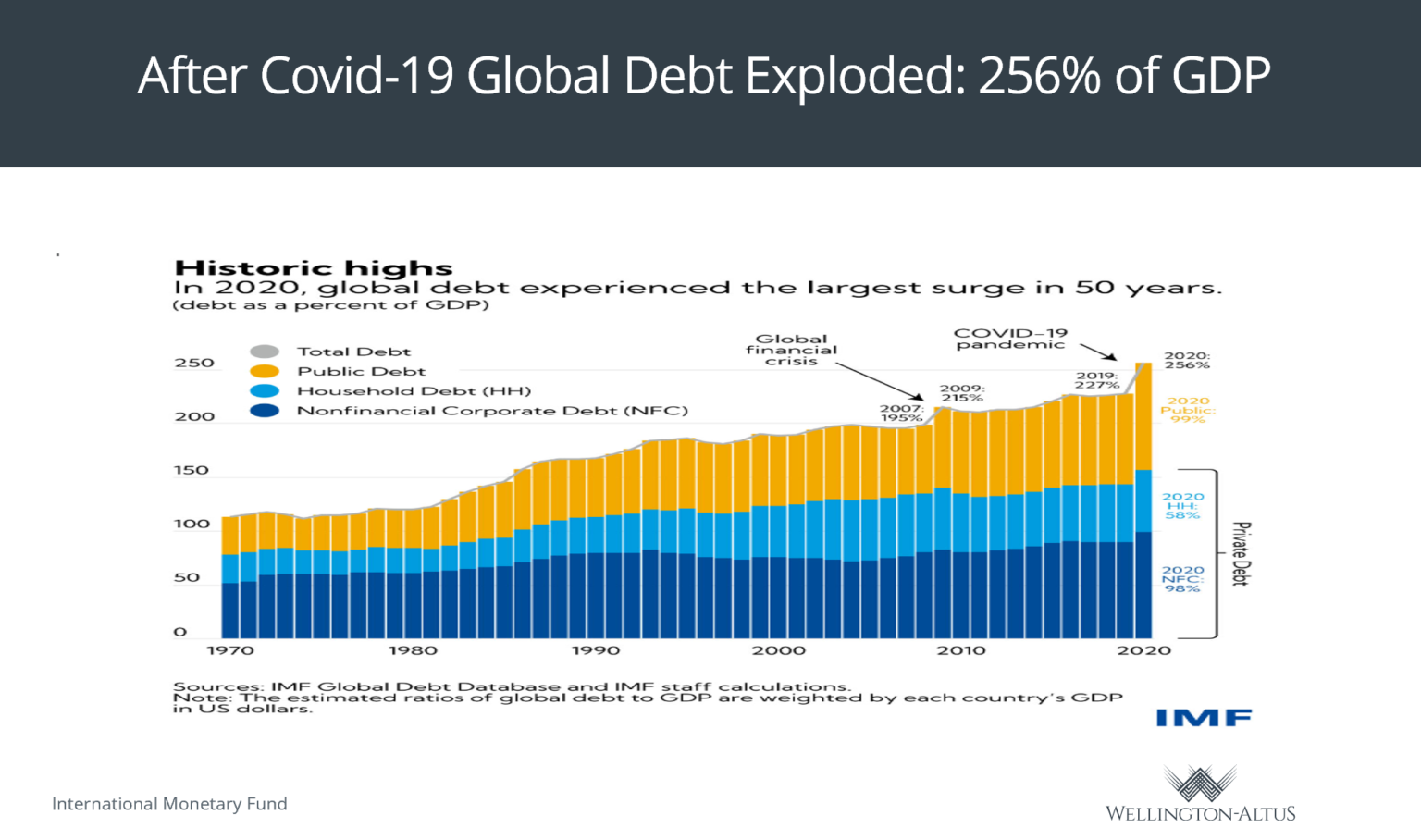

The longer-term inflationary risk today results from fiscal policy rather than wages. These fiscal inflationary pressures are caused by the desire of some to implement policies, for example, to reduce income inequality or greenhouse gases, irrespective of their effects on inflation. Can these policies be implemented in a non-inflationary way? As Nobel Prizewinning economist, Thomas Sargent theorized, “permanent high inflation is everywhere and always a fiscal phenomena.⁵” With the IMF reporting that global debt has reached 256%, one wonders how long the global economy can withstand high-interest rates.

