Buttoning his cardigan and sitting down in front of a crackling fire, President Jimmy Carter addressed the worried nation—the energy crisis was ongoing and sacrifices would have to be made.

source: Gemini

A New Global Energy Crisis is Unfolding

Last week Australia’s Prime Minister Anthony Albanese was smart enough not to wear a cardigan when he addressed Australians about the crisis and sacrifices that are coming down under, “the months ahead will not be easy”, he warned. Albanese inherited an Australia that closed six of its eight refineries, let reserves fall to 37 days, (the lowest of any IEA member nation) and now imports 80-90% of its refined fuel from Asian refineries that get their crude through the very strait that Iran has shut.

source: Gemini

How Supply Shortages are Hitting Europe and Australia

The Libyan-flagged Maetiga docked in the U.K. last week carrying jet fuel from Saudi Arabia. It is the last known shipment of jet fuel from the Middle East to the United Kingdom. No other U.K.-bound cargoes are visible on the water. Britain now has just four operating refineries, compared to seventeen in the 1970s.

The tankers arriving in Australian ports this week were loaded before the war started. By late April, when the pre-war inventory in Asian refineries is exhausted, Australia will discover what 37 days of reserves actually feels like.

While markets cheer the apparent beginning of the end of hostilities, the world has a period of pain ahead. It’s hard to understand how dramatic the shortages are. For reference, let’s recall that the biggest oil shock was the Suez Canal. The 1973 Arab Oil Embargo was only 90% as bad. So how does this stoppage compare?

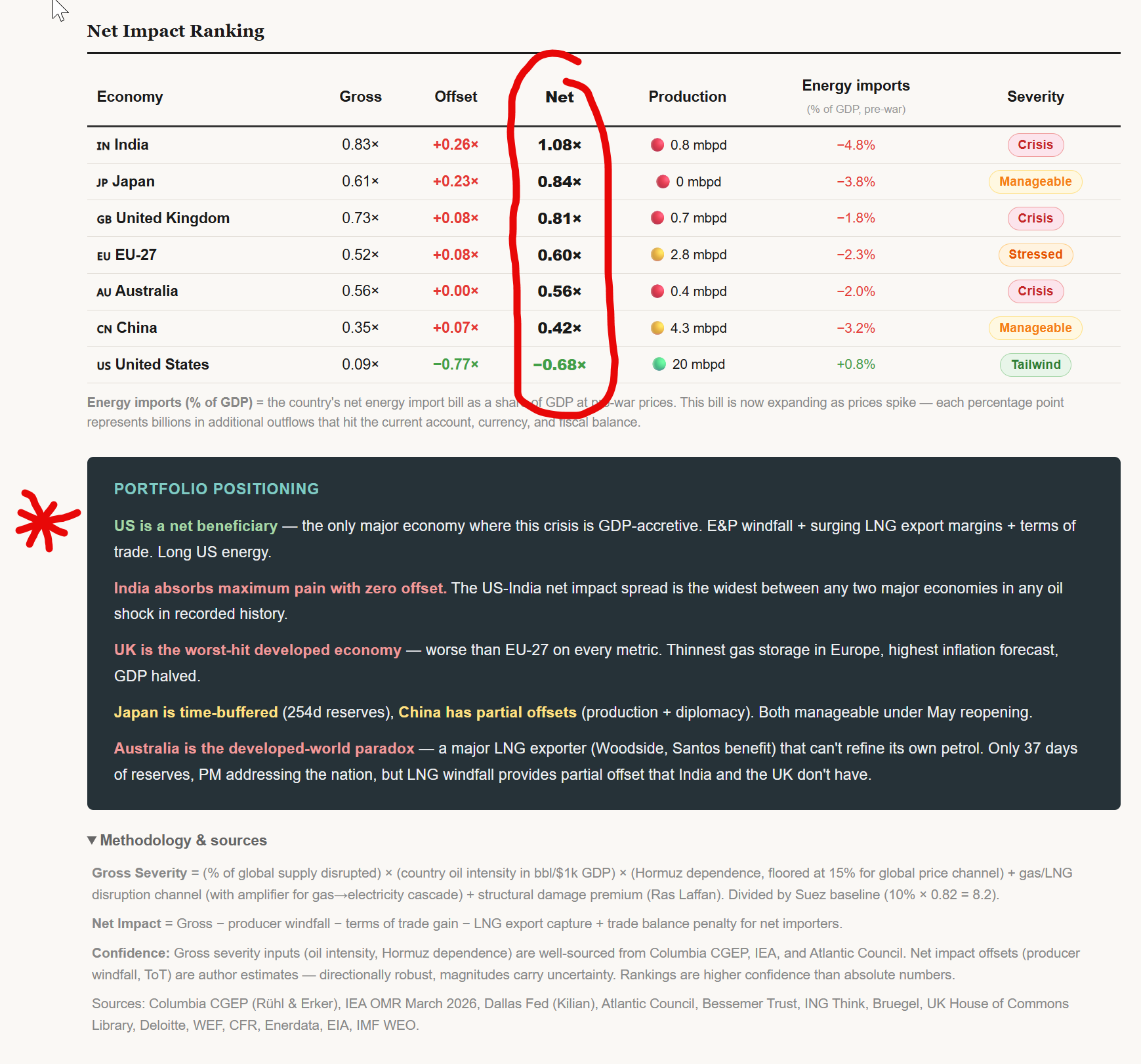

I had Anthropic’s Opus 4.6 research the order of magnitude of the current shortage compared to the Suez Canal. I’ve circled the Net Impact—India’s situation is 1.08 times as big as the Suez Crisis. The U.K. and Australia are among those countries for who this shortage will create a crisis. (By the way, the longer this persists, the worse the outlook. Now look at the United States.)

Why the U.S. is Winning the Energy Crisis

The United States now produces nearly 24 million barrels per day of petroleum liquids more than any country in history, (source: EIA) and is a net energy exporter. Its LNG producers are capturing Qatar’s European market share at record margins. Its shale operators are printing money at $100 WTI on a cost base of $40-50. Our severity index, (which adjusts each economy’s exposure for the actual oil and gas intensity of its GDP, then nets out producer windfalls and terms-of-trade effects), shows the U.S. as the only major economy that is a net beneficiary of this crisis. President Donald Trump is unlikely to be wearing a cardigan when he addresses the nation any time soon.

Energy Security and the Shift in Global Power

Ponder this reality for a few minutes and you begin to understand the implications. Energy rationing is already reported in many countries. IEA head Fatih Birol said this week: “In many countries the rationing of energy may be coming soon.” He warned that “the next month, April, will be much worse than March” because the tankers still arriving were loaded before the war—”in April, there is nothing.”

Last year saw investors preferring European and International investing over the U.S. The expectation that Europe was going to re-arm to equip NATO and re-industrialize made them an attractive bet. This energy crisis likely cripples the European re-industrialization hopes.

What the 2026 Energy Crisis Means for Investors

Investors are relearning the lesson I’ve repeated many times: “energy is life”. Without cheap and plentiful energy society does not flourish. Investments will migrate to where the energy is. For the near term that’s the U.S. (and Canada). Broadly speaking this fits into our Cold War 2.0 thesis about Bits and Atoms. Technology and the metals, minerals and energy to create it is the opportunity.

The caveat is that this energy shock will have global and diverging impacts. I expect more volatility, a reset in some markets (that might already be nearing the end) and a period of consolidation as the bulls step back in.

The crisis in the Persian Gulf might be getting closer to resolution—but the tsunami it created will continue to land on shores around the world for the next several weeks and months.

Glen