“Every day begins with an act of courage and hope: getting out of bed”

-Mason Cooley

Market packs its schoolbags as economic vacation comes to an end

It is likely that for each of us, our childhood memories of summertime was a time of bliss. The structure and discipline of the school year is thrown aside for two glorious months as problem sets shift from studying for math or spelling exams, to who is hosting the next sleepover or pool party. It’s a time to reset and be care-free, even if only for a time. The notion that this environment is short and seasonal, while acknowledged, couldn’t be further from thought. But, like all good things, it comes to an end as children face the reality that a return to structure, lessons, actions and consequences is inevitable. As they organize their binders for their new class list, they’re filled with apprehension to see the same subjects they’d struggled with so much last year. The dreaded subjects never really went away, they were just ignored, and it is now time to pick up right where they left off.

It is likely that for each of us, our childhood memories of summertime was a time of bliss. The structure and discipline of the school year is thrown aside for two glorious months as problem sets shift from studying for math or spelling exams, to who is hosting the next sleepover or pool party. It’s a time to reset and be care-free, even if only for a time. The notion that this environment is short and seasonal, while acknowledged, couldn’t be further from thought. But, like all good things, it comes to an end as children face the reality that a return to structure, lessons, actions and consequences is inevitable. As they organize their binders for their new class list, they’re filled with apprehension to see the same subjects they’d struggled with so much last year. The dreaded subjects never really went away, they were just ignored, and it is now time to pick up right where they left off.

After a long, pandemic-era period of low rates, near zero inflation and easy access to credit, the subjects we’re picking right back up on include:

- Rising and persistent inflation, just as it had tripled in Canada from June 2017 through July 2018

