In 1865, Britain was powered by coal, enriched by steam, and quietly haunted by the fear that the fuel driving its rise might someday run out.

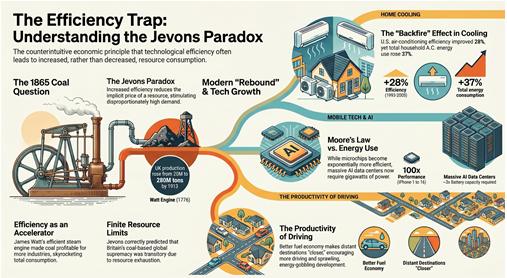

Into that anxiety stepped economist William Stanley Jevons with an unsettling argument. Common sense said more efficient steam engines should reduce coal use. Jevons saw the opposite. If coal-powered industry became cheaper to run, Britain would not burn less coal. It would build more factories, lay more rail, smelt more iron, and consume more of the very resource people assumed efficiency would conserve.

What is Jevons Paradox and Why it Matters for AI Investing

Jevons’ Paradox is the idea that greater efficiency can lower costs and expand use, causing total demand to rise rather than fall. In many ways, that was also the story of 20th-century finance: cheaper access created more participation, not less.

For investors like you and me, especially those in or near retirement, the debate is simple to state and hard to answer: will AI’s disinflationary productivity boom arrive before an energy-and-materials squeeze pushes the economy into another inflationary shock? The optimists think cheaper intelligence wins first. The scarcity camp thinks the physical world gets its say before the software miracle can fully pay off.

AI Investing Debate: Abundance vs Scarcity

The debate is not whether AI brings abundance. It is whether the road to abundance first runs through scarcity.

Our view is straightforward. Long term, we lean toward abundance. Short term, we think the road may still run through scarcity, especially in energy. And for investors, that timing could make all the difference.

The Optimist View: Why AI Could Lower Inflation

On one side sits the U.S. Federal Reserve Chair nominee Kevin Warsh and the broader AI-optimist camp. Their case is simple: AI makes intelligence cheaper. It lowers the cost of code, analysis, design, logistics, customer service, and decision-making. That lifts productivity, eases cost pressures, and, in Warsh’s view, should bring inflation down sooner rather than later.

It is a compelling story, and long term we lean that way. AI has a real chance to become a genuine productivity shock. Warsh may be right about the destination.

The Scarcity Case: Energy, Materials, and Rising Demand

On the other side sits the scarcity camp. Voices like Australian analyst Craig Tindale matter because they force investors to confront an old truth: software still has to live in the physical world. Their argument is not that AI is fake. It is that the market is underestimating what it takes to build and power this next phase of the digital economy. Data centres do not run on optimism. Chips do not appear because venture capital is excited. Grids do not upgrade themselves.

Tindale’s point is that AI may not be disinflationary at first. It may be inflationary. The more AI is used, the more compute is needed. The more compute is needed, the more pressure falls on electricity, transmission, transformers, cooling, metals, refining, processing, chemicals, and logistics. Chinese export controls and a mounting energy crisis caused by the closure of the Strait of Hormuz magnify Tindale’s concerns.

Jevons Paradox AI Investing in Action

This is where Jevons comes back in. He does not refute the optimists. He explains why they may be right and why investors can still get hurt along the way. If AI makes intelligence cheaper, that can broaden adoption and increase strain on the system behind it. The AI boom may be disinflationary at the application layer while inflationary upstream, where the atoms live.

Warsh thinks cheaper intelligence brings inflation down. Tindale thinks scarcer energy and materials push it up first. Warsh may be right about the destination. Tindale may be right about the road.

So who’s right? Why choose?

Long term, we lean toward Warsh. Short term, we lean toward Tindale. We think AI is likely to be a powerful disinflationary force over time, but the road there may still run through scarcity, especially in energy. And energy is everything. It sits inside fertilizer, solvents, pharmaceuticals, weed control, industrial gases like helium, and the etches and processes that sit upstream of AI hardware itself. When energy tightens, the whole system feels it.

Market Valuations and the Risk of Mispricing the Future

Also worrisome is how richly valued markets remain by traditional measures like the Shiller P/E ratio shown above. Outside the Tech Bubble, valuations have rarely been this stretched. At a minimum, that suggests the market is pricing something closer to Warsh’s smooth disinflationary future than Tindale’s scarcity-driven squeeze.

That matters because timing matters. If the scarcity camp is right over the next 12 to 36 months, the road to AI abundance may still run through weaker growth, policy stress, and a recession scare, none of which looks fully priced into markets today. That does not kill the long-term AI story. It simply reminds us that being right eventually is not the same as being positioned correctly now.

Positioning Portfolios for Both AI and Energy Trends

So the answer is not to pick one camp and ignore the other. It is to own both sides of the argument with your eyes open: the bits and the atoms. We want exposure to the businesses that benefit if intelligence gets cheaper, and to the physical layer that becomes more valuable when power, materials, and resilience matter more.

At Evans Family Wealth, we think the future still belongs to the optimists, but we intend to travel there with our eyes open.

Glen