A Cloud of Uncertainty

The rhetorical tautology, “Predictions are difficult, especially about the future” may feel particularly relevant today.1 The start of 2025 has been marked by low visibility, with two events casting a cloud of uncertainty over investor sentiment: the launch of DeepSeek’s AI platform—claiming to be a significantly lower-cost model—and U.S. President Trump unleashing a trade war.

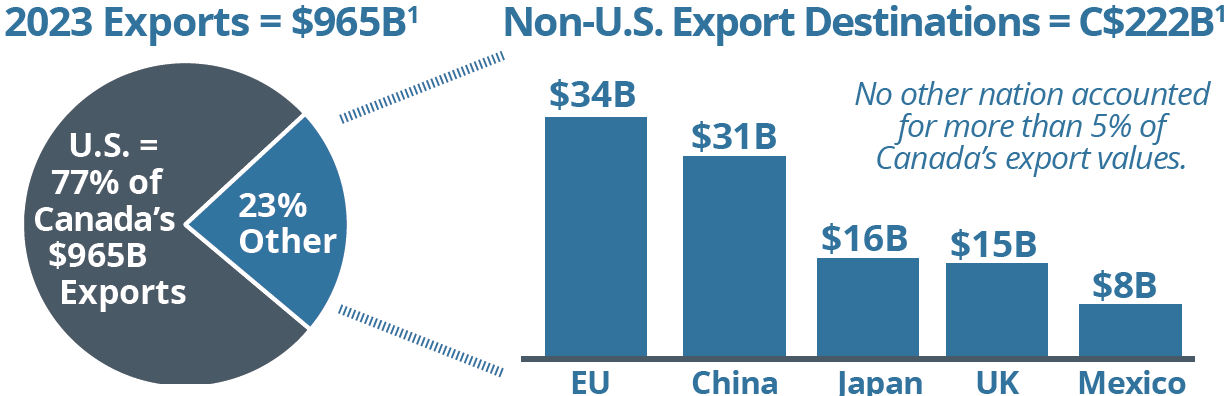

While the shift in U.S. policy direction has felt particularly unexpected—from tariffs against its closest ally to talk of annexation—it serves as a reminder of the value of diversification. Until now, Canada’s dependence on the U.S. as its primary export market has largely been overlooked: 77 percent of exports go to the U.S.—no other nation accounts for more than 5 percent.2 Just as diversification is important in portfolio management, it is equally critical in trade.

Over recent years, the focus on diversification in investing may have also taken a back seat. Market gains have been largely driven by a handful of U.S. tech giants, whose dominance has gone mostly unchallenged. DeepSeek’s emergence highlights that disruption is inevitable in any innovation cycle, and no sector remains immune.

If the first few months of 2025 have taught anything, it is to expect the unexpected. It may also be a watershed moment—signaling a shift toward a new era of national protectionism. Indeed, it appears to be a critical juncture for Canada to focus on strengthening its economic position.

The tariff situation has also reignited the debate over its effectiveness. While Trump actively campaigned on using tariffs to address the U.S. deficit and support tax cuts, the old economic principle still holds: If you want more of something, subsidize it; if you want less, tax it. Many economists agree that tariffs will have negative effects on the U.S. economy at a time when it faces its own uncertainties: persistent inflation, higher interest rates and slowing economic growth.

Given this backdrop, the tariff situation may evolve. As we have seen, the policy direction of the new U.S. administration is prone to shifting at any time. Even so, the effects of policy changes aren’t always immediate or predictable. And, markets and economies don’t always react as anticipated—as we saw in the pandemic’s aftermath. One of the best ways to navigate uncertainty is by preparing for multiple possible outcomes. Diversification is intended to position portfolios to withstand changing environments and varying conditions.

With the shifting rhetoric south of the border, the next four years will likely be a test of investor discipline. Many other factors, such as geopolitical instability, economic declines or stock market volatility, are also beyond an investor’s control. Yet, more often than not, how an investor reacts to these uncontrollable events can have the greatest impact on long-term outcomes. The key will be to look beyond the headlines and keep a broader perspective. While the near-term path may not always be clear, history has shown that, as with any cycle, the seasons change, the clouds will part and brighter days are never far behind.

For many of us, recent events feel unsettling. We continue to monitor the ongoing developments and their potential impact on portfolios making adjustments where needed, without losing focus on the longer term. While challenges undoubtedly lie ahead, brighter days will eventually prevail. Please reach out if you have concerns.