- An interest rate hiking cycle last attempted from 2017-2018

- A return to the U.S. – China tensions that dominated headlines in 2019

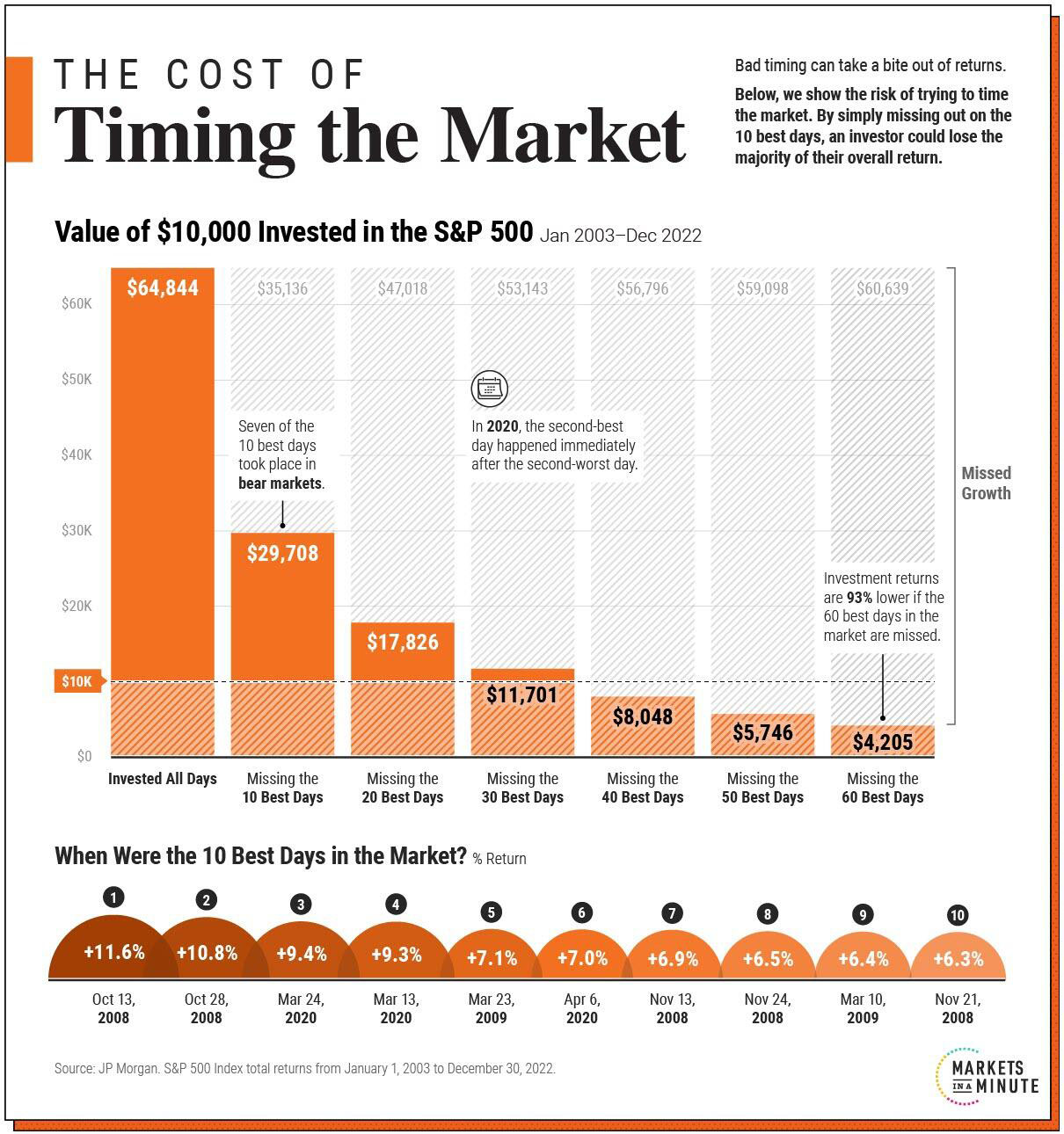

It’s crucial, now as always, to remember that the market is a cranky toddler that the economy is trying to ‘parent’ – they are not one and the same. Just like a toddler, the ‘market’ has a short-term memory, often displays erratic behavior and mood swings, and engages in gross exaggeration and fixation. Reason and logic are often not always the best approach when dealing with a toddler (and the market) and it’s best not to try and predict short-term behavior. The parenting economy can attempt to provide the right environment and warning signals when market behavior is likely to lead to adverse consequences, but at the end of the day, this toddler may not listen and may take their sweet time coming around. So, while the economy flashed signs of recession, the market continued whimsically through it’s economic summer with the S&P500 (USD) posting 17.4% gains and Canada posting 4.7% gains year-to-date (YTD) through to August 31st. Not necessarily a recession avoided, but certainly one postponed.

An important distinction to make is that when we talk about ‘risk of recession’, that’s an economic term understood to describe two back-to-back quarters of weakening real gross domestic product (inflation adjusted GDP). On the other hand, a ‘bear market’ describes a stock market decline greater than 20%. There is a link between recession and bear markets, but one does not always lead to the other; the economy is not the stock market. Worse yet, economic guidance that should influence market behavior is slow to arrive and slow to have an impact. Even the Bank of Canada states that it takes 18-24 months for a rate policy change to impact price levels. Measured from the start of their policy hiking cycle in 2022, that timeline takes us to right about now, so we’re only beginning to see the economic impacts of the first instances of those hiking decisions. Inflation, like unemployment, is what we call a lagging indicator – the last shoe to drop. Unemployment is the natural response to a slowing economy and lack of demand, and as such, many indicators flash red before any employment impact is felt. Separating indicators into “Leading”, “Coincident”, and “Lagging”, we believe our economic scorecard for North America looks like this:

Clearly, the only positive economic indicators are those that are trapped in the past, and all of our leading and current data points are either negative or deteriorating. It may seem at first glance that the market is gleefully ignoring daunting economic reality, but when you pop the hood on U.S. market performance this year, there’s a different story. To June 29th, 2023, the S&P500 was up over 14.0%. When you exclude the top 10 AI stocks in that market, year-to-date gains were only 1.2%. That’s a gap that doesn’t indicate widespread optimism on market or economic growth, just a strong belief in one sector of technology. Without it, U.S. market growth has been stagnant.

