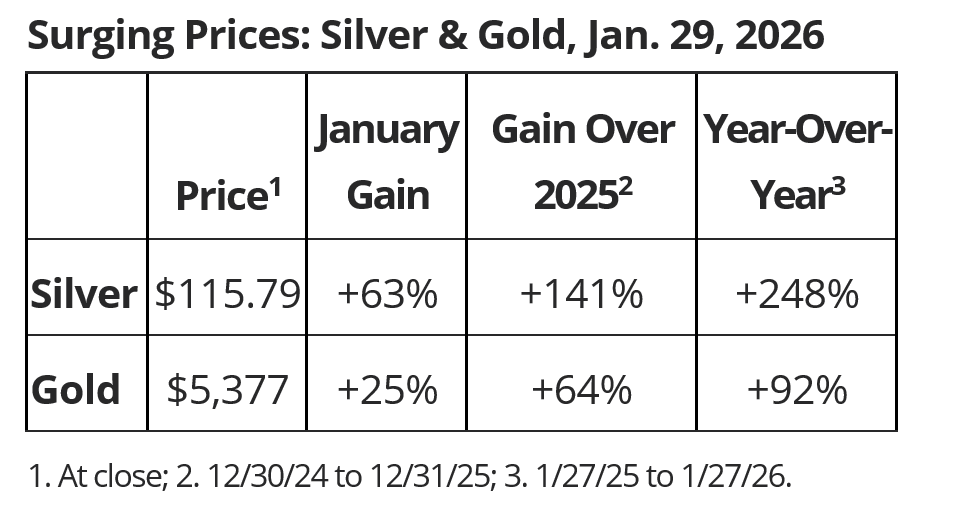

Gold and silver opened the year with substantial momentum. By the end of January, silver had surged to around $120 per ounce (intraday), up 63 percent in the month alone and up more than 248 percent year over year. Gold futures posted their largest single-day dollar gain on record, rising about $231 per ounce, while spot prices reached $5,600 (intraday), up 92 percent from a year earlier. In early February, both metals corrected sharply, retracing part of January’s rapid advance.

What was driving demand? Some market observers point to the “debasement trade”: an effort to preserve purchasing power amid monetary expansion and fiscal strain. The investment thesis is simple: when governments expand the money supply aggressively, keep interest rates below inflation or run large fiscal deficits, the real value of cash and fixed-income assets erodes. For investors worried about weakening currencies, gold and silver act as tangible assets with no sovereign liability attached. Recent developments have reinforced these concerns. In Japan, long-term government bond yields surged to record levels after the government unveiled a plan to increase spending while cutting the consumption tax in January.

Geopolitical Tension & the Commodities Imperative

Monetary concerns are only part of the story. Geopolitical tensions are reshaping capital flows and reserve strategies. Trade wars, tariffs and sanctions risks have pushed some governments to prioritize resource security, including stockpiling critical commodities. At the same time, the broader shift from global interdependence toward national self-sufficiency is strengthening demand for real assets. Since 2022, central banks including Poland, Turkey, India, China and Kazakhstan have significantly increased gold reserves partly as protection against geopolitical pressure or financial sanctions. This has raised the question: Is a commodities supercycle underway?

U.S. Dollar & Treasuries: Under Pressure

Traditional safe-haven assets are also facing scrutiny. For decades, the U.S. dollar and Treasuries were regarded globally for their stability, but this view may be changing. The dollar fell to a four-year low in January, fuelling headlines such as “How Trump Is Debasing the Dollar and Eroding U.S. Economic Dominance.” With lower interest rates and pressure for further cuts, the relative appeal of Treasuries may be diminishing. Other safe-haven currencies are also under pressure. The Japanese yen has weakened amid inflation and fiscal stimulus, leaving the Swiss franc as one of the few currencies still widely viewed as reliable.

What comes next? Given the scale and speed of gains, it’s reasonable to ask whether certain defensive trades were overextended. By historical standards, gold and silver’s early-year surge was steep. Still, the underlying drivers persist, including monetary expansion and geopolitical fragmentation. In such an environment, diversified exposure to defensive sectors, including commodities, alternative assets and resilient segments of the equity market, can help mitigate risks tied to inflation, currency erosion and geopolitical shocks.