Many Canadian shareholder investors (“investor”) own foreign securities. Occasionally a foreign corporation (“original corporation”) will spin-off a subsidiary or business line to its shareholders, so the subsidiary becomes a separate, publicly traded corporation (“spin-off corporation”). In this situation, the investor now owns two separate foreign securities.

By default, the receipt of the new spun-off securities is reflected as a taxable foreign dividend for Canadian tax purposes by the investor. However, in some cases, the investor can make an election so that no foreign dividend is reported, and therefore no Canadian tax applies in respect of the spin-off for the year.

The original and spin-off corporations can collectively apply to the Canada Revenue Agency (CRA) to have the spin-off transaction treated as an approved, eligible foreign spin-off if it meets certain conditions. The conditions to be approved as an eligible foreign spin-off are beyond the scope of this communication.

Where CRA has approved the foreign spin-off, section 86.1 “Foreign spin-offs” (S.86.1) in Canada’s Income Tax Act allows a Canadian resident investor to make a special election. This election allows the investor to exclude the taxable foreign dividend from income and recalculate the adjusted cost base (ACB) of the original corporation shares and the spin-off corporation shares held as a result of the spin-off. In effect, with the election, no tax is payable for the spin-off, but the future sale of the original and spun-off foreign securities may result in greater capital gains, owing to a lower cost basis.

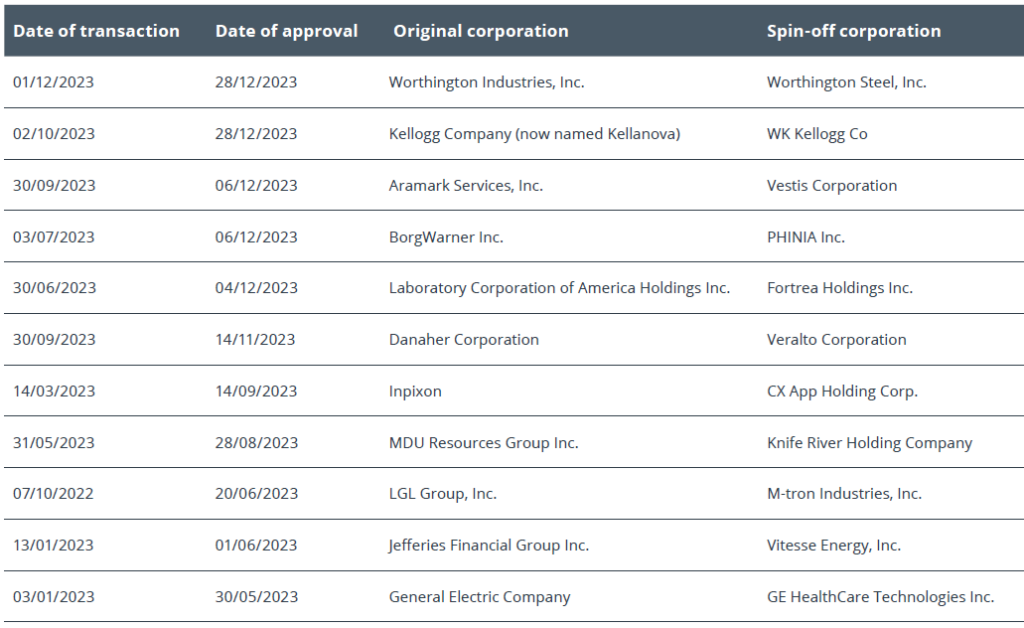

For 2023, the following foreign spin-offs were approved as eligible for S.86.1 election purposes, as of February 20, 2024: