Fasten Your Seatbelts

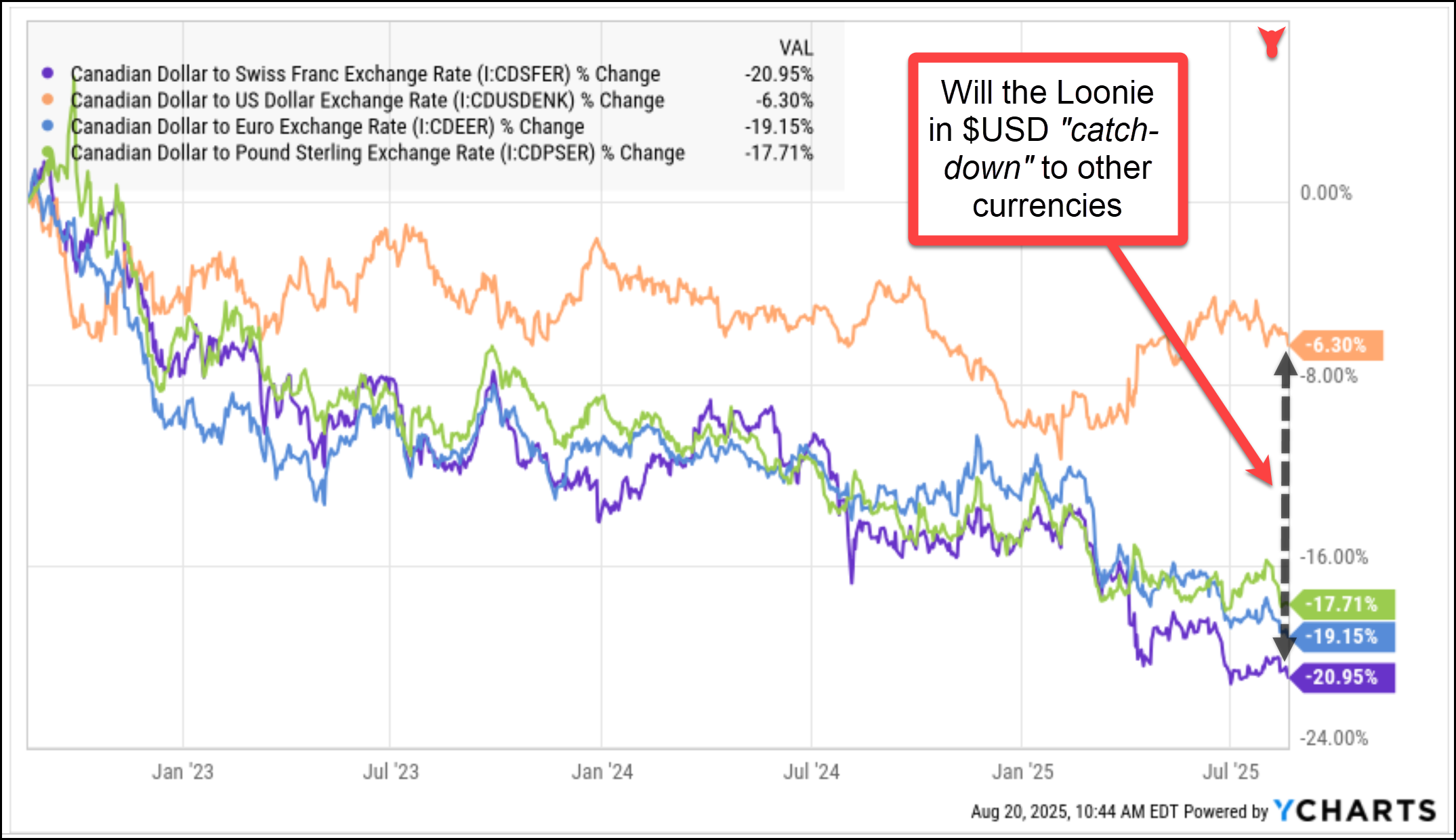

Against the euro, pound, and Swiss franc the loonie has already lost altitude (chart below). Only against the U.S. dollar has it seemed to hold steady since President Donald Trump’s election, but appearances can be deceiving. If CAD-USD “catches down” to the global trend, Canadian investors should be braced for turbulence.

Every flight has some bumps, and here is the good news: Canada still has time to act, and investors have tools to protect and grow their wealth while policymakers find their footing.

YCharts.com © 2025 YCharts, Inc. All rights reserved

Why the Loonie Faces Pressure

Canada’s fiscal picture is worsening, with projected deficits of 75 to 100 billion dollars. That would be concerning in any context, but paired with mounting trade friction it raises the stakes. The government has chosen a bold path, but in doing so it has also created irritants in Washington. From supporting Palestinian statehood to pursuing free trade talks with Brazil and other countries in Mercosur, in negotiations, timing matters.

By contrast, Mexico has kept its focus tightly on trade deliverables and security cooperation, and has been rewarded with concessions. The comparison is uncomfortable: if Mexico can make headway with Washington despite far greater border and fentanyl problems, why can’t Canada? Is it personalities, or trade negotiation skill? Canadians are right to expect prompt action.

We continue to believe that if Prime Minister Mark Carney can steer Canada through this turbulence—defending trade access, securing fiscal credibility, and unlocking stalled energy projects—he has the chance to go down as one of the country’s most consequential leaders. But patience is wearing thin, and the risks are rising.

Housing Correction Deepens

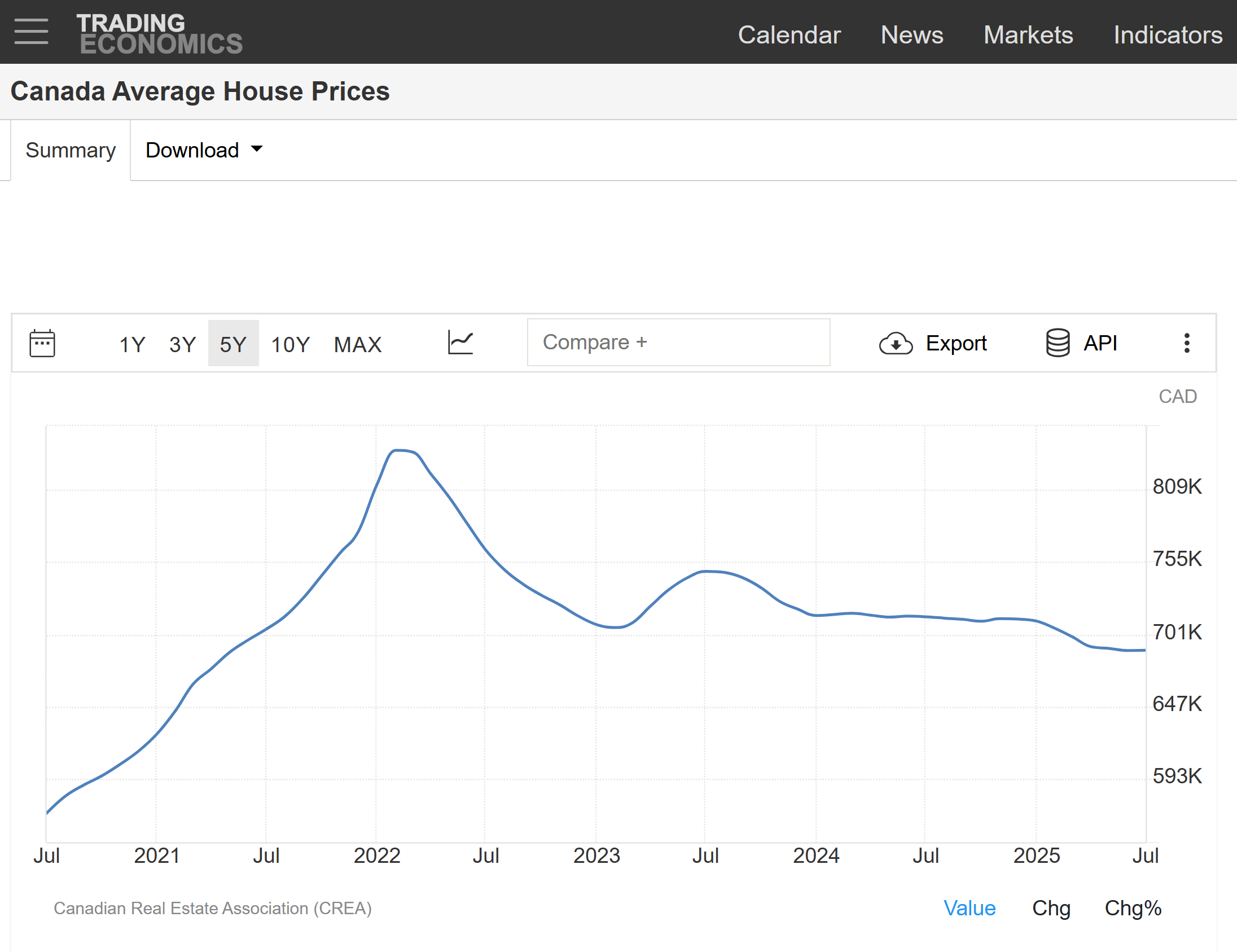

The national average home price peaked near $837,000 dollars in early 2022. Today it stands near $689,000 and trending lower. That is a 17.7% decline before adjusting for inflation. Canadian banks have so far looked resilient, thanks to strong capital buffers and mortgage insurance that delayed the pain. Renewals and rising insolvencies will test that resilience in the year ahead.

YCharts.com © 2025 YCharts, Inc. All rights reserved

Banks: Strong Past, Cautious Future

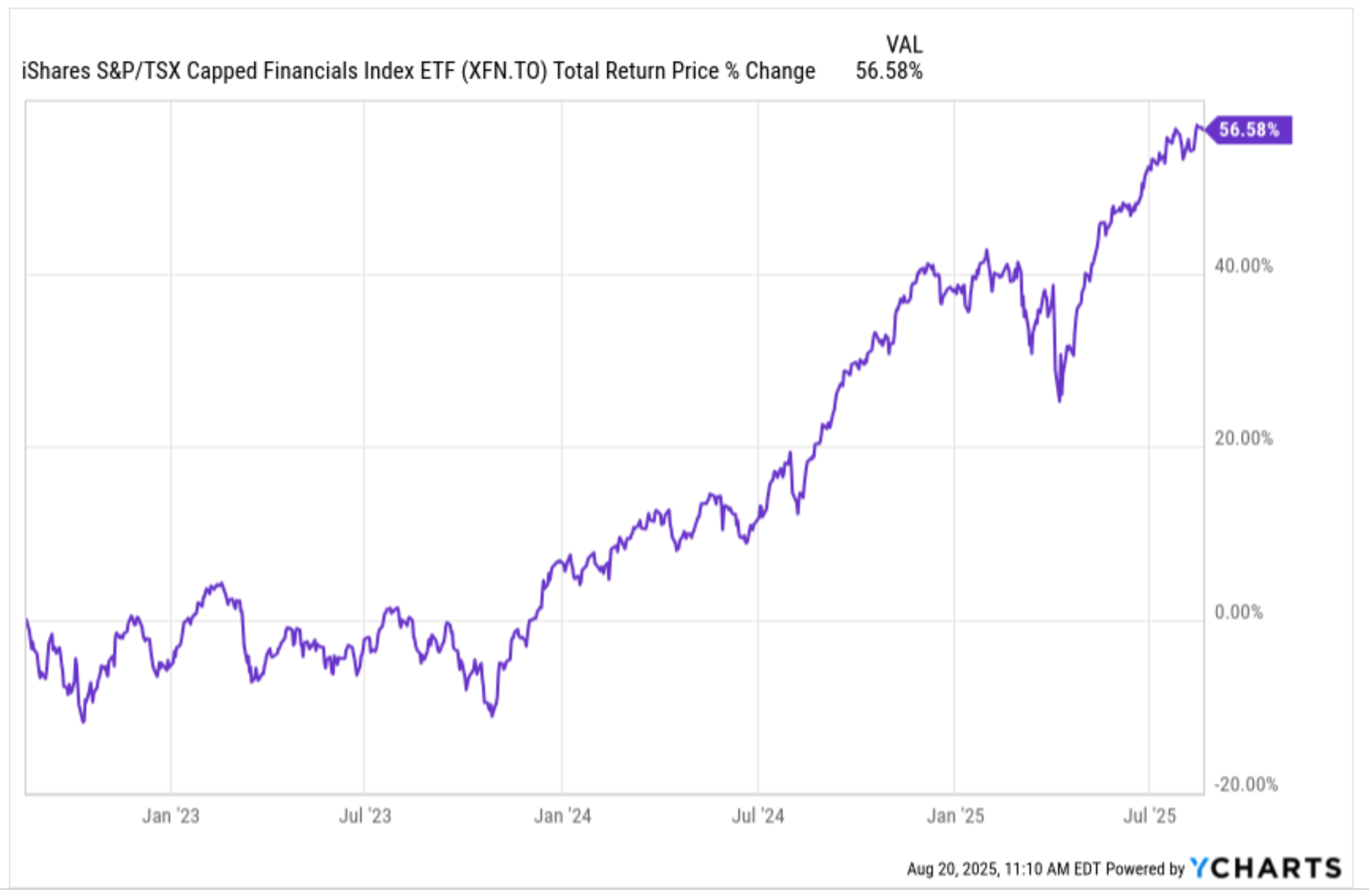

Canadian banks have been stellar performers in the past three years. The S&P/TSX Capped Financials Index (XFN) is up 56%. Almost all of those returns came in the past 18 months. The drivers were wide spreads, low credit losses, and steady loan growth. Investors need to ask if those trends will persist.

The good news is that banks remain well capitalized and their long term franchise value is intact. The caution is that the easy gains are likely behind us. If Canada tips into recession while trade frictions linger, banks will face slower loan growth, higher provisions, and earnings pressure as the Bank of Canada reduces interest rates as the economy weakens. This is not 1992 or 2008, but it is likely to be a period where stock picking matters more than index exposure.