1. Attributed to Niels Bohr, Danish physicist, and Yogi Berra, baseball player, known for saying, “It ain’t over ‘til it’s over”; 2. https://www. scotiabank.com/ca/en/about/economics/economics-publications/post.other-publications.canada-and-us-economics-.canada-and-us-decks.trade-stats–january-31–2025-.html

SPRING CLEANING

When Less Is More: Simplifying Your Finances

Former Wall Street Journal finance columnist Jonathan Clements has long advised readers to plan on living past age 90. But when, at age 61, he was diagnosed with an illness that gave him just a year to live, his financial priorities shifted. His focus turned to ensuring his family would be well-prepared for a time when he was no longer around. One key step? Simplifying his finances: “I thought my finances were well-organized and pretty simple. Yet, since my diagnosis, I’ve spent endless hours trying to simplify them even further.” His conclusion: “Death is hard work.”1

Indeed, when life becomes more challenging, simplicity matters more. If you are tackling spring cleaning this season, perhaps there may be an opportunity to revisit your finances. Here are two places to start:

Consolidate Financial Accounts — Consider the benefits of consolidating bank, investment and other financial accounts, where possible: better asset allocation, improved tax efficiency, easier administration and no “orphan” accounts forgotten over time. Just as important, it may make life easier for loved ones by reducing the number of accounts they may need to manage in the future if something were to happen.

Reduce Your Digital Footprint — How many online accounts do you have? According to one source, the average person holds 100!2 While this might seem high, it adds up quickly when factoring in email, social media, financial, entertainment, retail and other services. The more accounts you have, the greater your exposure to fraud through data breaches and cyberattacks. One of the best ways to protect yourself is by limiting the information scammers can access. Close unused accounts and delete inactive ones to minimize the risk of personal data being compromised.

Other Ways Less Can Mean More

Here are other ways simplifying can lead to greater financial efficiency and peace of mind:

- Automate Savings & Investing — Fewer decisions can lead to consistent habits. Setting up automatic transfers can help you stay on track toward long-term goals with minimal effort.

- Cut Subscription Fat — Reduce unnecessary recurring expenses (streaming, apps, memberships) to free up cash flow.

- Use Fewer Credit Cards — Reducing the number of credit cards you hold can lower the risk of missed payments or help to minimize fees. Fewer cards may also encourage more intentional spending habits. At the same time, strategically designating cards for specific purposes—such as one for online purchases and another for recurring bills—can make it easier to manage accounts and quickly respond to fraud if a card needs to be cancelled.

- Minimize Debt Accounts — Consolidating loans or prioritizing high-interest debt may be financially prudent to lower interest costs.

- Teach Younger Folks to Avoid Lifestyle Creep — Prioritizing needs over wants can help prevent overconsumption and financial stress. Owning fewer things can also mean lower maintenance costs and more financial freedom.

1. https://www.wsj.com/personal-finance/jonathan-clements-personal-finance-cancer-e30d1396; 2. https://www.cnn.com/2024/02/26/tech/digital-legacy-planning-personal-technology/index.html

PERSONAL TAX SEASON IS HERE AGAIN

A Turning Tide? Work From Home (& Tax Reminders)

Is the golden age of working from home (WFH) nearing its end? Last fall, the federal government mandated that employees return to the office (WFO) three days a week. Major corporations like Amazon and Dell have gone further, requiring full-time in-office work. The upside? This shift may help revitalize downtown areas that have struggled with vacancies since the pandemic. Proponents of WFO also argue it will boost productivity—one study suggests remote work may reduce productivity by 10 to 20 percent!1

Regardless of your stance, tax season is a reminder for remaining WFH workers to claim home office expenses. This year, Form T2200 has been amended to simplify employer certification. Now, employers only need to confirm whether an employee worked from home more than 50 percent of the time over a period of at least four consecutive weeks. According to the CRA, taxpayers claimed a record $2.08 billion in home office expenses in 2023, a 41.4 percent increase from the 2022 tax year, when the temporary flat-rate method was last available.2

Here are other notable tax changes as you file your 2024 returns:

Capital Gains. The proposed increase to the capital gains inclusion rate has now been deferred to January 1, 2026, from June 24, 2024. For those impacted, the CRA is providing additional time for taxpayers to meet their tax filing obligations, granting relief from late-filing penalties and interest until June 2, 2025, for individuals and May 1, 2025, for trusts.

