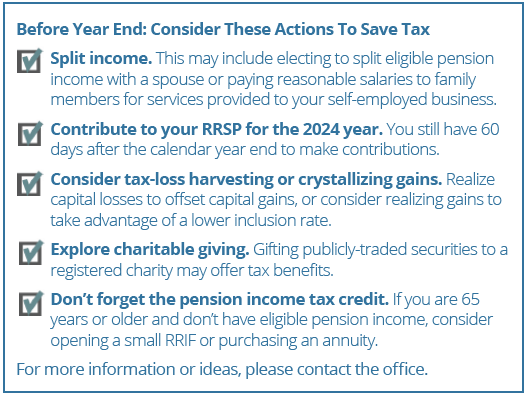

Year-End Planning & An Increased Inclusion Rate

With the (proposed*) increase to the capital gains inclusion rate in 2024, there have been various questions from investors about tax planning. Here are two that relate to year-end planning.

1. What is the Capital Gains Reserve?

When you dispose of capital property, you may realize a capital gain or loss: the difference between the proceeds of disposition and adjusted cost base of the property. The capital gains reserve allows you to reduce the amount of capital gain you report as income in a particular year by spreading it over multiple years. This may allow you to take advantage of a lower inclusion rate for gains realized up to the $250,000 threshold each year.

Usually, when you sell capital property, you receive full payment at that time. By claiming the reserve, you are able to report the portion of the capital gain in the year you receive proceeds of the disposition. Generally, the maximum period over which most reserves can be claimed is 4 years, spreading out a gain over 5 years (or 10 years for family farm/fishing property transferred to a child). Generally ,taxpayers must claim at least 20 percent of the gain annually each period (or 10 percent for farm/fishing property).

Why use the capital gains reserve? If you are looking to transfer a cottage or cabin within the family, this may be one way to help spread out the capital gains tax to take advantage of a lower inclusion rate.

Already claiming a reserve? For business owners who have structured a sale and claimed a reserve prior to June 25, 2024, and are subject to an increased inclusion rate, you may consider bringing a portion of the transaction out of reserve (where possible) in 2024. This is because the CRA has stated that “the amount of a capital gain that is brought out of reserve would be deemed to be a capital gain of the taxpayer form a disposition of property on the first day of the taxpayer’s taxation year for the purpose of determining the inclusion rate.” For individuals, this is January 1, so the transaction would be subject to the 1/2 inclusion rate and not 2/3.

Be aware that transactions that claim the capital gains reserve will need to be carefully structured, so seek advice from a tax specialist.

2. Does the Increased Inclusion Rate Affect Tax-Loss Selling?

Some investors have asked how the loss carryback/forward rules apply given the increased inclusion rate this past June. What happens when a loss on an investment was realized when the inclusion rate was1 /2, but the capital gain to which you want to apply the loss to is realized at the new 2/3 inclusion rate?

Net capital losses realized in previous tax years are deductible against current-year taxable capital gains by adjusting their value to reflect the inclusion rate of the capital gains being offset. As such, a capital loss that was realized when the 1/2 inclusion rate prevailed can still fully offset an equivalent capital gain realized in a year during which the 2/3 inclusion rate prevails.

As a reminder, generally an investment held in a non-registered account that is sold for less than its original cost will result in a capital loss. For tax purposes, the capital loss can be used to offset any capital gains realized during the year to reduce your current tax liability. If you don’t have sufficient capital gains to offset the losses, the net capital loss can be carried back to any of the previous three taxation years to offset realized capital gains, or carried forward to use against future realized capital gains.

Be aware of the “superficial loss” rules, which deny the capita loss if you or an affiliated entity (such as a spouse) acquires the same security either 30 days before/after the date of the loss transaction. In this case, you will not be allowed to use the capital loss in the current tax year to offset capital gains. Instead, the capital loss will be added to the adjusted cost base of the identical property.

*At the time of writing, the implementation bill has not achieved royal assent

The information contained herein has been provided for information purposes only. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information has been provided by J. Hirasawa & Associates and is drawn from sources believed to be reliable. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document. Wellington-Altus Private Wealth Inc. (WAPW) and the authors do not guarantee the accuracy or completeness of the information contained herein, nor does WAPW, nor the authors, assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact me for individual financial advice based on your personal circumstances.

Insurance products are provided through Wellington-Altus Insurance Inc.

© 2024, Wellington-Altus Private Wealth Inc. ALL RIGHTS RESERVED. NO USE OR REPRODUCTION WITHOUT PERMISSION.

www.wellington-altus.ca

If you no longer wish to receive commercial electronic messages from Wellington-Altus Private Wealth Inc., please send an email to unsubscribe@wellington-altus.ca