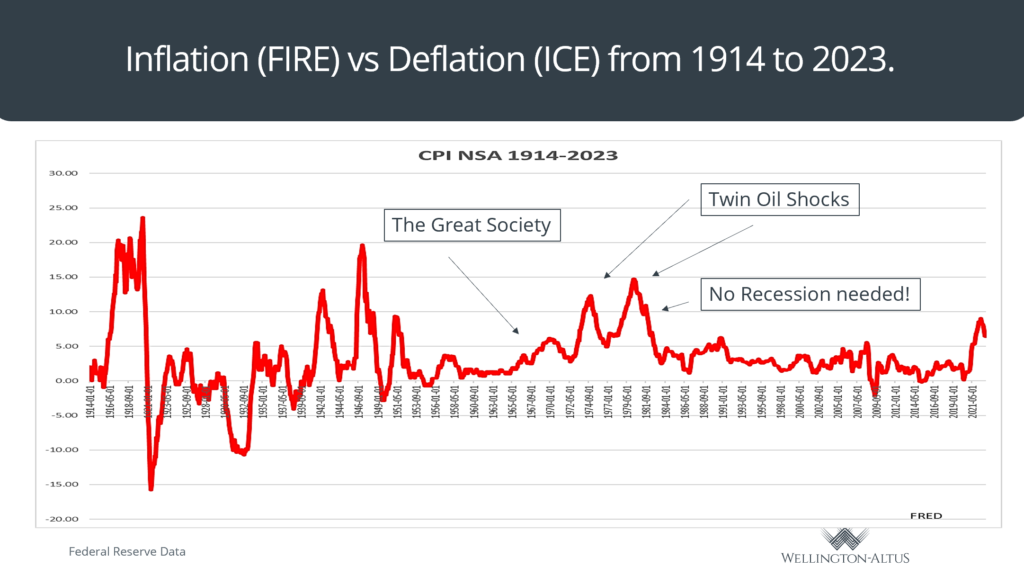

In the late 1960s, bowing to political pressure, President Johnson’s Great Society policy introduced dramatic social reform, disregarding its long-term inflationary effects. Monetary policy cannot counteract the extreme forces of fiscal policy, which is why we may have been too harsh on central bankers that came before Paul Volcker. Could Paul Volcker have been able to counteract the long-term inflationary pressures caused by NASA’s quest to reach the moon, the Vietnam War, and the Great Society? I say no. Mr. Volcker is not the prophet many make him out to be. An excellent central banker, yes, but with the good fortune of being at the right place at the right time.

Today, many try to frame the debate with the context that the Fed wants to avoid making the same mistakes they did in the late 1960s and early 1970s. If that’s the case, we need an honest and transparent recognition that fiscal policy threatens long-term inflation more than wage increases and a tight labour market. If not, monetary policy could be rendered impotent. Risks of unfunded entitlements, net zero, healthcare, and income inequality need a pragmatic solution that balances adoption and mitigation. At the same time, the ability to minimize structural inflationary effects on the economy. For example, the implementation of a policy that detrimentally affects the fertilizer industry will cause food prices to rise. Likewise, raising the minimum wage may cause prices in restaurants to increase.

The Fed’s response to COVID-19 was to use sector 13-3 of the Federal Reserve Act to create $4.5 trillion for the Treasury to inject through social programs to support the economy through the pandemic. This injection was as large as the fiscal policy response to WWII but implemented in half the time: the result was inflation. With extreme debt levels, it will be only a matter of time before the credit markets push back. Yes, the return of the bond vigilantes should not surprise. But if fiscal responsibility does not return, investors need to prepare for an era of higher interest rates and a financial crisis with the debt bubble finally popping, ushering in a new deflationary era.

In this instant gratification, group-think world, we need to remember that the thesis Chair Powell and Tiff Macklem anchored from in early 2022 was that the private sector, historically low unemployment, and job openings would lead to wage growth. Mr. Powell and Mr. Macklem are softening their stance on inflation while simultaneously recognizing the risk to the downside if the policy overtightens and ignites a debt deflationary downward spiral. The fight over inflation is not over, but if policymakers look ahead 18 to 24 months, they can easily paint a plausible narrative where deflation and secular stagnation episodes take hold.

What Should Investors Do?

Investors should expect the heated debate between inflation and deflation (fire and ice) to take center stage as the year progresses. Our base case is that inflation will continue to decline. In this environment, stocks and bonds should continue to appreciate, with annualized non-seasonally adjusted CPI from July 2022 tracking at 1.71% in the U.S. and 1.026% in Canada. Inflation is slowing in a structurally tight job market. An occurrence many proclaimed could never happen. A recession may not be needed to tackle inflation, just as in the 1970’s. With deflationary forces sitting in the wings, the more that central bankers continue to raise rates, the higher the probability of a significant deflationary event.

With the Republican control of Congress, and a budget ceiling debate on hand, there is a strong possibility that fiscal policy will become less inflationary. There are early indications that central bankers get it and thus recognize the risk to overtightening. As the year progresses, we expect the data to become more substantive in supporting the belief in deflation, secular stagnation, and a decline in interest rates. True, we live in an instant gratification group-think world, where narratives change as quickly as the positioning of day traders. With that, the debate between fire and ice will take center stage. Significant deflationary pressures built up in the pipeline, such as housing, should provide enough solid data for the central banks to pause and evaluate. Price stability is slowly, before our eyes, evolving into a two-way street, where the tension between the forces of inflation and deflation counterbalance. An environment where fire and ice cancel each other out sets the stage to a continuation of our secular bull market into the end of the decade.