Overview

- Team Update

- Portfolio and Market Performance

- Market Commentary

- Portfolio Update

- Global Outlook

Team Update

Next month (August), there will be no call or update – we usually skip a month every summer as most people are on vacation or travelling. We will be back with our monthly update the first week of September. By then, we should have moved into our newly renovated office and are looking forward to welcoming everyone. We may even throw a small party to celebrate!

Portfolio and Market Performance

Year-to-date performance as of June 30, 2023

- TSX 60 Total Return, C$: 5.7%

- S&P 500 Total Return, US$: 16.9%

- NASDAQ Composite Total Return, US$: 32.3%

- Dow Jones Industrial Average Total Return, US$: 4.9%

A quick note on currency: the U.S. dollar is down 2.7% year to date, creating a drag on U.S. dollar-denominated positions.

The Conservative Equity Portfolio returned 21.2% year to date and has averaged 10.4% per year over three years, 10.2% over five years, and 12.3% since inception (October 2015).

The Diversified Income Portfolio, which is our balanced portfolio used for many of our clients’ registered accounts, returned 6.6% year to date and has averaged 9.8% per year over three years, 8.9% over five years, and 9.0% since inception (July 2017).

The Focused Total Return Portfolio returned 33.4% year to date, averaging 14.6% per year over three years and 19.4% since inception (April 2020).

Your returns will vary depending on the amount of fixed income you hold, cash flows in and out, and management fees.

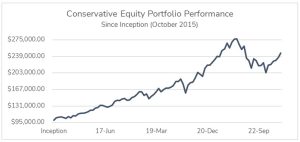

Sometimes, our clients ask when their portfolio will return to its all-time high. This is a common question, especially shortly after a bear market. For some context, we’ve included this graph that illustrates the performance of our equity strategy over time. We believe the market went up too much in 2021 and probably down too much in 2022. The best strategy is to simply stay invested through the volatility and reap the long-term average returns.

When managing equities, our goal is to average at least 10% per year over five years. Sometimes this number will be lower, like it was last year when we saw our five-year average dip to 9%, and sometimes it will be higher, like in 2021 when our five-year average reached almost 20%. By staying focused on the quality of the businesses that we own and not the stock market’s short-term movements, we expect your portfolio to continue to grow at our target return of 10% per year, retaking the previous high and ultimately surpassing it. We stay invested, and over time that’s how wealth is built.

Market Commentary

The Consumer Price Index (CPI) for May, released in mid-June, showed that inflation in the United States was coming down faster than people had expected. The year-over-year number has now come down to just 4%, and the monthly change was an increase in average prices of 0.1%. Markets rallied on the news, and the U.S. Federal Reserve Board paused interest rate hikes for the month with the overnight rate sitting at 5%.

It was similar in Canada, with our annualized CPI reported at 3.4% year over year as of May. The Bank of Canada had raised overnight rates a quarter point at the beginning of the month before the data was released, bringing it to 4.75%, still below the U.S. rate.

Despite predictions of a looming recession, it has yet to materialize. GDP reported at the end of this June was positive in the first quarter, making for three consecutive positive-growth quarters in a row. When we went through the numbers by industry, it was clear the banking problems in the U.S., brought on by higher interest rates, had a negative effect, as the financial sector was the biggest detractor, while health care was the biggest contributor to growth. Government spending continues to be a huge contributor as well.

Between a strong jobs market and government spending, the economy is certainly more robust this year than many people had predicted.

On the currency front, last month, we saw the U.S. dollar weaken and the long list of things the media said we needed to worry about are now behind us. The U.S. government did not default on their debt, inflation isn’t out of control, and we aren’t headed into a deep recession. That $5 trillion, that had been sitting in U.S. treasuries, increasing demand for U.S. dollars, has started to move back to “risky” assets, and the flight to safety appears to have ended, resulting in a weaker USD.

At the same time, here in Canada, the CAD dollar has strengthened. Fears of a housing crash haven’t materialized, and the economy remains stable, despite the increase in interest rates.

Is this the recession that never happened? People in the media have been calling for a recession for almost two years. Eventually, they will be right – just not yet.

Portfolio Update

Six weeks ago, we added to our position in Amazon, believing that the stock would rally as investors look to purchase more mega-cap tech. Microsoft, Apple, and Nvidia had already run and were retesting all-time highs. Amazon has been in a bear market for the past two years and is finally coming out and starting to rally. This aligns with our strategy to trade around the companies we know well and have confidence in. Amazon has rallied 13% since adding to the position.

