Market commentary

Following one of the worst months in years, April delivered the S&P 500’s strongest monthly return since November 2020. With the benefit of hindsight—post-recovery and back to new highs—this volatility can look like much ado about nothing. However, based on the dozens of calls we fielded in March, bouts of volatility have a very real impact on investor psyche. Anything that erodes confidence has the potential to derail long-term strategies. That’s precisely why our investment approach is designed to dampen volatility. Statistically, smoother returns improve the probability of meeting a return objective, in part because they reduce the importance of timing. The smoother the return path, the less likely you are to invest immediately before—or after—a major market event. And the easier it is to forecast returns, the easier it becomes to plan a lifestyle around the portfolio.

April was an impressive month for portfolios, outperforming benchmarks by a healthy margin. To recap: we captured substantially less of the downside in March and meaningfully more of the upside in April. Some might call that the Holy Grail!

Despite one of the most tenuous geopolitical environments I can recall, economic growth remains resilient and equity markets continue to deliver strong returns. It behooves investors to look past the headlines and consider whether positive changes are unfolding beneath the surface—changes that may not be reflected in the daily news cycle. There are structural shifts underway in the global economy that are difficult to quantify. The impact of artificial intelligence (AI), for example, is likely to be significant, but also hard to measure in real time. Many have argued that valuations are stretched, but the reality is that returns have been among the strongest in history. We understand the world can feel uncertain, but change often produces prosperity rather than hardship. It’s possible we’re on the cusp of a period of meaningful positive transformation, and markets appear to be reflecting that possibility. As investors, it’s incumbent upon us to participate in that growth. At the same time, with meaningful change comes meaningful risk—so we seek only as much exposure to risk as is necessary.

Striking that balance isn’t easy, but it’s exactly what we focus on every day.

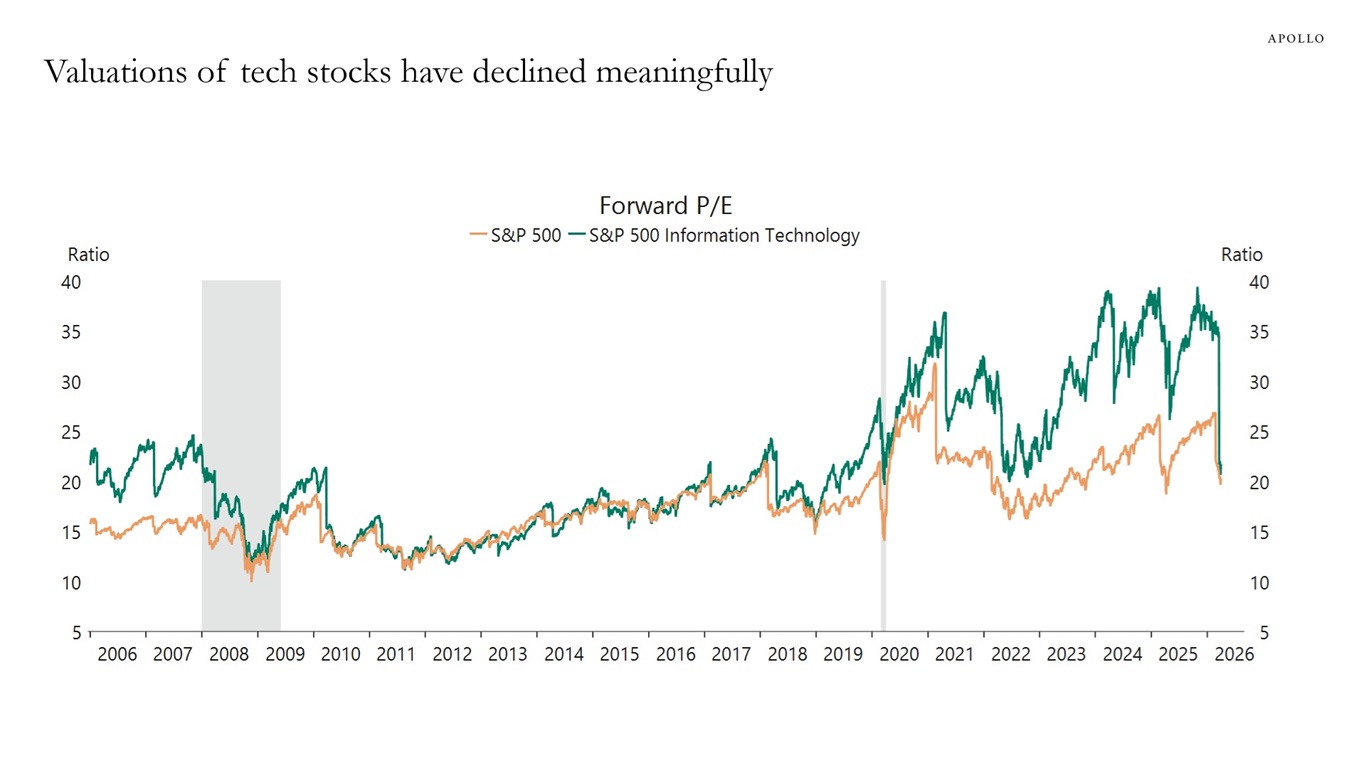

Chart of the month:

Tech Valuations Back to Pre-AI Boom Levels | The Daily Spark

The March sell-off was most severe for tech companies. That drop in price as earnings continued to grow impressively led to valuations plummeting. That valuation-check eased a major concern we have held for several months, leaving us with more reasonable valuations on the best companies around and a more balanced market.

Content recommendation: Blackstone Q2 market views

Jon Gray breaks down Blackstone’s portfolio and provides sage advice on staying the course in today’s volatile environment.

How Blackstone Is Thinking About IPOs, Hard Assets & AI Investing | Jon Gray’s Market Views Q2 2026

Portfolio strategy

Debt

Liquid fixed income

- Government bond yields have spiked around the world.

- The U.S. 30-year treasury yield is 5.17%, its highest in a quarter century.

- Traditional bond strategies have high sensitivity to long-term interest rates; accordingly, they have had a rough run.

- Our portfolio has minimal government debt exposure and a low sensitivity to rising rates. It has performed comparatively well.

Private credit

- Yields seem likely to stay higher for longer, helping preserve strong payouts from private loans.

- Defaults have been rising, so manager and portfolio quality are paramount.

- We reduced exposure nearly a year ago, currently underweight and very high quality.

Equity

Public equity (stocks)

- For all the hype and concern about AI and tech stocks, boring international equity markets have delivered better returns than the tech-heavy S&P 500 year-to-date (10.7% vs. 7.4%).1

- The addition of an active Fidelity equity fund in February has yielded outstanding returns for Growth and Balanced mandates.

Private equity

- Strong returns in March continue the trend of enhancing diversification, smoothing returns and providing additional upside potential.

- Initial Public Offering (IPO) activity is ramping up (see Blackstone video from the content section).

Real Assets

Real estate

- Portfolios contain only minimal real estate exposure through a small allocation in Apollo Aligned Alternatives.

- Returns seem to be improving, but on balance, we see better opportunities in infrastructure.

Infrastructure

- Energy, defence, data centres, transportation, are all durable, persistent growth themes globally.

- Inflation is rising. Infrastructure historically performs very well during periods of high inflation.