Dear Friends & Clients,

Spring has finally started to show up here in Canada. It’s that in-between season—too cold for the lake, too warm for the slopes—but perfect for getting outside, firing up the barbecue, and catching your breath after a busy winter.

It’s also a good time to step back, take stock, and look at where things stand.

2025 Taxes

After a busy month of April, tax season is wrapping up. Many of you noticed a higher tax bill this year, which is a side effect of a very good “problem” to have: our conservative equity portfolios compounded at over 24% per year over the last three years. To maintain our strict risk controls, we had to trim several major winners like Nvidia, Tesla, and AMD once they grew beyond a 10% portfolio weighting. This triggered an average of around 10% in capital gain across our clients’ taxable portfolios. Fortunately, Canada’s capital gains tax rates (around 20% to 25% depending on your bracket) remain quite favorable compared to our high income tax rates.

We will continue to manage things in as tax-efficient a manner as possible as we always have. At the same time, we must be vigilant in managing risk, protecting capital, and ensuring our capital is as well deployed as possible, even if it means triggering capital gains from time to time.

Performance Update

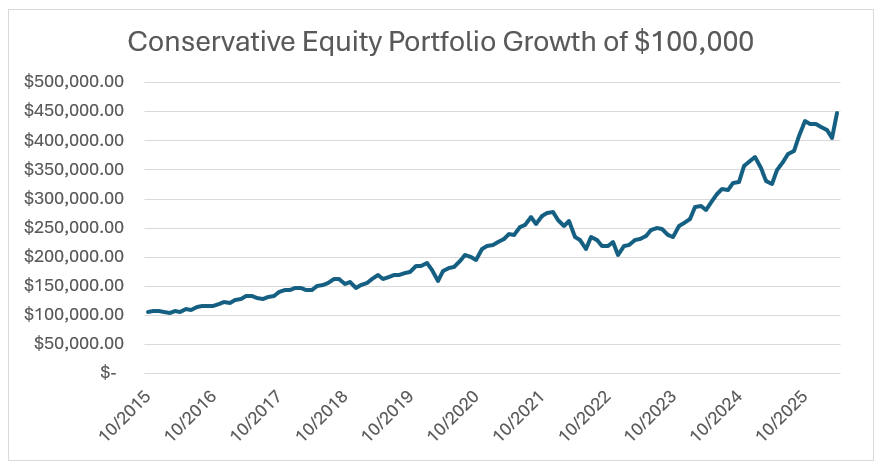

April delivered one of the best single-month returns we’ve seen in the last 20 years, rivaling the January 2009 rebound and the April 2020 pandemic recovery. Our Conservative Equity portfolio was up over 10% for the month, and the Focus Total Return portfolio was up nearly 14%. When we look at the long-term compounding of these strategies, the numbers speak for themselves:

|

Investment Performance (%) |

|

|

|

|

|

|

As of April 31, 2026 |

YTD |

1Y |

3Y |

5Y |

SI |

|

CONSERVATIVE EQUITY TOTAL GROSS RETURN (CAD) |

4.7% |

37.8% |

24.8% |

13.4% |

15.6% |

|

Benchmark (50% DJ US Div 100; 45% S&P/TSX 60, 5% S&P Can T-Bill) |

12.3% |

30.9% |

16.4% |

11.6% |

12.3% |

|

Morningstar Category (Global Neutral Equity) |

-2.1% |

12.0% |

13.2% |

8.1% |

9.4% |

|

|

|

|

|

|

|

|

DIVERSIFIED INCOME TOTAL GROSS RETURN (CAD) |

0.8% |

18.6% |

13.0% |

9.3% |

10.7% |

|

Benchmark (35% S&P Can Bond; 25% S&P Can Div; 25% DJ US Div 100; 10% MSCI EAFE, 5% S&P Can T-Bill) |

7.7% |

19.7% |

11.5% |

8.0% |

N/A |

|

Morningstar Category (Global Neutral Balanced) |

0.0% |

8.9% |

9.6% |

5.8% |

N/A |

|

|

|

|

|

|

|

|

FOCUSED TOTAL RETURN TOTAL GROSS RETURN (CAD) |

10.1% |

54.4% |

31.0% |

18.1% |

23.4% |

|

Benchmark (40% DJ US Div 100; 35% S&P/TSX 60, 20% S&P Can Bond, 5% S&P Can T-Bill) |

9.9% |

24.7% |

13.6% |

9.3% |

N/A |

|

Morningstar Category (Tactical Balanced) |

1.2% |

10.3% |

8.8% |

5.3% |

N/A |

|

|

|

|

|

|

|

|

S&P 500 (NR USD) – USA |

5.6% |

30.6% |

21.2% |

12.7% |

|

|

S&P TSX 60 (NR CAD) – CANADA |

7.3% |

35.3% |

19.5% |

14.3% |

|

|

MSCI EAFE (GR CAD) – EUROPE |

5.6% |

23.4% |

16.0% |

11.6% |

|

*Your own returns will vary depending on the amount of fixed income you hold, cash flows in and out, and management fees.

|

LARGEST MUTUAL FUND IN CANADA (1.94% MER FEE) |

YTD |

1Y |

3 yr |

5 yr |

10 yr |

|

RBC SELECT BALANCED PORTFOLIO FUND (A) NET RETURN (CAD) |

4.2% |

17.9% |

11.7% |

6.5% |

7.1% |

Portfolio Moves & The Beauty of Simplicity

We like to buy wonderful businesses and let them do the heavy lifting, but occasionally the market gives us a fat pitch. Late last month, we trimmed a flat-trading Berkshire Hathaway position to buy more Micron on a pullback around US $360. Today, Micron is trading over $800. When we added to Micron, it was trading at an incredibly cheap four times future earnings. Strategic moves like this aim to add 1% or 2% alpha to our returns over time.

In other portfolio news, Brookfield is exploring merging its dual trust and corporate unit structures into a single corporate structure. These exist for both Brookfield Renewable Partners and Brookfield Infrastructure Partners. While trust structures previously allowed for higher distribution rates by avoiding corporate taxes, they also generated frustrating tax slips for those in taxable accounts. On the investment side there are also many large international investors that are not able to own trust units, excluding the trust units from many potential investors. If it proceeds, we see this simplification of structure as largely positive, paving the way for greater inclusion in market indexes and access to a larger pool of potential investors, which would push the share price higher.

As a side note, Cameco’s recent earnings call highlighted massive global interest in the AP1000 micro-reactors. This is fantastic news for Brookfield Renewable, which owns 51% of Westinghouse, the creator of those reactors. The combination of a tremendous business in a growing sector, along with a simplified share structure, reinforce our view of the potential in Brookfield’s businesses.

The Main Event: Earnings & The AI Infrastructure Race

We are witnessing a massive shift in technology, but the limiting factors for artificial intelligence (AI) aren’t just software—they are physical chips and electrical power. Companies like Anthropic have incredible demand for their AI models but are bottlenecked by a lack of compute power, forcing them to limit access. Because hyperscalers own the servers, they hold all the leverage. We’ve positioned your portfolios to benefit from these “tollbooth” businesses.

Here are the highlights from a stellar earnings season:

Global Macro & The View from the Porch

Despite global tensions, such as those in the Strait of Hormuz causing oil and bond yields to fluctuate, markets remain incredibly resilient. We started last month at “peak fear” and ended with immense optimism due to businesses executing so well.

Lending rates remain somewhat elevated, putting pressure on the housing market. However, as inflation cools and rates eventually recede, paired with expanding corporate profits, we see a highly constructive environment for equities. On the geopolitical front, we are carefully watching the upcoming meeting between Chinese President Xi Jinping and U.S. President Donald Trump, the USMCA review in July, and the U.S. midterms this November.

Closer to home, the federal government’s proposed “Canada Strong Fund” (a sovereign wealth fund) has sparked a lot of debate. While we remain cautious given the government’s track record of red tape and economic stagnation over the last decade, there is a potential silver lining. If structured properly, co-investing public funds alongside private capital (like BlackRock or Blackstone) could incentivize progress, fast-track infrastructure approvals, and allow the public to share in the economic upside. Only time will tell.

Closing Thoughts

Looking ahead, we are maintaining our target of 8,000 for the S&P 500 by year-end. Businesses are executing exceptionally well, profit margins are expanding, and the economic engines are humming.

Spring is here, the markets are green, and it’s time to enjoy the warmer weather. My brother and I are deeply grateful for your continued trust and partnership with the Hale Investment Group. If you ever have any questions about your portfolio, our lines are always open.

Fire up the barbecue, and we will talk to you next month.

Warmly,

Michael & Simon Hale