Last Month in the Markets: February 2 – 27, 2026

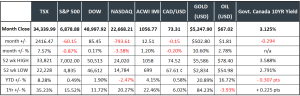

Index returns based on index value (source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis. Price returns are reflected)

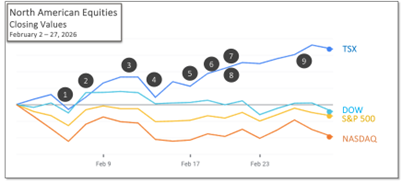

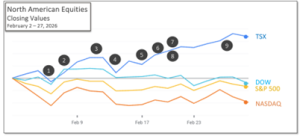

What happened in February?

(source: Bloomberg https://www.bloomberg.com/marketsand ARG Inc. analysis)

The events that influenced markets in February included:

1. February 5 – European Central Bank held rates unchanged

The European Central Bank left its three key interest rates unchanged. According to its monetary policy decision, “the outlook remains uncertain,” partly due to ongoing global trade policy uncertainty and geopolitical tensions.

2. February 6 – Canadian employment and U.S. employment data disappointed

According to the most recent Labour Force Survey, employment in Canada edged down in January by 25,000 (-0.1 per cent), and the employment rate declined by 0.1 percentage points to 60.8 per cent.

In the United States, unemployment data also showed some softening. In 255 of 387 U.S. metropolitan areas, the unemployment rate in December 2025 was higher than one year earlier. The national unemployment rate was 4.1 per cent, up from 3.8 per cent in December 2024.

In 255 of 387 U.S. metropolitan areas, the unemployment rate in December 2025 was higher than one year ago, according to the Bureau of Labor Statistics. National employment was 4.1 per cent, up from 3.8 per cent in December 2024. BLS Metro Employment Report – Dec 2025

3. February 11 – U.S. employment report showed moderate job growth

The U.S. Bureau of Labor Statistics (BLS) released its delayed Employment Situation Summary, “Total nonfarm payroll employment rose 130,000 in January, and the unemployment rate changed little at 4.3 percent.” For context, in 2023, 2024 and 2025, monthly job gains averaged 210,000, 122,000 and 15,000, respectively. CNBC and Employment

4. February 13 – U.S. CPI and corporate performance improved

The U.S. Consumer Price Index increased by 0.2 per cent in January, and rose 2.4 per cent on a year-over-year basis according to the release from the BLS. While inflation has moderated, the annual rate remains above the U.S. Federal Reserve’s long-term target of 2 per cent. CNBC and CPI

5. February 17– Canadian consumer prices eased slightly

Canada’s Consumer Price Index (CPI) rose 2.3 per cent year-over-year in January, down slightly from 2.4 per cent in December. Lower gasoline prices, which have fallen nearly 17 per cent since January 2025, were the largest contributor to the moderation in headline inflation.

Core inflation, which excludes food and energy, rose 2.4 per cent and continues to move gradually toward the Bank of Canada’s 2 per cent target. StatsCan and CPI CBC and CPI

6. February 19 – Trade balance data released amid tariff developments

The U.S. trade deficit totaled $901.5 billion in 2025, a modest decline of 0.2 per cent from the previous year. Trade policy developments also remained in focus after a U.S. Supreme Court ruling determined that the use of the International Emergency Economic Powers Act (IEEPA) to impose certain tariffs was unlawful. New tariffs of 10 per cent, later increased to 15 per cent, were subsequently announced under a different legislative authority. Trade Deficit releases SCOTUS decision

In Canada, the annual trade deficit widened to $31.3 billion in 2025, the largest since the pandemic. Exports to the United States declined by 5.8 per cent, while imports from the United States fell by 2.9 per cent. Canada’s trade surplus with the U.S. narrowed to $81.6 billion from $101.3 billion in 2024. NP and trade deficit

7. February 20 – U.S. GDP growth slowed in Q4

U.S. Gross Domestic Product grew at an annualized rate of 1.4 per cent in the fourth quarter of 2025. Economic growth came in below expectations, with government spending temporarily declining during the U.S. government shutdown. CNBC and GDP

8. February 20– U.S. inflation indicator rose slightly

The U.S. Federal Reserve’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) Price Index, rose to 2.9 per cent year over year in December. BEA and PCE

9. February 27 – Canadian GDP declined in Q4

Canadian real gross domestic product (GDP) declined 0.2 per cent in the fourth quarter of 2025 after rising 0.6 per cent in the third quarter. The decline was partly attributed to weaker export activity. StatsCan GDP release

What’s ahead for March and beyond?

February ended with reports of coordinated military strikes by the United States and Israel targeting Iranian leadership and nuclear-related infrastructure. Iran subsequently responded with attacks on U.S. and Israeli interests across the region.

Markets reacted quickly at the beginning of March. Gold and oil prices rose sharply on the first trading day of the month. North American equity markets were relatively flat on March 2 before declining at the open the following day.

In the medium and long term, inflation, employment trends, economic growth, and monetary policy will continue to influence financial markets. In the near term, developments in the Middle East and their potential impact on energy supply and prices may play an important role.

The VIX Volatility Index, which measures the market’s expectations of near-term price changes in the S&P 500, has also risen. Market volatility may remain elevated while the geopolitical developments continue to evolve.