Last Month in the Markets: January 31 – February 28, 2025

(source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis)

What happened in February?

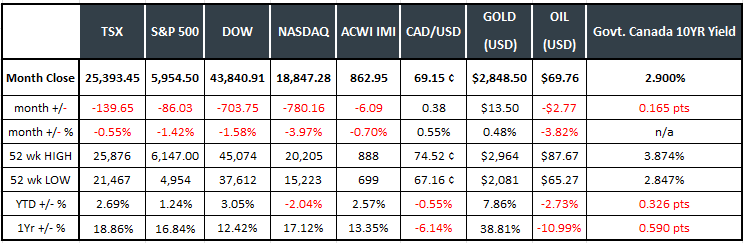

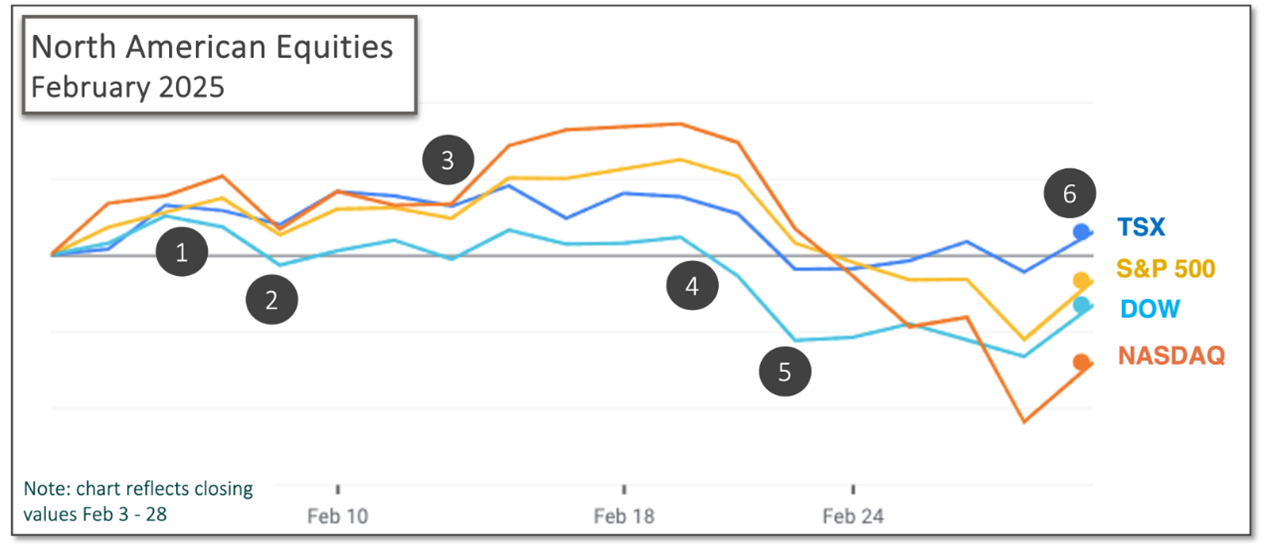

Equity performance during the second month of 2025 was weak. None of the indexes increased, and the NASDAQ lost nearly 4 per cent of its value. Despite February’s negative results, North American equity indexes have done reasonably well year-to-date, with the NASDAQ as the only exception.

The TSX sits atop the table over the past year with growth of almost 19 per cent. Its year-to-date performance is bettered by only the Dow, which is a narrow sample of 30 large U.S. corporates, while the TSX is more diverse.

The losses during February reflected the political uncertainty associated with President Donald Trump’s administration and its penchant for Executive Orders, many of which have generated a legal challenge and consternation in Congress, even among Republicans. One of the most consequential actions could be the introduction of import tariffs of 25 per cent on Canada and Mexico, despite the United States-Mexico-Canada Agreement (USMCA) trade treaty signed by Trump in his first term, and 10 per cent on imports from China. These moves were originally scheduled for early February and have been postponed until March 4. NYTimes article

Additionally, several economic indicators have shown that inflation progress and employment have not continued their improvements, which have moved markets. In February, the events and announcements included:

- February 3 – 7

Stocks moved downward at the beginning of the week, then regained value after U.S. tariffs on Canadian and Mexican goods were postponed for at least 30 days. Losses pushed the indexes into negative territory for the week. The downturn at the end of the week can be attributed, in part, to U.S. and Canadian government employment reports for January that were released as markets opened on Friday, February 7.

