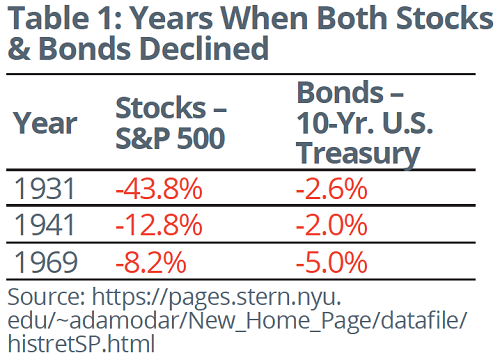

However, in 2022, the stock/bond correlation turned positive, and both asset classes experienced significant declines. This prompted the question: Is the 60/40 portfolio dead? Regardless of the percentage of a portfolio’s allocation to equities and fixed income — 60/40 or 70/30, as examples — last year’s situation demonstrated that diversification isn’t always a sure thing.

However, in 2022, the stock/bond correlation turned positive, and both asset classes experienced significant declines. This prompted the question: Is the 60/40 portfolio dead? Regardless of the percentage of a portfolio’s allocation to equities and fixed income — 60/40 or 70/30, as examples — last year’s situation demonstrated that diversification isn’t always a sure thing.

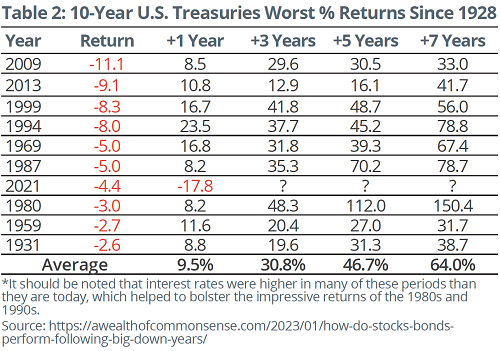

As well, higher yields and the potential for lower volatility are expected to support fixed-income markets. At the time of writing, inflation continues to show signs of easing and the pace of policy rate increases appears to be slowing. Of course, prices could be driven lower and yields higher if economic conditions or fundamentals dramatically change, though it is unlikely we will experience hawkish surprises from the central banks similar to those seen in 2022. Even if prices do remain volatile in the short term, consider that yields are now at highs not seen in decades.1 Higher income, through increased yields, contributes to supporting total returns over time.

As well, higher yields and the potential for lower volatility are expected to support fixed-income markets. At the time of writing, inflation continues to show signs of easing and the pace of policy rate increases appears to be slowing. Of course, prices could be driven lower and yields higher if economic conditions or fundamentals dramatically change, though it is unlikely we will experience hawkish surprises from the central banks similar to those seen in 2022. Even if prices do remain volatile in the short term, consider that yields are now at highs not seen in decades.1 Higher income, through increased yields, contributes to supporting total returns over time.

The information contained herein has been provided for information purposes only. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information has been provided by J. Hirasawa & Associates and is drawn from sources believed to be reliable. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document. Wellington-Altus Private Wealth Inc. (WAPW) and the authors do not guarantee the accuracy or completeness of the information contained herein, nor does WAPW, nor the authors, assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact me for individual financial advice based on your personal circumstances. WAPW is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. ©️ 2023, Wellington-Altus Private Wealth Inc. ALL RIGHTS RESERVED. NO USE OR REPRODUCTION WITHOUT PERMISSION