Last Month in the Markets: March 2 – 31, 2026

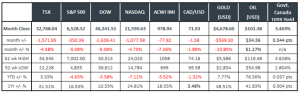

Index returns based on index value (source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis. Price returns are reflected)

What happened in March?

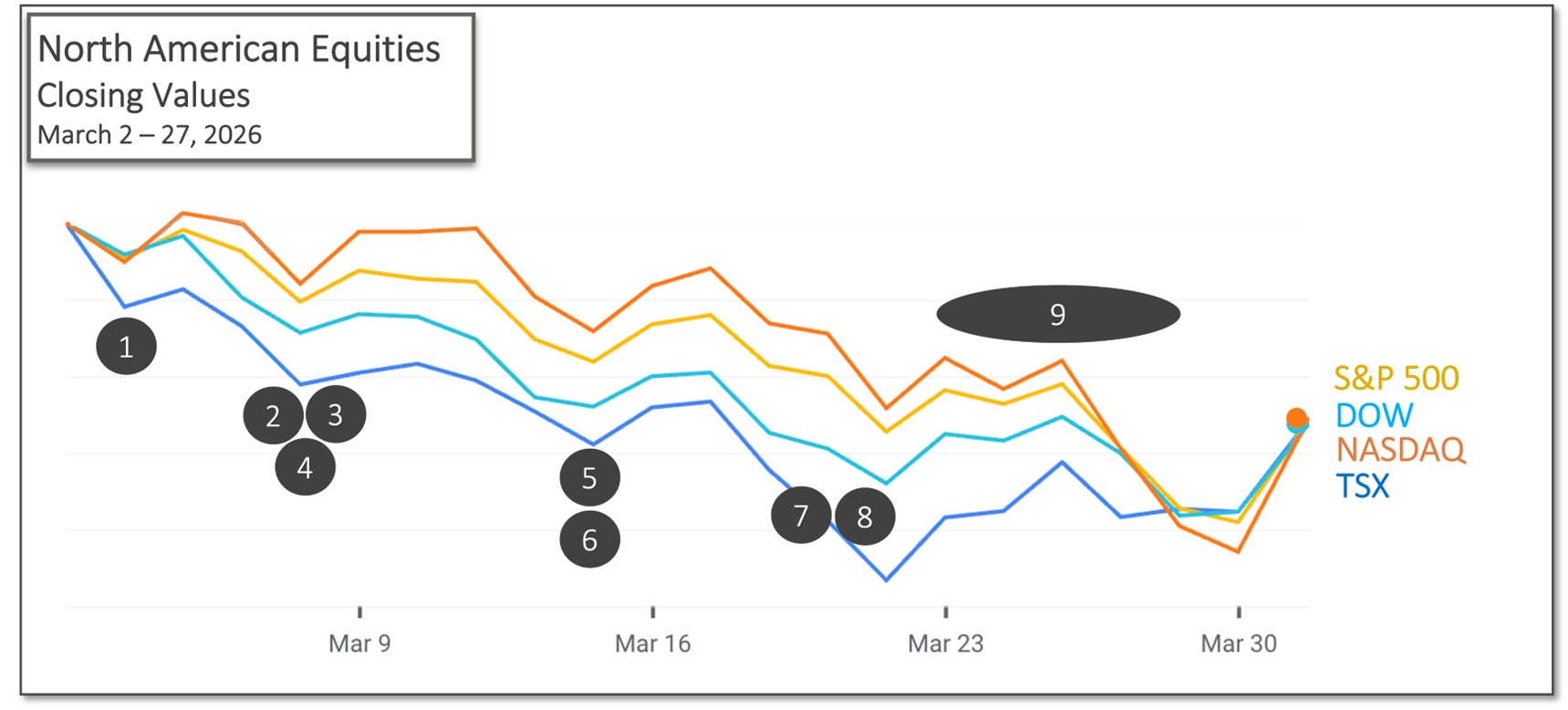

Market movements in March were heavily influenced by geopolitical developments following military conflict involving the United States and Iran that began at the end of February. Military action began prior to the opening of trading on March 2 and continued through the month. During the first three weeks of March, North American equity indexes declined between approximately 4.5 and 9 per cent.

On March 23, reports indicated that negotiations to end the conflict were progressing. Markets reacted quickly. Oil prices declined more than 10 per cent, gold fell 5 per cent, and equities rose approximately 2 per cent following the opening on March 24. These movements highlighted the relationship between uncertainty-driven commodity prices and equity markets. Progress toward reopening oil shipments through the Strait of Hormuz may influence oil prices and equity markets in the near term.

Political and military uncertainty contributed to elevated levels in the VIX Volatility Index.

