The Illusion of Speed

It has been said that “there are decades where nothing seems to happen, and there are weeks where decades happen.” The sweeping global tariffs, announced by the U.S. on April’s “Liberation Day,” caught the world off guard—disrupting long-held norms in global trade and world order. This may signal the beginning of a new chapter—one where political disruption, rapidly shifting policies and the velocity of digital information collide.

We’ve seen a wave of financial market volatility triggered by how rapidly these changes were communicated—and perceived. In today’s hyper-connected world, the pace of modern life has never been faster. That same urgency has seeped into the way we make decisions.

Technology underpins this behavioural shift. The average investor now holds a stock for just months—down dramatically from the multi-year horizons of previous generations.1 A recent study found that many retail investors spend less time researching a stock than they do reading a restaurant menu.2 The result? Decisions are driven more by momentum and emotion than thoughtful, long-term planning.

Markets, too, have become increasingly reflexive. April’s rapid selloff, followed by the swift recovery in May, shows how quickly sentiment can shift.

Similarly, the U.S. administration’s approach has been characterized by rapid disruption, with some describing it as a “move fast and break things” approach.3 The speed at which new policies are introduced amplifies the perception of urgency—even when outcomes remain uncertain, or when policies may later be changed—or even reversed.

Yet amid this policy whiplash, a shift may be taking place: a move away from globalization toward greater national protectionism, security and economic self-sufficiency. This pivot has raised deeper questions about the role of the U.S. as the dominant superpower. During April’s volatility, a sharp selloff in U.S. Treasurys raised concerns—particularly as China, which holds about one-sixth of all foreign-owned U.S. Treasurys, has been increasing its gold reserves. Subdued demand for the U.S. dollar—once the default safe haven—has prompted questions about its future as the global reserve currency. Since the start of the year, its value has fallen by around 9 percent4—a rare and significant drop. Questions about waning confidence in U.S. global leadership have emerged. To paraphrase one analyst: “You can’t antagonize and influence at the same time.”

This environment should serve as a reminder: speed does not always equate to change. The illusion of speed—fueled by technology and policy turbulence—can distort our sense of urgency and lead us to chase headlines rather than stay grounded in fundamentals. It’s a dynamic that can leave investors vulnerable to short-term noise. Investing, at its core, rewards patience.

While the events of April may already feel like a distant memory, it’s understandable that the market movements were unsettling for many. If you have friends or family who could benefit from our approach, we would be happy to offer support. We’ve navigated these challenging times before and continue to provide value through a disciplined process.

After a spring marked by ‘weeks where decades seemed to happen,’ may your summer days be filled with many slow and relaxing moments.

- https://www.visualcapitalist.com/the-decline-of-long-term-investing/; 2. https://www.wsj.com/finance/investing/buying-stocks-research-study-2a839a4a; 3. A term coined in the tech industry; 4. To end of May, per ICE U.S. Dollar Index.

Bridging the Housing Affordability Gap

Supporting a Home Purchase? Five Questions to Ask

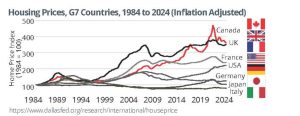

Without a doubt, home ownership has become increasingly out of reach for younger generations (chart, bottom right). Canadian home prices have risen faster than in any other G7 country—nearly quadrupling over 40 years (graph, top). As such, many families are stepping in to help.

Beyond easing financial stress, this support can have added benefits. Many high-net-worth individuals value the opportunity to see their wealth in action during their lifetime. Lifetime gifting can also simplify estate administration and, depending on province, may reduce probate fees.

Still, meaningful support requires thoughtful planning to avoid unintended consequences. Here are five key questions to consider:

- How will this impact my own finances? Many people draw from lifetime savings to provide support. It’s essential to assess how this could affect your long-term financial security—especially given increased life expectancy and the rising cost of long-term care.

- How do I structure my support? Support can take many forms, including gifting cash, loaning funds, co-signing a mortgage or purchasing a property in your own name—each with different tax and family law implications.* Remember, gifting means giving up control. Smaller, ongoing support may allow the recipient to leverage tax-advantaged tools like the Tax-Free Savings Account (TFSA) or First Home Savings Account.

- What are the family law implications? If the recipient is in a relationship that ends, gifts or property could be subject to division, depending on provincial family law. There may be ways to protect the intent of your support, such as through the use of formal ownership agreements or cohabitation agreements.*

- Are there tax implications? While Canada has no gift tax, some arrangements can trigger taxable events. For example, co-owning a property with the recipient may protect your share, but if it’s not your principal residence, you could face capital gains tax upon its sale or disposition. Large gifts from taxable investment accounts could also trigger capital gains or income tax.

- Will this affect my estate plan? If you have multiple children who are intended beneficiaries, a gift to one child can affect how you equalize your estate. A strategic approach might include integrating gifting into an estate equalization plan—through lifetime gifts or testamentary planning using trusts or insurance.

*Consult legal and tax professionals to understand the implications of any strategy.

Housing Costs Over 40 Years: Kids Today May Have It Harder

| 1984 | 2012 | Today | % Change from 1984 | |

| Average home cost | $76,214 | $369,677 | $712,200* | +834% |

| Median family income | $48,500 | $71,700 | $107,663** | +122% |

| Price-to-income ratio | 1.57 | 5.16 | 6.62 | +321% |

| 5-yr. fixed mortgage | 14.96% | 4.23% | 4.70%*** | –69% |

| 75% mortgage value | $57,161 | $277,258 | $534,150 | +834% |

| Monthly payment (25 yr.) | $711 | $1,493 | $3,016 | +324% |

| Payment-to-income ratio | 17.6% | 25.0% | 33.6% | +91% |

| Lifetime interest cost | $156,034 | $170,704 | $370,665 | +138% |

*National benchmark, April 2025: https://wowa.ca/reports/canada-housing-market. **StatCan Table 11-10-0190-01, 2022 figure (after tax) with 2.56% annual wage growth in 2023-25. ***Avg. major banks’ five-year fixed rate, April 28, 2025. Historical data source: “2012 vs 1984: Yes, Young Adults Do Have It Harder Today,” R. Carrick. Globe & Mail, 8 May 2012, B12.

Macroeconomic perspectives

A Credit Downgrade: What’s in a Rating?

In May, Moody’s downgraded the U.S. credit rating from the top Aaa to Aa1. This move by one of the major credit rating agencies—S&P and Fitch are the other two—raised the question: Does a downgrade matter?

First, what is a rating? A credit rating assesses a borrower’s ability and willingness to repay debt. Unlike personal credit scores, which typically range from 300 to 900, government credit ratings are expressed as letter grades, with AAA representing the highest quality and lowest risk. A downgrade implies an increasing likelihood that a government may default on its bonds.

Why does this matter? A downgrade generally means investors demand higher interest rates to compensate for added risk. Higher interest payments raise the cost of government borrowing. To sustain spending, more bonds must be issued—further increasing the debt burden. In the U.S., interest payments have become the second-largest federal expense, surpassing defence spending in 2024.

While credit downgrades can shake investor confidence, equity markets had a muted response, briefly jittering. This was partly because the move wasn’t a surprise, lagging similar downgrades by Fitch in 2023 and S&P in 2011. However, bond prices have come under pressure, sending yields higher, with the 30-year rate surpassing 5 percent in May. It comes at a time when a Republican tax bill rekindled debate about the sustainability of the U.S. deficit and spending.

There are likely to be ripple effects. A surge in U.S. mortgage rates may dampen consumer spending. Credit card and auto loan rates are less likely to be affected, as they tend to follow the federal funds rate more directly.

Why is this significant for Canada? Canada is among the few nations still holding the top credit rating from at least two major agencies. Fitch downgraded Canada in 2020 due to pandemic-related spending. While Canada’s credit outlook remains stable, a downgrade would be unwelcome. Net debt is not out of step with other AAA-rated economies, but gross debt levels are high, and rising interest rates would raise debt-servicing costs—straining future budgets. The heightened focus on global debt may help explain why Prime Minister Carney has opted to delay the release of the federal budget, usually delivered in the spring. Credit agencies continue to evaluate sovereign debt positions, and the U.S. downgrade follows a move by Moody’s to downgrade France at the end of 2024.

thinking ahead:

Planning a Tax-Efficient Withdrawal Strategy

“A dollar’s value depends on the tax trail it travels.”

How and when you access your income sources can influence the taxes you pay, your eligibility for government benefits and your long-term financial health. Whether you’re accumulating wealth, transitioning between career stages or planning for retirement, a tax-efficient withdrawal strategy can make a meaningful difference. Here is a brief look at common income sources and ideas to help you optimize withdrawals or manage income streams more effectively:

Non-Registered Accounts — Tax treatment depends on the type of income: interest (fully taxable), dividends (eligible for a dividend tax credit) or capital gains (50 percent is taxable). Tax-loss harvesting can offset capital gains to reduce your overall tax bill.

Registered Retirement Savings Plan (RRSP) — Withdrawals are fully taxable and subject to withholding tax. Importantly, once funds are withdrawn, contribution room is permanently lost.

TFSA — Offers significant benefits as growth is tax free and withdrawals are not taxed. This means withdrawals do not affect income-tested government benefits. Any amount withdrawn can be recontributed in the following calendar year.

Employment Income — If you continue to work while drawing income from other sources, consider how employment income will stack with taxable withdrawals. In high-income years, deferring benefits (if possible) or adjusting other withdrawals may help reduce the overall tax burden.

Here are additional considerations for those nearing retirement:

Canada/Quebec Pension Plan (CPP/QPP) — CPP/QPP benefits are taxable income. Timing matters: starting early reduces benefits by 7.2 percent per year before age 65. Delaying increases payments by 8.4 percent per year after age 65, to a maximum of 42 percent by 70. The total benefit received can impact income level and tax situation.

Old Age Security (OAS) — OAS is a taxable benefit starting at age 65. If you expect higher income later in life, here are two considerations: i) Clawback—If net income exceeds $93,454 (2025), OAS is reduced by 15 percent of the excess. At $151,668 (ages 65 to 74), it is fully clawed back; and ii) Delaying OAS—This increases the benefit up to 36 percent by age 70.

Registered Retirement Income Fund (RRIF) — Mandatory RRIF withdrawals begin the year after the RRIF is opened, increasing taxable income. Some choose to begin RRSP withdrawals earlier to manage future tax exposure or reduce the risk of triggering the OAS clawback.

Company Pension — Pension income is taxable. After age 65, the pension tax credit may help offset the tax liability. Consider timing your pension’s start with other sources of income to manage your tax liability.

Don’t Forget: Income Splitting — Couples can sometimes lower their combined tax burden by splitting certain types of income, especially when one has significantly higher income. For retirees, shifting eligible pension income may reduce taxes or the OAS clawback. In cases of continued employment, coordinating taxable income (particularly after 65) may yield tax savings over time. Planning together can lead to better outcomes.

Building a tax-efficient income plan involves many moving parts. Knowing how and when to draw income may help reduce taxes and preserve benefits. Alongside tax advisors, we can help develop a strategy that balances cash flow needs, tax implications and government benefits to support your long-term financial goals.

perspectives on market volatility

The Merits of Hanging in (& Why April Felt So Bad)

It’s been a wild ride this year—and we’re only halfway through.

If April’s market movements felt unsettling, you weren’t mistaken. While volatility is a natural part of equity markets, the magnitude of April’s decline was unusual. A two-day drop of more than 10 percent in the S&P 500, seen over April 3 and 4, is rare and has occurred only four times since 1980: on Black Monday in 1987, twice during the 2008 Global Financial Crisis (GFC) and in the early days of the 2020 pandemic.

It’s worth repeating: while it might feel tempting to exit the markets during turbulent periods, doing so can come at a cost. One reason is that some of the best-performing days often follow the worst. Exiting the markets after a decline may mean missing out on these gains, which can then make re-entering even more difficult. We saw this play out in the spring when April’s sharp drop was followed by a swift recovery in May.

While markets don’t always rebound immediately, time has a powerful way of smoothing even the sharpest declines. In the year following the worst two-day drops, the S&P 500 posted an average gain of 36.3 percent. Similarly, after the largest one-day declines in the S&P/TSX, the average one-year forward return was +34.6 percent.

One of the benefits of navigating through challenging markets like the GFC and the pandemic is that we have accumulated invaluable experience. Time and again, we are reminded that you can’t keep the markets—or the economy—down for long.

Even the darkest nights eventually give way to dawn—and patience remains one of an investor’s great virtues.

- BMO Capital Markets, U.S. Strategy Report, April 6, 2025. 2. BMO Capital Markets, Canadian Strategy Report, April 6, 2025. Calculations based on BMO Capital Markets Investment Strategy Group calculations, Factset, Compustat, IBES.

S&P 500 Two-Day Declines & One-Year Forward Return1

| Date | Decline | 1-Yr. Forward Return |

| 10/19/1987 | -24.6% | +23% |

| 3/12/2020 | -13.9% | +59% |

| 11/20/2008 | -12.4% | +45% |

| 11/6/2008 | -10.0% | +18% |

| Average | -15.2% | +36.3% |

Largest S&P/TSX One-Day Declines & One-Year Forward Return2

| Date | Decline | 1-Yr. Forward Return |

| 3/12/2020 | -12.3% | +51% |

| 10/19/1987 | -11.3% | +6% |

| 3/9/2020 | -10.3% | +27% |

| 3/16/2020 | -9.9% | +53% |

| 12/1/2008 | -9.3% | +36% |

| Average | -10.6% | +34.6% |

A New Trade Order?

How Tariffs Are Reshaping Global Dynamics

The global trade landscape was thrown into flux when the U.S. introduced a sweeping wave of tariffs on April’s “Liberation Day,” aimed at reshaping its economic relationships. While the situation continues to evolve, tariffs remain at the centre of global attention. Here’s a brief look at how they are reshaping trade dynamics—and what it could mean going forward.

First, What Is a Tariff?

A tariff is a duty (or tax) applied to goods brought into a country, calculated as a percentage of the product’s value. The rate often depends on two factors: i) Product country of origin (where it’s from); and ii) Type of product.

Tariffs are generally designed to protect domestic industries by reducing the competitive advantage that foreign producers might have—whether due to cheaper labor, lower production costs, more lenient environmental regulations or financial support from foreign governments. These tariffs are paid by the importer when goods enter the country, with the funds collected on behalf of the government of the importing country.

What Is the Rationale Behind Broad-Based Tariffs?

Although the current U.S. administration hasn’t officially outlined its reasoning, President Trump has long advocated for tariffs as a strategic tool. They appear to be aimed at a range of objectives: shrinking the trade deficit by boosting exports and curbing imports, encouraging domestic manufacturing and onshoring, reinforcing national supply chain security, fighting unfair trade practices, increasing federal revenue and applying pressure on trading partners to negotiate better terms.

The Potential Effects: Economic and Market Impacts

Tariffs have heightened economic uncertainty, due to a range of potential effects, such as:

Pricing pressures for consumers — Since tariffs are essentially import taxes, U.S. businesses bringing in foreign goods are on the hook for the added cost. More often than not, these additional costs get passed down to consumers. That means higher prices, feeding into inflation and potentially softening purchasing power.

Disrupted trade and supply chains — Businesses thrive on predictability, but evolving tariff measures introduce uncertainty. Many firms now struggle to make long-term decisions on production, investment and supplier relationships. Tariffs can also impact trade volumes. As a recent example, in April amid the temporary but sharp 135 percent tariff on Chinese imports, there was a 21 percent year-over-year drop in Chinese outbound shipments to the U.S.1

Downward pressure on company profits — Higher input costs, potentially lower demand and logistical complications can impact profit margins for affected companies. This can lead to cost cutting, including layoffs—especially in industries heavily reliant on international trade.

Broader economic drag — Collectively, all of these dynamics weigh on economic growth. In the U.S., consumer spending accounts for roughly 68 percent of U.S. GDP, so the combination of rising prices, rising unemployment and general uncertainty could weigh on economic growth.

Rethinking Global Trade Norms

For decades, global trade has leaned on the principle of “comparative advantage”—the idea that countries should focus on producing goods they can make most efficiently. That approach has kept prices lower—and supported broad-based global economic growth. As renowned investor Howard Marks recently noted: “Globalization has contributed to a rising economic tide that has lifted all boats.”2

Critics of the new tariff strategy argue that shifting away from globalization isn’t so simple. For example, building out domestic manufacturing requires massive investments in infrastructure, which also take time. Plus, U.S. companies often can’t match the low labor costs found overseas. According to one estimate, producing an item like an iPhone on U.S. soil could cost around US$3,500.3 While developing nations have benefitted from globalization, so have countries like the U.S. and Canada, especially through cheaper consumer goods.

What Lies Ahead?

At the time of writing, the situation continues to evolve—from legal challenges to ongoing negotiations between the U.S. and various countries. As such, trade policy is likely to remain a market driver over the near term. Yet market disruptions of one sort or another are not uncommon throughout history, and free-market economies have shown time and again that they can adapt and progress. There’s no reason to believe this period will be any different.

1. https://www.cnbc.com/2025/05/09/chinas-exports-jump-us-tariffs-imports-tumble.html; 2. https://www.oaktreecapital.com/insights/memo/nobody-knows-yet-again; 3. https://www.cnbc.com/2025/04/11/heres-how-much-a-made-in-the-usa-iphone-would-cost.html#