Alternative Minimum Tax (AMT). For 2024 and beyond, the AMT rate increases to 20.5 percent from 15 percent and the basic exemption threshold rises to $173,205 from $40,000.

Charitable Donations. Due to the postal strike, draft legislation extended the deadline for 2024 charitable donations to February 28, 2025. Individuals can choose to claim eligible monetary donations made up to February 28, 2025, on their 2024 tax return, 2025 return or during the normal five-year carryforward period. Corporations with taxation years ending after November 14, 2024, or before January 1, 2025, are also eligible.

Short-Term Rentals. If you rent a residential property for less than 90 consecutive days, you must now comply with all provincial and municipal regulations and licensing or the CRA will deny any expense deductions. Transitional relief is in place for the 2024 tax year.

Canada Carbon Rebate (CCR) for Small Business. While the government stated that the rebate is tax free, at the time of writing, legislation is pending so it must be reported as taxable income.3 This was distributed in December to eligible Canadian-Controlled Private Corporations (CCPCs) to offset the federal fuel charge in certain provinces: AB, MB, NB, NL, NS, ON, PE, SK. CCPCs in other provinces/territories may be eligible if they employ people in designated provinces.

1. https://www.forbes.com/sites/benjaminlaker/2023/08/02/working-from-home-leads-to-decreased-productivity-research-suggests/; 2. https://www.investmentexecutive.com/news/industry-news/claims-of-home-office-expenses-increased-41-last-tax-season/; 3. https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/business-tax-credits/canada-carbon-rebate-small-businesses.html

TARIFF TALK: WHERE DO WE STAND?

Oh, Canada: Trade Perspectives, in Brief

In brief, here are four perspectives on Canada/U.S. trade:

- The U.S. is Canada’s main export market. In 2023, Canadian total exports were valued at C$965 billion, with 77 percent going to the U.S. No other nation accounts for more than 5 percent of Canada’s exports.1

- Canada is the U.S.’s largest export market. However, only 18 percent of total U.S. exports go to Canada.2 These exports account for 44 percent of Canadian imports, which totaled C$978 billion in goods and services in 2023.1

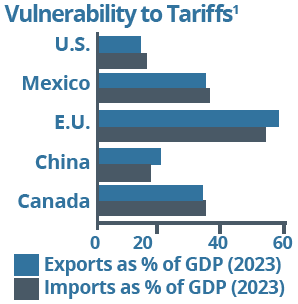

- Canada is relatively vulnerable to tariffs. When comparing trade as a percentage of GDP (chart, right), Canada has greater exposure than the U.S. and China. However, Mexico and the E.U. are more vulnerable by this metric.1

- The U.S. relies on Canada’s resources. Canada exports over 4 million barrels of oil per day to the U.S., with Midwest refiners importing 3 million barrels daily and lacking viable alternatives.3 Canada ranks 4th globally in natural resource value4 and is a key supplier of critical minerals, providing around 50 to 80 percent of U.S. zinc, tellurium, nickel and vanadium.5

1. https://www.scotiabank.com/ca/en/

about/economics/economics-publications/post.other-publications.canada-and-us-economics-.canada-and-us-decks.trade-stats–january-31–2025-.html; 2. https://www.usitc. gov/research_and_analysis/tradeshifts/2023/us_ trade_industry_sectors_and_selected_trading; 3. https://www.bnnbloomberg.ca/investing/commodities/2025/02/03/eric-nuttall-says-the-us-has-no-alternative-to-replace-canadian-oil/; 4. https://www.voronoiapp.com/natural-resources/Ranked-Top-Countries-by-Natural-Resource-Value-2885 (2021 figures); 5. https://economics.td.com/domains/economics.td.com/documents/reports/me/Setting_the_Record_ Straight_on_Canada_US_Trade.pdf

PERSPECTIVES ON THE LOONIE’S DECLINE

Food for Thought: A Weaker Canadian Dollar

The Canadian dollar’s (CAD) weakness has raised questions about its broader impact and the path forward:

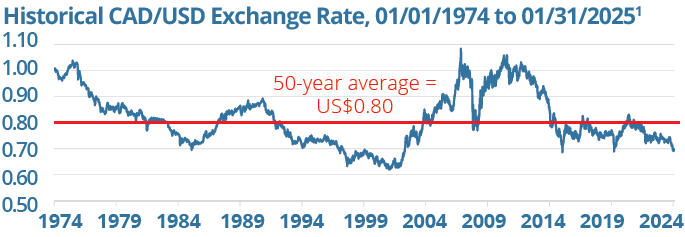

The CAD is trading below its historical average. To start 2025, it fell below 68 U.S. cents—a level not seen in two decades. The decline has been driven by factors such as diverging U.S. and Canadian monetary policies (lower interest rates make the CAD less attractive to foreign investors), ongoing tariff threats and a strong U.S. dollar. Historically, the CAD has moved in cycles. From 2005 to 2014, it benefitted from strong resource demand, surpassing parity with the U.S. dollar (USD) in 2007 and peaking at US$1.09. Over 50 years, it has averaged around US$0.80.1

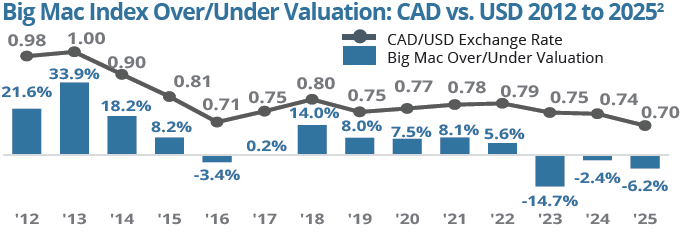

Will the loonie continue its fall? The “Big Mac Index” may offer some fun “food for thought.” Published by The Economist, it was developed as a lighthearted way to make exchange-rate theory digestible by comparing the purchasing power parity (PPP) of currencies. PPP suggests that, over time, exchange rates should adjust so that an identical basket of goods and services costs the same in each country. The index estimates an exchange rate by comparing the price of a Big Mac in different nations to its cost in the U.S. By comparing this to the prevailing exchange rate, it gauges whether a currency is under- or overvalued. According to the index, the CAD is undervalued (chart, top).

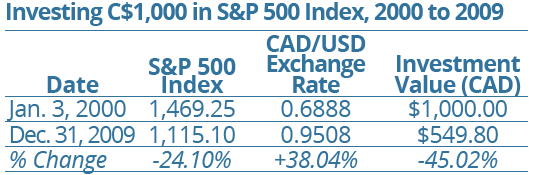

What does this mean for investors? Currency swings can impact returns on foreign-denominated investments when converted to Canadian dollars. A notable example occurred between 2000 and 2009—a period with parallels to today. At the start of 2000, U.S. equity markets were at record highs amid the dot-com boom, while the CAD traded below 70 cents USD. If an investor put CAD into the S&P 500 Index in early 2000, they would have experienced a loss—not just due to the market downturn, but also due to currency appreciation. By December 2009, the S&P 500 declined by 24.1 percent, but over the same period, the CAD appreciated by 38 percent.

Over the long run, currency fluctuations tend to even out in well-diversified global portfolios, as gains in one currency can offset losses in another. There are also ways to mitigate currency risk directly, depending on an investor’s objectives, such as by using currency-hedged investment funds or Canadian Depository Receipts, which allow investors to buy foreign stocks on Canadian exchanges in CAD.

1. https://ca.investing.com/currencies/usd-cad-historical-data; 2. January data; https://github.com/

TheEconomist/big-mac-data/tree/master/output-data

The Evolving Trade War:

Is a Recession Looming?

When the U.S. launched a trade war in January, many were quick to warn of a possible recession. With Canada’s economy already growing at a sluggish pace—GDP growth is projected at just 1.8 percent for 2025—the Bank of Canada estimated that a blanket 25 percent tariff would reduce annual GDP growth by 3 to 4 percentage points. While the tariffs implemented in March have been subject to change, concerns about their economic impact have continued to grow.

Is a Recession Imminent?