In Canada, pessimism continues to prevail as both Bank of Montreal (BMO) and Bank of Nova Scotia (BNS) missed profit expectations this week, both citing provisions for credit losses. This is not a new theme as the big Canadian banks have been aggressively setting aside money to cover bad loans, and reasonably so. A Q2 2023 report from credit monitor Equifax Canada showed that, versus last year:

- Missed debt payments (non-mortgage) are up by 175,000 (18.8%).

- Insolvencies are up 28.5%. Consumer proposals are up 36.5%.

- New mortgage originations are down 42%.

- Non-mortgage debt delinquency has increased 25.3%. In BC and Ontario, that’s over 31%.

That’s the bad news.

The good news is that recessions come in many different forms and causes, and an inflationary recession is one where policy tools exist to set the economy back on track: the rates. High interest rates, while unpleasant in the short term, act as “dry-powder” to be able to cut and stimulate the economy in the event of a recession, particularly one driven by inflation. In fact, the largest contributor to May’s 3.4% inflation rate in Canada was increased mortgage interest cost, a direct result of high rates themselves. When artificially high rates are the largest driver of the inflation problem you’re trying to correct, cutting provides both relief to an already-defaulting consumer as well as a disinflationary pressure. At present, Canadian money markets have priced in a probability of 77% that rates will have dropped -1.25% by this time in 2025. Absent of any further economic disruption and while inflation remains the primary concern, it is our team’s view that the market impact of a Canadian recession would be immediately met with substantial rate cuts, limiting the drawdown. We also believe that weakening U.S. economic data would further allow for greater cuts in Canada without currency disruption. With rate targets in Canada now at 5% and the U.S. bound between 5.25%-5.5%, we haven’t had this much dry powder in 15 years.

As we approach our September Gold Seal Financial Group quarterly asset mix meeting, we’ll be carefully evaluating our shorter term, tactical positioning to reflect some of the more near-term risks in North America and abroad. While some positioning changes are likely to appear defensive in nature, we are always careful to moderate our convictions and maintain flexibility in our client portfolios for evolving conditions. After all, this toddler market may take its time coming around.

Big trouble in little China

As detailed above, one of the main returning themes this year was a revival of the U.S.–China economic relationship woes that plagued 2019. While our own convictions on the Chinese equity market are another article entirely, the decision since inception of our Serenity investment strategies has been to significantly underweight investment in Chinese equities, insulating the portfolio from Chinese equity risk. Our emerging markets strategy within our Serenity portfolios has been implemented with an Exchange Traded Fund (ETF) that runs a screen prohibiting investment within Chinese equity markets, resulting in a significant under-exposure to the country. Where China accounts for 18.5% of the global economy, it is 1.4% of our stock exposure.

As such, our investors were relieved not to have felt the ripples sent through global markets this month as brewing disruption in the Chinese real estate sector threatens to boil over into a full real estate crisis. The second largest real estate development firm in the country, China Evergrande Group, filed for bankruptcy in the U.S. on August 17th, two years after defaulting on it’s debt. A second firm, Country Garden Holdings, failed to make payments on its bonds this month after issuing an earnings warning on August 10th anticipating losses greater than $6 billion USD. Other real estate firms showing signs of distress include Sino-Ocean, which failed to meet repayment of a $2 billion yuan bond, and KWG Group Holdings, that defaulted on their bond payments after having already received an extension. The Chinese real estate sector as a whole is suffering another terrible year, with property investment growth -12.2% over the year and new home sales growth down -15.4%.

The fear is that this sector proves symptomatic of an overall weakening economy, as a population dealing with the repercussions of 30 years of a one child policy begins to feel the impact of reduced demand and limited labor force. While the backdrop of deflation and decreasing economic indicators is one concern, access to and accuracy of that data is another. Particularly during times of volatility, we as investors require full and timely access to information. Alarmingly, our access to Chinese economic data is getting worse as it deteriorates with the country suspending reporting on youth unemployment data – right after posting a record high of 21.3% in June. While the People’s Bank of China has already begun cutting key rates in response to weakening conditions, we will be maintaining our underweight to Chinese equity until quality and availability of information improves.

