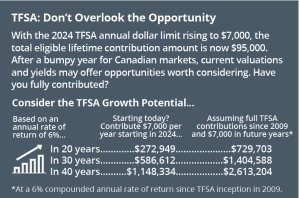

For 2024: Focus Less on the Headlines

It has been 45 years since BusinessWeek declared the “Death of Equities,” warning that rampant inflation was “destroying the stock market” and “to regard the death of equities as a near-permanent condition.”1 These dramatic prognostications haven’t subsided over time, likely because negative news is more appealing. When one news website decided to report exclusively good news for a day, it lost two-thirds of its readership 2. Our brains are hardwired to react more strongly to negative information.

As we begin a new year — and in this season of resolutions — why not focus less attention on the headlines? One reason is that negative news can skew our perceptions. An article in The Economist suggests that in recent years, opinions about the state of the economy have diverged from reality (see page 3). This has been termed a “vibecession,” where the prevailing mood is significantly more negative than the actual economic situation.3

This may not come as a great surprise — our brains aren’t meant to handle the high volume of negative news we are fed today. Just two generations ago, most of our news was delivered by local television or newspaper. In the last 20 years, the internet made global news more ubiquitous. With the unveiling of the iPhone in 2007, news is now available at our fingertips 24/7; and in the last decade, social media has continued its proliferation.

From an investing perspective, negative news may create undue concern and sometimes compel investors to make hasty decisions. We all know the oft-counterproductive behaviours, such as trying to sell before a market downturn or, worse still, abandoning stocks during a downturn, which deprives the investor of the ability to eventually recover. While these appear to be intuitive actions in the face of uncertainty, they can derail the investing journey.

Today, there has been no shortage of negative news. Many are understandably struggling with an increasing cost of living and the impact of higher interest rates. Global economies remain highly indebted, economic conditions at home are softening and we’re still likely to see the lagging effects of the rate likes. As advisors, we are focused on managing portfolios to navigate the challenges that come with the changing times.

However, it’s worth repeating: we’ve experienced these challenges, and many others, before. Recessions, financial crises, inflation, stagflation, even global conflict and war — the returns since the “Death of Equities” include all of these terrible things. And, yet, we’ve persevered and forged ahead. Consider that an investment of $100,000 in the S&P 500 Index during that period of maximum pessimism 45 years ago would have yielded around $8 million today.4 Decades later, in 2019, the publishers would sheepishly admit: “The S&P 500 return since its 1982 low has been 7,000 percent. Not bad for a corpse.”5 Yet, participating in this growth required having confidence that brighter days lay ahead.

As we begin another year, look forward to those brighter days ahead. We would like to take this opportunity to express our gratitude for entrusting us with your wealth management. Wishing you and your loved ones an abundance of health, happiness and prosperity in 2024.

1. BusinessWeek Aug. 13, 1979;

2https://www.bbc.com/future/article/20200512-howthe-news-changes-the-way-we-think-and-behave;

3. https://www.economist.com/graphicdetail/

2023/09/07/the-pandemic-has-broken-a-closely-followed-survey-of-sentiment;

4. S&P500 Total Return Index, with dividends reinvested: 8/13/1979 1- 07.42; 11/7/2023 – 9,452.28;

5. https://www.bloomberg.com/news/articles/2019-08-13/it-s-been-40-years-since-our-coverstory-

declared-the-death-of-equities

H O W W E L L A R E Y O U M A N A G I N G Y O U R R R S P ?

Avoid These Five RRSP Pitfalls

Registered Retirement Savings Plan (RRSP) season is just around the corner. Beyond the importance of rowing funds for retirement, avoiding certain practices can help to save tax or create a bigger nest egg for the future. Here are five RRSP pitfalls:

1. Withdrawing funds to pay down debt — Consider the implications of making taxable withdrawals from the RRSP to pay down short-term debt. You may be paying more tax on the RRSP withdrawal than you’ll save in interest costs. In addition, once you make a withdrawal from the RRSP, you won’t be able to reinstate the valuable contribution room — unlike the TFSA, where a withdrawal is added back to contribution room in the following year.

