This may sound familiar: your first home started out small, but as your family grew, you needed more bedrooms and a larger backyard. Now the children have left the home, and those bedrooms sit empty — but over the years, rising housing prices may have helped you build significant equity in your home. Perhaps you’re asking: Is there an opportunity to “rightsize”?

This may sound familiar: your first home started out small, but as your family grew, you needed more bedrooms and a larger backyard. Now the children have left the home, and those bedrooms sit empty — but over the years, rising housing prices may have helped you build significant equity in your home. Perhaps you’re asking: Is there an opportunity to “rightsize”?

Downsizing can provide financial advantages by unlocking home equity and reshaping both lifestyle and financial flexibility. A smaller home typically reduces maintenance, utilities and property tax bills, while freeing capital for other priorities. Accessing home equity may help strengthen retirement cash flow, support family members or fund new goals.

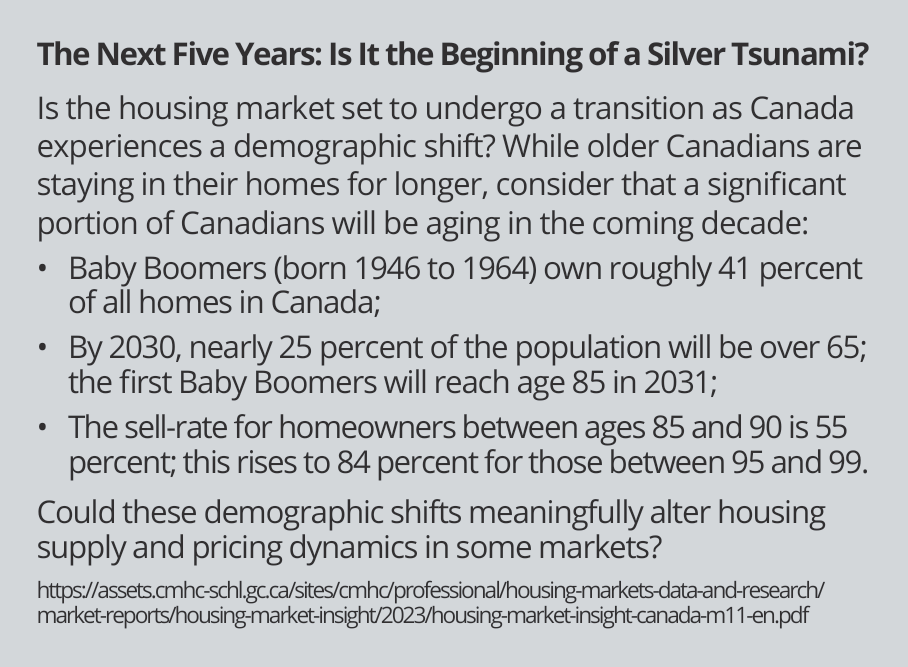

However, fewer people are choosing to downsize. Many prefer to remain in their homes as long as possible. A recent survey found that among those 65 and older, just 16 percent plan to downsize in the next decade, while 57 percent wish to remain in their current home.1

This shift reflects broader changes in housing economics and retirement planning. In the past, homeowners more commonly viewed real estate as a retirement resource. Today, that assumption is less prevalent. Longer life expectancy, improved health in later years and higher overall wealth have contributed to a greater ability to remain in place. At the same time, rising real estate costs, including seniors’ housing, have reduced the net financial benefit of downsizing, limiting the equity released.

Several other factors may also influence the decision:

Emotional impact. Downsizing is not purely financial. Long-time homes are often tied to memories, routine and identity — factors that can delay decisions long after the financial case becomes clear.

The cost of moving. Selling expenses, including legal fees and commissions, can account for a meaningful portion of proceeds. Preparing a home for sale (including staging or repairs) adds further expense, as do moving costs and updates needed to settle into a new property. The process itself can create administrative complexity and require a substantial time commitment.

Market uncertainty. Limited inventory has made it difficult for some homeowners to find a suitable replacement property, while market price fluctuations can affect what a sale will ultimately yield. In many markets, prices have shifted from their highs, making the sale of an existing home less attractive.

Trade-offs in housing flexibility. Moving to a rental or community setting may reduce maintenance responsibilities but can introduce uncertainty around lease terms, fees and future cost increases. Ownership typically provides greater control and predictability.

It’s Not Just a Financial Decision

Yet the decision to downsize isn’t simply a financial one. As life circumstances evolve, including changes in energy, health and mobility, the question often shifts from whether downsizing is financially optimal to whether a current home still fits day-to-day life.

Those who successfully transition tend to act proactively, motivated by what their next home offers, whether it’s simplicity, convenience or a better lifestyle fit. A recent Globe and Mail article suggested that the best time to plan a downsize is “when you’re still excited about what comes next.”2 The argument is straightforward: it’s better to decide on your own terms, before health issues or practical limitations force the issue. Waiting too long can mean the choice is driven by necessity rather than preference, often under pressure from family members or advisors.

Start Early

As with any major financial decision, planning is important. Take the time to explore your options before circumstances force the decision. If you’re considering relocating to a new community, city or province, spend time there during different seasons to understand what day-to-day life might look like. If you’re thinking of moving abroad, understand the tax, healthcare and residency implications. For condo living, review bylaws and restrictions carefully; details like pet policies or renovation rules may significantly affect your experience.

A thoughtful approach allows you to weigh both the financial and lifestyle implications before making a decision. While “rightsizing” your home may mean it becomes smaller, the opportunities ahead can expand in meaningful ways.

1.https://www.bnnbloomberg.ca/business/real-estate/2026/05/03/not-the-right-time-retirees-delay-downsizing-plans-as-housing-market-slumps/

2.https://www.theglobeandmail.com/investing/personal-finance/article-what-is-the-right-age-to-downsize-your-home-its-all-about-timing/