August Market Insights: Unveiling the crystal ball

A glimpse into the future of financial markets from 2024 to 2030.

How will the events of this decade shape the markets of tomorrow? In his August Market Insights, Dr. James Thorne, Chief Market Strategist at Wellington-Altus reviews past and present economic trends to reinforce his position about the future of financial markets and what they hold for investors.

Click here to read the full article.

Gold Seal Insights

Tanya’s Tips:

Now that summer is winding down, and we head into a new school year, it’s also a great time to consider ways to augment savings for a beneficiary’s post-secondary education.

A RESP is a Canadian registered investment account that promotes saving to support a beneficiary’s post-secondary education. When the time comes to withdraw funds for post-secondary education purposes, many subscribers wonder about the best approach to maximize the RESP’s value and minimize taxes.

Important considerations to make the most of the RESP Account include the withdrawal strategy. Generally, it makes sense to withdraw Educational Assistance Payments (EAPs) first. You should also plan to withdraw contributions as Post-Secondary Education Payments (PSEs) and there are also opportunities to transfer unused funds to another beneficiary or a RRSP.

To learn more about RESP fundamentals such as how to maximize the account value and minimize taxes, please read the full article.

Cycling across the country, one province at a time…

Well, it’s time! Time for Brendan to venture back out to see more of this beautiful country on his road bike. This time, our fearless partner, Ryan Archambault is joining him as they courageously set off to the Alberta/Saskatchewan border this weekend to continue the trek from the west coast to east coast of Canada. Having already cycled across BC and Alberta in past years, this year, Brendan (and Ryan) are tackling Saskatchewan.

Every year, our team’s cyclists choose a cause to raise money for while on the ride. This year, the cause was an obvious one. The West Kelowna fire was devastating. Authorities issued evacuation orders to safeguard residents and properties. Firefighters from all over the country, supported by aerial resources, battled the flames tirelessly. The view of the fire ravaging the Kelowna mountainside is something few will soon forget. Despite their efforts, nearly 200 homes and structures have been severely damaged or destroyed, and the blaze continues to consume significant forested areas. The community’s resilience and collaborative firefighting efforts were crucial in mitigating the disaster’s impact. Now, resources are critical for those displaced or homeless.

Brendan and Ryan are riding for the relief efforts offered by Mamas for Mamas. If you wish to show your support for both their efforts as well as Brendan and Ryan as they cycle over 700kms across Saskatchewan next week, please follow THIS LINK.

The Gold Seal Financial Group wishes Brendan and Ryan good health and the wind at their backs as they cycle across Saskatchewan!

Ryan’s Rationale:

No pension? No problem, make your own.

Incorporated business owners all too often contribute to their RRSP’s without considering that there’s an alternative vehicle available: the Individual Pension Plan (IPP).

An IPP is like an upgraded RRSP – offering asset diversification, increased retirement savings, tax deferral, and even creditor protection. You earn contribution room if you draw employment income from the corporation, so you’re still gaining Canada Pension Plan eligibility, and the funds will grow tax-deferred.

You can also still hold and invest in the same securities you otherwise would within an RRSP. However, IPPs are quite different in that the retirement benefit of an IPP is pre-defined, and it’s up to the corporation to ensure there’s enough contributions and growth to fund it. Every IPP must abide by the restrictions and assumptions in the tax legislation and possibly the provincial pension rules as well. So, due diligence is key, and that’s where our team can step in to help!

Business owners, these are the conversations that should happen BEFORE you start down the path of saving. Let’s plan better for a secure retirement.

Noteworthy Links

- Tips to Protect Your Smartphone from Getting Hacked

- ‘I watched my home burn’: on the front line with firefighters during B.C.’s worse fire week

- Ebert.com’s review of “Oppenheimer”

- Exploring the ancient wonders of Jordan, travellers learn just how small they are in time

- Grey divorce and retirement planning: What you need to know – Starts at 60

- 3 Financial Traits – and 6 ‘Non-Financial’ Traits of Happy Retirees

Photo of the Month