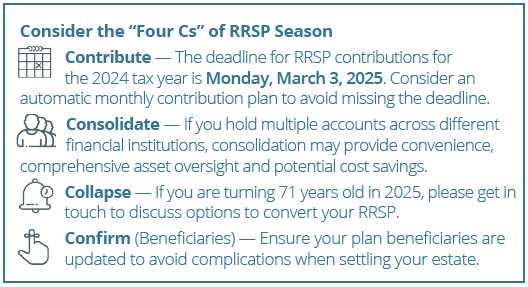

RRSP Season: Don’t Overlook the Spousal RRSP

It’s RRSP season once again! Over the decades, the federal government has eliminated many income-splitting opportunities available to taxpayers. However, if you have a spouse/common-law partner, don’t overlook the spousal Registered Retirement Savings Plan (RRSP) — a valuable opportunity to split income at retirement if your spouse will be in a lower tax bracket at that time.

A Tax Break Now…A Tax Break Later

A spousal RRSP is a plan to which you contribute on behalf of your spouse and receive a tax deduction based on your own available RRSP deduction limit. With a spousal RRSP, your spouse is the annuitant, so any funds withdrawn are considered to be the spouse’s income and must be included in their income tax return. As such, withdrawn funds will be taxed at a lower rate should your spouse pay tax at a lower rate than you. Be aware that income attribution rules may apply to a spousal RRSP: In general, if you contribute to a spousal RRSP in the current year, or two of the preceding years, some or all of any RRSP withdrawal may be taxed in your hands.

More Flexibility Than Pension Income Splitting?

A spousal RRSP may provide an enhanced income-splitting opportunity when compared to pension income splitting. Pension income splitting can only be done after reaching the age of 65 and is limited to 50 percent of eligible pension income. A spousal RRSP can begin before age 65 and the full amount of RRSP withdrawals may be included in the spouse’s tax return. However, RRSP contributions can only be made until the end of the year the taxpayer turns age 71. If you have a younger spouse, you can contribute to the spousal RRSP until the end of the year the spouse turns age 71. For any RRSP matters, please call.

A spousal RRSP may provide an enhanced income-splitting opportunity when compared to pension income splitting. Pension income splitting can only be done after reaching the age of 65 and is limited to 50 percent of eligible pension income. A spousal RRSP can begin before age 65 and the full amount of RRSP withdrawals may be included in the spouse’s tax return. However, RRSP contributions can only be made until the end of the year the taxpayer turns age 71. If you have a younger spouse, you can contribute to the spousal RRSP until the end of the year the spouse turns age 71. For any RRSP matters, please call.