Market commentary

May was another blockbuster month for public markets, with both stock and bond markets delivering impressive gains. Client portfolios responded in kind with a third straight month of outperformance. This is notable because portfolios have substantially less public equity (stocks) exposure than their respective benchmarks. Our active equity managers have produced outstanding returns, driven mainly by strategic investments in artificial intelligence.

Many of our conversations over the years have centered around U.S. politics. I think it’s safe to say there’s not much love for President Donald Trump. That said, the growth index (80% stocks, 20% bonds) is up roughly 30% since his election. Had an investor sold after his election (as some clients inquired about), they would have missed an epic run of returns. That’s all to say: it’s possible to dislike the politics and still benefit from the markets at the same time. AI, defense, and government stimulus are outweighing political concerns in the market’s weighing mechanism.

Personal computers and the internet led to one of the greatest bull markets of all time through the ’80s and ’90s. That period was not without geopolitical and market disruptions, but the productivity benefits of these technologies proved transformational. Although this era of exceptional returns ended with the tech bubble bursting in 2000, the total return over those 20 years was approximately 1,000%, or about 12% annually.1 Investors should not allow the fear of selloffs to prevent participation in potential exceptional long-term returns. Of course, we structure portfolios to navigate deep drawdowns, but avoiding this market out of fear could continue to be a costly mistake.

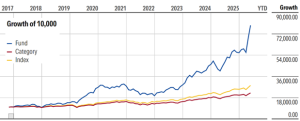

Chart of the month: Fidelity Global Innovators Fund

Only about 10% of public equity managers actually beat the market. Part of the problem is that many are what we call “closet indexers,” meaning their portfolios closely mimic the index they are measured against. Once fees are added, it’s little surprise that a portfolio holding largely the same stocks underperforms over time. As the saying goes, “an expensive index fund will always underperform a cheap index fund.” Most of our exposure to stocks is through very low-cost index funds that benefit from owning the entire haystack, along with low fees and strong tax efficiency. When we allocate to an active manager, we look exclusively for someone who can do what we can’t get essentially for free—finding the needle in the haystack. In early February, we allocated to the Fidelity Global Innovators Fund. Based on the hockey-stick-shaped chart and the ~35% return since purchase, we seem to be getting something that an index fund can’t deliver.

Content recommendation: Exceptional earnings!

Fundamentally, a stock price should be a direct function of the earnings that company generates and its future earnings potential (i.e. growth). So, when people ask how stocks could be charting such impressive returns right now, I point to the unprecedented corporate earnings. Click on the link for graphs and commentary on the most recent earnings season.

“The numbers are unbelievable. Four sectors are on pace to grow earnings by over 39%.”

Portfolio strategy

Debt

Liquid fixed income

- Government bond yields have stopped climbing but remain volatile and elevated.

- Our portfolio recovered nicely during May, well positioned to benefit from slightly higher yields.

Private credit

- The media seems to have become bored with the private credit redemption story (which was never very interesting or worthy of so much attention anyway).

- We reduced exposure nearly a year ago, currently underweight (almost none in Growth portfolios) and very high quality.

Equity

Public equity (stocks)

- May delivered another stellar month for stock markets.

- Amazingly international stocks outperformed U.S. stocks by a substantial margin.

- Large initial public offerings (IPOs) of SpaceX and Anthropic in coming months will be interesting.

- The addition of an active Fidelity equity fund in February has yielded outstanding returns for Growth and Balanced mandates.

Private equity

- What’s better than buying the biggest IPO in history (SpaceX)? We believe already owning it for years and earning outstanding returns via a private equity fund.

- Private equity portfolios own a diversified mix of boring but profitable value-oriented companies along with some of the fastest growing companies ever.

- Capturing exponential growth before companies go public seems to be increasingly important.

Real Assets

Real estate

- Portfolios contain only minimal real estate exposure through a small allocation in Apollo Aligned Alternatives.

- Returns seem to be improving, but on balance, we see better opportunities in infrastructure.

Infrastructure

- Energy, defence, data centres, transportation, are all durable, persistent growth themes globally.

- Inflation is rising. Infrastructure historically performs very well during periods of high inflation.