2. Contributing losers in-kind — In order to fund the RRSP, some may choose to move investments from non-registered accounts. If you are considering making in-kind contributions to the RRSP, be careful not to transfer investments that have accrued losses. You will be deemed to have sold these investments at fair market value at the time of transfer to the RRSP, yet the capital loss will be denied and any tax relief lost. Instead, consider selling them on the open market and contributing cash to the RRSP so you can claim the capital loss (and, again, be aware of the denied loss rules, thus do not repurchase the investment for 30 days).

3. Claiming the deduction in the wrong year — With any RRSP contribution, you’re entitled to claim a tax deduction for the amount so long as it is within the contribution limit. Keep in mind that you don’t have to claim the tax deduction in the year that the contribution is made. You may carry it forward if you expect income to be higher in future years such that you may be put in a higher tax bracket, potentially generating greater tax savings for a future year.

4. Neglecting to update beneficiary designations — It may be beneficial to review account beneficiaries (in provinces where applicable) periodically and in light of major life changes. For example, in the event of separation or divorce, be aware that named beneficiaries may not be revoked, depending on provincial laws. Therefore, the designation of an ex-spouse may still be in effect.

5. Withdrawing from a spousal RRSP — For couples in which one spouse will earn a high level of income in retirement, while the other may have little income, a spousal RRSP may be a valuable income splitting tool. Yet, don’t forget that the attribution rules generally apply to a spousal RRSP. If the higher-income spouse has made contributions to the spousal RRSP in the year, or immediate two preceding years, and if funds are withdrawn from the plan, they may be taxed to the higher income spouse, as opposed to the lower-income spousal RRSP owner.

RRSP Deadline Reminder:

February 29, 2024 for the 2023 tax year. Limited to 18 percent of the previous year’s income, to a maximum of $30,780.

P E R S P E C T I V E S O N T H E D I V E R G E N C E I N E C O N O M I C G R O W T H

In Brief: Reasons for Diversification

In many aspects, the economies of Canada and the U.S. share similarities as developed countries ranked among the top 10 economic powers globally. Over the past two years, we’ve both grappled to curb inflation, with central banks’ actions mirroring each other. Moreover, both economies have shown substantial economic resilience due to low unemployment rates.

However, more recently, there’s been a divergence in economic growth, with the U.S. showing progress while Canada has been stagnant. This divergence stems from various factors. Higher interest rates are affecting Canadians more than Americans, largely because of the way our mortgages are structured. The average Canadian mortgage has a five-year term, whereas the average U.S. mortgage has a 30-year term. Many Americans secured fixed rates during their lows, so there has been less concern over rising debt payments and this has sustained U.S. consumer spending to support economic growth. New U.S. government initiatives, including the Inflation Reduction Act (focused on green initiatives), the CHIPS and Science Act (backing the semiconductor industry) and the Bipartisan Infrastructure Deal have earmarked trillions in spending to further fuel economic growth.1

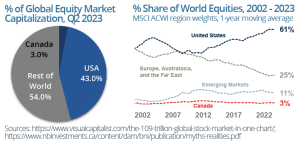

As we consider the economic differences we see today, we should also remember that there are distinct differences from an investing context. Canada, with its considerably smaller population and total output, represents only a fraction of the global equity market, at around 3 percent by market capitalization, in contrast to the U.S. at 4.3 percent (chart). The Canadian equity market is overweight in financials and energy sectors, but underweight in technology, health care, consumer discretionary and consumer staples relative to the global market.

These distinctions should highlight the significance of diversification. Different sectors, industries and regions can exhibit varied performances at different times. Diversification serves to shield against inevitable downturns while offering exposure to top-performing sectors. One interesting perspective comes from the MSCI All-Country World Index (ACWI). Over the past decade, U.S. equities have expanded from around 45 to over 60 percent of global market share within the index (graph).

Yet, in contemplating Canada’s economic path forward, let’s not forget that change is constant. Just three years before the pandemic, some sources proclaimed: “The American Dream Has Moved to Canada.” 2 This should serve as a reminder that economic direction and perspectives can evolve, emphasizing the enduring value of diversification over time.