A recession is typically defined as two consecutive quarters of declining GDP. While tariffs will undoubtedly put downward pressure on the economy, Canada has a few economic buffers in its favour:

- Low interest rates and inflation — Both help to support consumer spending. For example, recently released Q4 2024 GDP data showed annualized growth of 2.6 percent, surpassing expectations and driven by stronger consumer spending;1

- A weaker Canadian dollar — This makes Canadian exports more competitive as they cost less, potentially offsetting some of the tariff impact on U.S. buyers; and

- Government intervention — As we witnessed during the pandemic, the government has been willing to provide fiscal and monetary support when conditions deteriorate, thus preventing a prolonged downturn. The federal government has already announced potential aid in light of the evolving situation.2

It is also worth noting that the U.S. economy is facing its own uncertainties, including persistent inflation, higher interest rates and weakening economic data. One inflation-related development garnering significant recent attention is the soaring price of U.S. eggs, which have more than doubled since August 2023 due to the avian flu. Less than a year ago, a dozen eggs cost an average of $2.04; today they are around $4.95—if you can find them, as many store shelves remain empty.3 The effects of higher tariffs continue to be actively debated in U.S. circles, with many concerned that tariffs will lead to higher prices for U.S. consumers.

Perspectives for Investors

Without a doubt, broad-based tariffs would put downward pressure on the economy. However, it is important for investors to keep things in perspective. Here are some reasons why:

Markets and economies don’t always move in sync. Seasoned investors know that markets don’t always mirror the state of the economy. At times, economic and stock market performance can diverge. The composition of the market also differs from the economy. For example, the S&P/TSX is heavily weighted in sectors like financials (33%), energy (17%), and metals and mining (12%).4 While these sectors are key to the economy, they can have a disproportionate influence on the index. Not all sectors will react similarly to tariffs. Consider the financial services sector, for example. It’s unlikely to see a major direct impact from tariffs, though an economic slowdown could still affect things like loan loss provisions. As advisors, we are continuously evaluating the potential effects of the evolving

tariff situation on investments.

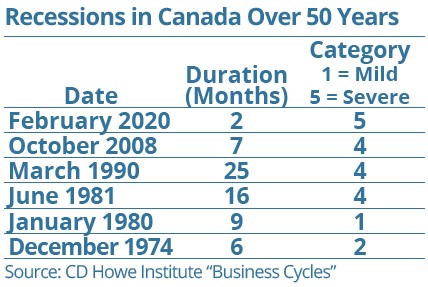

Economic cycles are normal. While recessions have become less frequent in recent years (chart, above) due to government intervention, economies—just like financial markets—naturally expand and contract over time. It’s unrealistic to expect perpetual economic expansion. Contractions are a natural part of the cycle and often serve as a much-needed reset to correct inefficiencies and ignite growth.

Equity markets trend upward over the longer term. Despite financial crises, pandemics, supply chain issues, war—and even recessions—the longer-term trend of the markets has been upward. From 1945 to 2022, we’ve seen all these challenges; yet the S&P 500 delivered positive returns in 78 percent of one-year periods and 97 percent of 10-year periods. Similarly, the S&P/TSX posted positive returns in 74 percent of one-year periods and 100 percent of 10-year periods.5

Consider also that the economy and the markets don’t always react as expected—especially in extreme scenarios. Take the pandemic, for example, which many expected would lead to a prolonged recession. Moreover, if the start of 2025 is any indication, the nature and degree of tariffs can shift at any time—the policies of the new U.S. administration appear to change rapidly. During uncertain times, careful analysis and thoughtful investment selection become even more critical. This is where the support of advisors provides value. For a deeper discussion, please call.

1. https://financialpost.com/news/economy/canadas-economy-gained-momentum-2024-beating-expectations; 2. https://www.ctvnews.ca/business/article/ottawa-announces-6-billion-aid-package-for-businesses-hit-by-trade-war/; 3. https://fred.stlouisfed.org/series/APU0000708111; 4. At 01/31/25: https://www.spglobal.com/spdji/en/indices/equity/sp-tsx-composite-index/; 5. https://ca.rbcwealthmanagement.com/documents/691191/0/market_ perspectives_play_long_game_apr2023.pdf/eddab819-e602-4064-8b19-8e1283950129

The information contained herein has been provided for information purposes only. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information has been provided by J. Hirasawa & Associates and is drawn from sources believed to be reliable. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document. Wellington-Altus Private Wealth Inc. (WAPW) and the authors do not guarantee the accuracy or completeness of the information contained herein, nor does WAPW, nor the authors, assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact me for individual financial advice based on your personal circumstances. All insurance products and services are offered by life licensed advisors of Wellington-Altus Insurance Inc. or other insurance agencies separate from Wellington-Altus Private Wealth.