- February 7

StatsCan’s Labour Force Survey reported that employment increased by 76,000, which exceeded the expectation of analysts. The unemployment rate fell by 0.1 per cent to 6.6 per cent. Wages for permanent employees rose 3.7 per cent on a year-over-year basis. Wage rate growth is closely watched by the Bank of Canada as a leading inflation indicator. StatsCan release CBC and LFS

The U.S. Bureau of Labor Statistics released its Employment Situation Summary showing that nonfarm payrolls rose by 143,000 in January. Unlike Canada, this was below the expectation of 169,000 and significantly less than December’s 307,000. The unemployment rate in January lowered slightly to 4.0 per cent. The market has interpreted the less-than-stellar report as not weak enough to push the Federal Reserve (the Fed) back into rate cutting mode. CNBC and jobs

- February 12

U.S. inflation for January was higher than expected. After rising 0.4 per cent in December, the Consumer Price Index (CPI) increased 0.5 per cent in January. Over the past 12 months, the all-items index increased 3.0 per cent before seasonal adjustment. About 30 per cent of the month’s increase was attributed to the index for shelter. The energy index increased 1.1 per cent, and gasoline rose 1.8 per cent in January adding to rising inflation. Equity values moved downward after the Bureau of Labor Statistics release. Rising prices suggest that the Fed will delay interest rate reductions until the second half of 2025. CNBC and January CPI

The Bank of Canada released its summary of deliberations that resulted in a 0.25 point (25 basis points) reduction on January 29. The Bank indicated that a trade conflict with the U.S. would permanently shrink domestic Gross Domestic Product. Approximately 75 per cent of Canadian exports are sent to the U.S. and tariffs would reduce U.S. demand for Canadian goods. BoC deliberations CBC and BoC

- February 20

The 4 Nations Face Off concluded successfully for Canada when Connor McDavid scored in overtime against Team USA securing the inaugural championship.

The threat of U.S. tariffs has increased patriotism and consumer efforts to “buy Canadian”. The definitions of “made in Canada” and “Product of Canada” have become important according to a recent article in The Walrus.

- February 21

The nascent U.S. administration has introduced changes at an unprecedented rate, and concern by consumers and businesses that the U.S. economy will be negatively affected is increasing. Spending cuts at the federal level and the introduction of tariffs are two of the most concerning elements of change. Inflation expectations for consumers are also rising. As a result, small company stocks fell the most, and three-quarters of S&P 500 stocks declined. Stock pressures from Yahoo

The Fed released the minutes from its January 28-29 meeting that held interest rates steady. The committee noted that businesses would attempt to pass input cost increases to consumers arising from tariffs, and that inflation expectations had increased recently. The expectation for rising inflation continues to push the next Federal Reserve rate reduction further into the future, likely in the summer or autumn. A delay in rate cuts by the Fed places additional negative pressure on stock values. CME FedWatch tool FOMC minutes

- February 28

Canadian Gross Domestic Product (GDP) rose 0.2 per cent in December after declining by the same proportion in November. Fourth quarter Real GDP increased 0.6 per cent after rising 0.5 per cent in the third quarter. Overall household spending rose 1.4 per cent in the fourth quarter and 2.4 per cent in 2024. December GDP Q4 GDP

The quarterly earnings season concluded for S&P 500 companies with an average earnings gain of 18.2 per cent over the same period one year ago. It was the strongest growth since the fourth quarter of 2021. Financials posted an earnings gain of 56 per cent, the highest of all 11 sectors. FactSet Earnings Insight

The Fed’s preferred inflation indicator, the Personal Consumption Expenditures price index (PCE) rose 2.5 per cent in January from the same month one year ago, and core PCE that excludes food and energy increased 2.6 per cent. January’s performance was a slight improvement from December’s levels. BEA PCE release

What’s ahead for March and beyond?

The implementation of U.S. import tariffs and the responses from other nations on U.S. exports will continue to affect capital markets. Tariffs will deliver increased prices and lower economic output in the affected countries based on recent and historical instances of retaliatory trade wars. Investopedia and Trade Wars

Central banks, like the Bank of Canada and the U.S. Federal Reserve, will straddle the issue of inflation control and employment growth linked to economic output. It appears that rate reductions will be delayed based on current predictions, which may also negatively affect corporate performance.

The next two interest rate announcements in Canada and the U.S. are on March 12 and 19, respectively.