Tesla rallied 30% last month and was the portfolio’s largest contributor to performance.

We believe there are three reasons why Tesla stock rallied so much this year:

- Inflation is coming down and long-duration assets do well in this environment.

- AI boom – people are finally starting to wake up and recognize that Tesla is not just a car company.

- Legacy automakers and other charging stations are moving to Tesla’s charging standard.

Last month, Ford, GM, Rivian, Volvo, and Polestar announced they would start using Tesla’s charging standard. Blink Charging, ChargePoint, and Electrify America have also announced they would start using Tesla’s charging standard.

This could be the beginning of something big.

If Tesla is already licensing their charging technology to all the auto manufacturers, the next logical step would be to license its operating system, self-driving technology, and possibly battery manufacturing down the road. This would be a huge revenue driver, and we believe the revenue and margins would be substantially higher than their auto sales in the future. We will leave it at that for now. But we like Dan Ives’s quote from Wedbush Securities, using the analogy of the charging standard being a gateway drug to other bigger technologies in the future.

Tesla reported their third-quarter global vehicle delivery numbers – 466,000 vehicles in the second quarter. We will see their actual financial results related to this in their earnings report on July 19. The stock jumped roughly 7% on the news, as most wall street analysts were expecting 440,000 deliveries.

That said, focusing on the quarterly vehicle production is a limited short-term indicator, as we are more interested in what the entire company will look like in three to five years, not how many cars they sell this month. Nevertheless, it still indicates consistently strong execution on their part and demand on the consumer side. It also suggests that they are on track for their 50% annual long-term growth targets. Many analysts are reporting 83% vehicle production growth year over year for the quarter, but we think even that strong number is not an accurate picture since they had to close a Chinese factory in Q2 of last year amid COVID-19 restrictions.

RBC Capital Markets Equity Research Analyst Tom Narayan recently published a research report on Tesla that made some waves in the investment world. In the report, he looked at the different business lines and set Tesla as their top investment idea with a $305 price target.

As positive as Tom’s report was, we believe he was overly conservative. For example, he set zero profits on car production and put car sales at 2.1 million for 2024 and given that Tesla will likely get close to that number this year, we believe this estimate is too low. We also believe that the assumptions used to calculate the expected cash flow from autonomous driving vehicles and robotaxis were overly conservative.

Despite these conservative assumptions, Narayan estimates that approximately 80% of the long-term value of the company will come from the autonomous driving vehicles and software, only around 10% from the actual car production, and a small portion from the Tesla Energy storage business. Currently, car production represents almost all the value, as that is where the earnings and revenue are coming from. So, he’s saying that five years from now, the company will be deriving the majority of profits from areas other than car production. Whether he ends up being right or not, the point is that the company has significant growth potential from multiple lines of business. Tesla’s licensing of its car software to other car companies around the world, could make Tesla the Microsoft of car software. Think about what Apple did for the telephone.

Regardless, we are happy to see an analyst who is at least doing the work to explore the numbers.

Global Outlook

Looking to Russia, the Wagner Group private military uprising had no effect on financial markets, as it began Friday and was halted before the end of the weekend.

A resolution of the conflict in Ukraine would have a positive effect on financial markets as it would further reduce food and energy inflation. However, political instability in Russia could have longer-term negative repercussions. We’re not so sure had the rebellion continued that it would have been a net positive for markets.

Over in China, the economy has been less robust than they had hoped, and so we are seeing a lot more dialogue coming from China recently. China is still growing at around 4% this year but certainly less than the 6% growth they are used to.

Overall, the global situation is fairly good and certainly better than most had expected. This contributed to surprisingly strong equity markets over the first half of the year. Historically when markets rally more than 10% in the first six months of the year, the second half also tends to be strong.

~~~

We would like to thank all clients for their continued trust and support.

We’ll see you back in September. Have a great summer.

Simon & Michael

Simon Hale, CIM®, CSWP, FCSI®

Senior Wealth Advisor,

Portfolio Manager

Wellington-Altus Private Wealth

Michael Hale, CIM®

Senior Wealth Advisor,

Portfolio Manager

Wellington-Altus Private Wealth

Hale Investment Group

1250 René-Lévesque Blvd. West, Suite 4200

Montreal, QC H3B 4W8

Tel: 514 819-0045