1. https://www.cbc.ca/news/business/armstrong-economy-us-canada-stimulus-interestrate-

1.7016698#;

2. https://macleans.ca/news/canada/the-american-dream-moved-to-canada

P R O G R E S S D U R I N G C H A L L E N G I N G T I M E S

Looking Forward: Reflecting on a Year That Has Passed

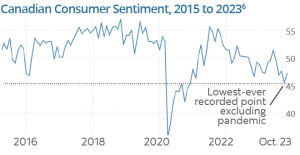

Need some good news? Things may be better than they seem. Understandably, consumer sentiment has lingered at low levels. We’ve been through a lot lately. We’ve persevered through a pandemic, only to face new challenges on the other side, many of which have come about quickly: a substantially higher cost of living, higher interest rates and ongoing global conflict, to name a few.

Yet, according to a recent article in the The Economist, our collective feeling does not accurately reflect actual economic data.1 Since the pandemic, there’s been a growing divergence in sentiment and economic performance.

Indeed, the significant strides we’ve achieved during this economic cycle shouldn’t be overlooked. In Q3, U.S. GDP was reported at4 .9 percent — the highest economic growth since 2014, after adjusting for the pandemic.2 While Canada has been challenged by sluggish growth, we shouldn’t forget this was the central banks’ intention in raising rates to curb inflation. Over the past two years, economic resilience has surpassed expectations, partly due to low unemployment rates. Canada’s fell to its lowest level on record in June/July 2022 at 4.9 percent, and continues to remain at relatively low levels.3 The latest data shows that Canadian household net worth increased for the third consecutive quarter, by 3.4 percent to reach $15,704 billion in Q1 2023.4 In Q2, U.S. households held the highest levels of net worth ever recorded. 5

Households have never been wealthier. The year that has passed serves as a reminder that things can often unfold much differently than predicted. Despite the many challenges, both economies and households have remained comparatively resilient.

This isn’t to suggest there aren’t challenges ahead. However, reflecting on the positive economic outcomes over 2023, there may be a lesson. Don’t lose sight of the economic and wealth-building progress that can be achieved even during seemingly challenging times.

1. https://www.economist.com/graphic-detail/2023/09/07/the-pandemic-has-broken-aclosely-

followed-survey-of-sentiment;

2. https://www.investopedia.com/shoppers-boostedu-

s-economic-growth-to-fastest-in-years-8382874;

3. Since Statistics Canada began formally tracking this data in 1979;

4. https://www150.statcan.gc.ca/n1/daily-quotidien/230614/dq230614a-eng.htm;

5. https://www.federalreserve.gov/releases/z1/dataviz/z1/balance_

sheet/chart/#units:usd;

6. Based on IPSOS data sourced from: https://tradingeconomics.com/canada/consumer-confidence. Note that a level below 50 suggests net negative views

about the economy.

C P P I N T H E S P O T L I G H T

CPP: Four Things You May Not Know

The Canada Pension Plan (CPP) has been in the spotlight as the Alberta government proposes creating its own retirement plan. For the answers to some questions about Alberta’s potential divorce from the CPP, see: https://www.cbc.ca/news/business/cpp-app-pensionquestions-1.7011117. Most of us contribute to the CPP through our employment income, with the expectation that we will receive future CPP benefits, a monthly, taxable payment that will supplement retirement income. Here are four things you may not know:

1. Over recent years, we have been contributing more. In 2019, CPP reforms were put in place to address the decline in workplace pension plans and increase future CPP benefits. The first phase began in 2019 and ended in 2023, gradually increasing the contribution rate by one percentage point on earnings between $3,500 and the maximum pensionable earnings (MPE) limit.

2. In 2024, higher-income earners will pay even more. The second phase of reforms begins January 1, 2024. Employees and employers will contribute an additional four percent on earnings between the MPE and a new ceiling. In 2024, the MPE is $68,500 and the new ceiling will be $73,200 in 2024 and $78,000 in 2025 2.

3. Future benefits will increase, but it will take time. Under the old rules, those retiring at age 65 in 2023 could receive a maximum annual CPP benefit of $15,460. With the new rules, this increases to $23,489 or by over 50 percent, in 2023 dollars1. This also doesn’t account for the 0.7 percent per month enhancement for those who wait to start benefits after age 65, which would further increase the benefit. Very few retirees wait, despite studies showing that deferring to age 70 may be a wise decision if you live to average life expectancy. However, it will take time before the full impact is realized since benefits are generally based on an average of the best 40 years of earnings.