(source: Bloomberg https://www.bloomberg.com/marketsand ARG Inc. analysis)

Events that influenced markets in March included:

- March 3 – Quarterly U.S. corporate results remained strong

Despite geopolitical uncertainty, a positive development for equities was the conclusion of the fourth-quarter earnings results for the S&P 500. 73 per cent of companies exceeded their earnings-per-share estimates and earnings growth was 14 per cent higher, the fifth consecutive quarter of double-digit growth. FactSet Earnings Insight

- March 6 – Oil prices rose and equities values declined

The price of oil rose more than 35 per cent in the first week of March to close at nearly $91 USD per barrel for the West Texas Intermediate (WTI) benchmark. Rising energy prices weighed on many equity markets, as higher input costs can affect corporate revenue and profit expectations. Higher energy prices may also contribute to inflation and could influence the timing of potential rate cuts by the U.S. Federal Reserve, the Bank of Canada, and other central banks.

- March 6 – U.S. employment declined

The Bureau of Labor Statistics announced in its Employment Situation Summary that “payroll edged down by 92,000 in February, and the unemployment rate changed little at 4.4 per cent.”

- March 6 – Canadian trade diplomacy continued

Prime Minister Mark Carney pursued additional trade discussions with India, Australia and Japan, with further bilateral economic integration under consideration. CBC and Carney trade deals

- March 13 – U.S. economy slowed in Q4 2025

U.S. Gross Domestic Product (GDP) grew just 0.7 per cent in the fourth quarter of 2025, according to the Commerce Department’s latest revision. The government shutdown contributed to slower economic growth. For the full year of 2025, GDP grew 2.1 per cent. CNBC and GDP

- March 13 – Canadian employment declined

Canada’s Labour Force Survey showed that employment declined by 84,000 in February, and the unemployment rate rose 0.2 per cent to 6.7 per cent. Employment fell in goods-producing industries by 28,000 and in services-producing industries by 56,000.

- March 13 – U.S. inflation remained below 3 per cent

The Bureau of Economic Analysis reported that the U.S. Federal Reserve’s preferred inflation indicator, the Personal Consumption Expenditures Price Index (PCE), increased 2.8 per cent year over year in January. Core PCE, which excludes food and energy, increased by 3.1 per cent. These figures are consistent with December’s levels. The rise in energy prices since the conflict began was not reflected in these figures. BEA PCE release

- March 18 – North American interest rates remained unchanged

The Bank of Canada held its overnight rate steady at 2.25 per cent, where it has remained since October 29, when the Bank reduced rates by 0.25 per cent. Canadian consumer inflation slowed in February, but Governor of the Bank of Canada, Tiff Macklem stated, “the sharp increase in global energy prices has led to increases in gasoline price, and this will push up total inflation in the coming months.” BoC release

The U.S. Federal Reserve maintained its federal funds rate in the range of 3.5 to 3.75 per cent after lowering it 0.75 per cent (75 basis points) from September to December 2025. The Chair of the U.S. Federal Reserve Jerome Powell stated, “near-term inflation expectations have risen in recent weeks, likely reflecting the substantial rise in oil prices caused by supply disruptions in the Middle East.” The U.S. Federal Reserve’s Summary of Economic Projections indicated that inflation forecasts have increased since December. FOMC meeting info

- March 19 – European Central Banks also held rates unchanged

The Governing Council of the European Central Bank kept its interest rates unchanged. Europe’s consumer inflation has been close to 2 per cent for a year, but higher energy prices related to the Middle East conflict are expected to push inflation above the 2 per cent target in the short term. ECB summary

- March 23 to 27 – Oil prices and U.S. equities moved inversely

During the last full week of March, oil prices and equities moved in opposite directions. As oil prices rose, equities declined, and as oil prices fell, equities improved. Reports of progress toward negotiations to end the conflict corresponded with a decline in oil prices and a rise in equity markets.

What’s ahead for April and beyond?

The relationship between geopolitical tension, reflected in energy prices, and capital markets may continue in the near term. Supply disruptions related to the Strait of Hormuz have drawn comparisons to past oil supply shocks, including the oil embargo imposed by the Organization of Arab Petroleum Exporting Countries in the 1970s.

If higher oil prices contribute to increased inflation, monetary policy expectations may shift. Prior to recent energy price increases, moderating inflation and slower employment growth had supported expectations for potential rate cuts by the Bank of Canada and the U.S. Federal Reserve. However, CME’s Fedwatch tool indicates that U.S. rate cuts may not occur in the near term, and Canadian rates are already below U.S. rates. Upcoming interest rate decisions will incorporate updated inflation data, including the effects of higher energy prices.

Higher inflation and slower economic growth may increase pressure for a resolution to the conflict. A de-escalation could reduce market volatility and geopolitical risk. Politico and risk with Iran

On April 1, Donald Trump delivered a 20-minute primetime address regarding the conflict. Following the address, oil prices rose approximately 10 per cent, illustrating the sensitivity of commodity markets to geopolitical developments. Oil prices following national address