YCharts.com © 2025 YCharts, Inc. All rights reserved

Energy and Commodities: Bright Spots Amid Turbulence

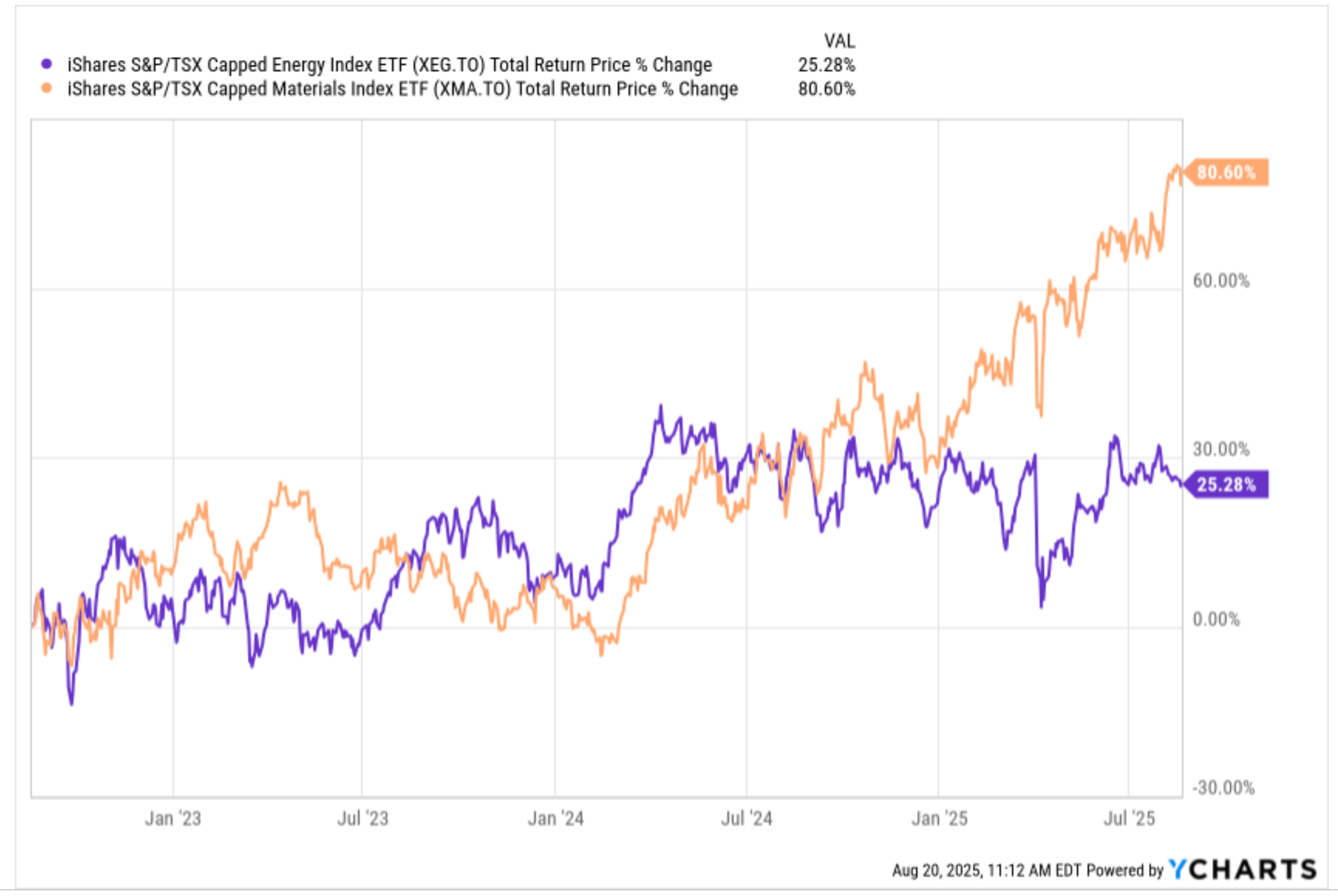

Energy and metals remains Canada’s strongest card (see chart above). Canadian producers sell into U.S. markets in U.S. dollars while paying many of their costs in Canadian dollars. A weaker loonie boosts their margins. After three years of underperformance oil companies are lean and disciplined. If U.S. shale supply slows further Canadian producers are set to benefit.

Base metals are more complicated. China still represents half of global demand for copper and aluminum, and its slowdown is a headwind to base metal demand. At the same time U.S. onshoring and grid build out are creating new demand for Canadian inputs, though on a slower timetable.

Agriculture is even tougher. China’s restrictions on Canadian canola are a clear headwind and will remain so until trade relations improve.

The lesson is simple: stay overweight in energy and U.S. anchored exporters, stay selective in base metals, and underweight in Canadian agriculture until the policy winds shift.

Could the Loonie Fall Further?

In 2002, the Canadian dollar touched 62 U.S. cents (see chart above). The mix was similar to today: fiscal drift, U.S. outperformance, and weak commodity investment. If tariffs remain in place, deficits swell past 100 billion dollars, and the Bank of Canada cuts aggressively, the loonie could revisit that zone. Recession would cut tax receipts, worsen deficits, and risk corporate flight south where U.S. tax incentives and permitting are more competitive.

Investor Playbook: Hedge and Diversify

Even if Ottawa takes time to deliver results, investors can still position for opportunity. Holding U.S. equities unhedged converts a currency problem into a return engine. Equity performance combines with a currency tailwind if the loonie weakens. Canadian energy and exporters with U.S. dollar revenues are natural hedges inside domestic portfolios. Banks should be approached selectively rather than as an index bet.

How Canada Can Regain Momentum

There is still time to avoid the worst case. Rebuild fiscal credibility with a transparent anchor. Prioritize Washington before Brasilia or Brussels. Streamline project approvals so that Canada can capitalize on the global LNG and oil cycle rather than watching from the sidelines. Support productivity growth to stem the migration of investment to the U.S.

Risks and Opportunities Ahead

Canada faces real risks and Canadians are right to expect prompt action. The good news is that the future is still in our hands. If Carney can deliver, he has the chance to go down as one of Canada’s greatest leaders. For investors, the way forward is clear: diversify into the U.S., lean into energy and exporters, and take a selective approach to banks.

Watch the Video: Turbulence Ahead

Want to hear Glen’s take in more detail? Check out our latest video on YouTube and subscribe to stay up to date.

Glen