Is the Small-Cap Surge Here to Stay?

Since October 2025, U.S. small-cap stocks have staged a notable comeback, outperforming large-cap growth stocks as investors look beyond years of dominance by tech mega-caps. This has prompted the question: Is this a temporary bounce, or the start of a more meaningful trend?

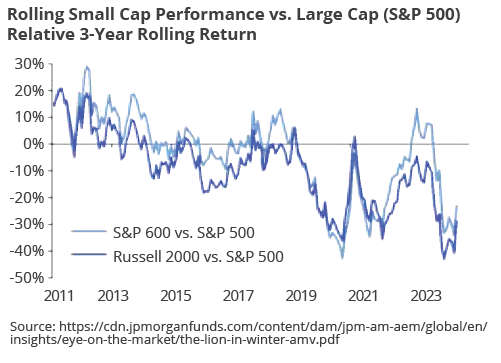

Small Caps vs. Large Caps

In the U.S., small-cap stocks are generally defined as companies with a market capitalization (share price multiplied by shares outstanding) between $250 million and $2 billion. The Russell 2000 and S&P 600 are the most commonly used U.S. small-cap benchmarks. In Canada, where markets are smaller, small caps are generally considered to have a market capitalization of $1.5 billion or less. In contrast, a large-cap stock generally refers to a company with a market capitalization exceeding $10 billion.

In the past, small caps were seen as attractive opportunities for those investors willing to take on more risk in exchange for potentially higher returns. These firms were perceived to have higher growth potential, as well as strong merger and acquisition prospects.

Yet, since 2010, small caps have largely underperformed large cap stocks (see graph for relative performance) and have traded at some of their lowest levels in decades. The current cycle happened for a reason. Large caps have had stronger earnings and better free cash flow margins, while small caps exhibit much lower profitability. Small caps often carry higher debt positions (relative to earnings) and are more exposed to interest rate changes due to floating rate debt and shorter average maturities. Rising interest rates between 2022 and 2024 placed significant pressure on many small caps with rate-sensitive debt. In addition, small caps tend to be more sensitive to economic cycles than their large-cap counterparts.

At the same time, many higher-quality small-cap companies are not listing publicly, instead being taken private by private equity firms before reaching scale. Private markets have grown dramatically: In 2000, private equity and venture capital firms managed around $600 billion in assets; today, assets under management exceed $10 trillion. This shift has resulted in a greater proportion of lower-quality companies entering small-cap indices, which has challenged overall returns.

Why the Rotation Into Small Caps Over Recent Months?

As valuations for tech mega-cap growth stocks remained well above historical averages, investors turned to more undervalued sectors. Recent easing of cyclical headwinds, particularly higher interest rates that previously pressured small-cap valuations, has created a more favourable environment for these companies. A weaker U.S. dollar has further benefited small-cap firms with foreign revenue exposure, while improvements in the U.S. regional banking sector have helped support broader small-cap business activity. Ongoing fiscal stimulus measures provide an additional layer of support, enhancing the potential for selective opportunities within the sector.

A Selective Approach

The small-cap universe is highly diverse, with significant variation in company quality and performance. As with many aspects of successful investing, a selective approach can help investors manage structural risks while identifying businesses with stronger balance sheets, earnings resilience and longer-term potential. Even with a more favourable environment emerging for the sector, ongoing economic uncertainty makes disciplined, quality-focused stock selection increasingly important.

The information contained herein has been provided for information purposes only. The information has been drawn from sources believed to be reliable. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document. Wellington-Altus Private Wealth Inc. (WAPW) does not guarantee the accuracy or completeness of the information contained herein, nor does WAPW assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact your financial advisor. Transactions of the type described herein may involve a high degree of risk, and the value of such instruments may be highly volatile. Such risks may include without limitation risk of adverse or unanticipated market developments, risk of issuer default and risk of illiquidity. In certain transactions prospective investors may lose their entire investment or incur an unlimited loss. This brief statement does not disclose all the risks and other significant aspects in connection with transactions of the type described herein, and prospective investors should ensure that they fully understand the terms of the transaction, including the relevant risk factors and any legal, tax, regulatory and accounting considerations applicable to them, prior to transacting. The information contained herein may include the opinions of representatives of third-party companies or organizations and may not necessarily reflect that of Wellington-Altus (WA) or its representatives. All third-party products and services referred to or advertised are sold by the company or organization named. While WA may have referral arrangements with some third-party companies or organizations, WA does not specifically endorse any of these products or services and is not liable for any claims, losses or damages however arising out of any purchase or use of third-party products or services. All insurance products and services are offered by life licensed advisors of Wellington-Altus Insurance Inc. or other insurance companies separate from WAPW.

© 2026, Wellington-Altus Private Wealth Inc. ALL RIGHTS RESERVED. NO USE OR REPRODUCTION WITHOUT PERMISSION. www.wellington-altus.ca

If you no longer wish to receive commercial electronic messages from Wellington-Altus Private Wealth Inc., please send an email to unsubscribe@wellington-altus.ca