4. CPP survivor benefits are often misunderstood. Many may not realize that CPP survivor benefits may be minimal or non-existent, which can leave a retirement income/cash flow shortfall for a surviving spouse. Consider a situation in which both spouses collect maximum CPP and OAS benefits, collectively providing over $48,000 in annual retirement, based on monthly CPP of $1,307.57 (2023) and OAS of $707.68 (Q4 2023). If one spouse passes away, annual benefits of $24,000 will be lost. This is because the most that can be paid to a survivor eligible for both CPP benefits is the maximum of the two. There is no additional OAS survivor benefit. The CPP provides a one-time “death benefit” payment of $2,500; however, this is hardly sufficient to complement the potential lost income.

1. CPP outcomes mirror QPP: https://www.rrq.gouv.qc.ca/en/programmes/regime_rentes/

Pages/regime-supplementaire.aspx;

2. The 2025 figures are based on the current 2024 MPE

A Tax-Efficient Alternative to GICs: Consider the Benefits of Discounted Bonds

Given the rise in interest rates since the start of 2022, there has understandably been greater interest in low-risk, fixed-income investments like Guaranteed Investment Certificates (GICs). While investors can take advantage of rates not seen in decades, it is important to consider the tax implications. When a GIC is held in a non-registered account, any income earned will be fully taxable at the investor’s marginal rate — compared to capital gains and dividend income, which generally receive more favourable tax treatment. As such, are there tax-efficient alternatives?

Due to rapid rate increases and unprecedented bond market volatility, many quality bonds are trading at discounts to their par values. These bonds may be suitable alternatives to GICs from a risk perspective, but may offer greater after-tax return potential.

A Short Primer: GICs vs. Bonds

GICs pay a guaranteed return, expressed as an interest rate paid on the amount invested, which is taxable as interest income in a nonregistered account. Since they aren’t tradeable assets, they don’t vary in price. At maturity, the original investment is returned to the investor. Bonds, on the other hand, generally pay a coupon, or annual interest rate (sometimes paid semi-annually), which is taxable as interest income. The coupon rate is expressed as a percentage of the bond’s “face value” — the amount paid to the bondholder at maturity. Over the life of the bond, a bond’s price can vary as interest rates change.

If interest rates were to rise, any comparable bonds would now offer a higher coupon amount. As such, the bond that was issued at the lower interest rate, which pays a lower coupon, will need to fall in price so that its coupon and eventual face value paid at maturity will be equivalent to the new bond. When a bond is sold for less than its face value, it is termed a “discounted bond.” Conversely, if interest rates fall ,the bond’s price will rise. If it is sold for more than its face value, it would be sold at a “premium” (or above par).

Discounted Bonds: A Tax Advantage

What makes a discounted bond attractive from a tax perspective? Since the bond was purchased at a discount from its face value, part of the total return from the bond comes from capital gains. The coupon amount would still be taxed as interest income; however, the capital gain would be subject to a lower tax rate. This makes the discounted bond more tax-efficient than a comparable GIC with returns fully taxable as interest income.

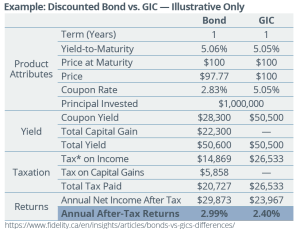

To illustrate the tax efficiency of a discounted bond compared to a GIC, the chart compares a bond offered by a $14 billion Canadian packaged foods company with a yield to maturity of 5.06 percent to a GIC that pays interest at 5.05 percent. Based on a tax rate of 52.54 percent, the after-tax return for the bond is 2.99 percent, whereas the GICs’ return is only 2.40 percent once taxes are considered. In fact, on an initial $1 million investment, the net after-tax income is $5,906 more for the bond than for the GIC.

What accounts for such a difference? Since capital gains are treated more favourably, as a result, the blended tax rate is only 41 percent for the bond, compared to 53 percent for the GIC. In some cases, even if a GIC has a higher pre-tax expected return than a discounted bond, the after-tax returns of the discounted bond may be notably higher. In addition to the tax advantage, many quality bonds are more liquid than GICs. As well, in a situation where future interest rates decline, there may be an opportunity for investors to realize gains before the bond reaches maturity. Since many quality bonds currently trade at a discount, investors may be able to find appropriate portfolio additions that meet their risk tolerance, while offering higher after-tax returns than GICs. To learn more, please feel free to call the office.