A Cascading Life Insurance Strategy

Some HNW grandparents are using insurance to pass along a legacy to grandkids while achieving estate planning benefits. With a cascading strategy, a grandparent would purchase a permanent life insurance policy on their adult child (as contingent owner) and name a grandchild as the beneficiary. The cash value could be accessed by the adult child to help pay for educational costs for the grandchild. Upon death, the policy’s ownership would be transferred to the adult child on a tax-free basis. When the adult child passes away, the grandchild would receive the death benefit on a tax-free basis. (It is important to note that the death benefit could be reduced by any withdrawals from the policy.) For estate planning, this would facilitate a generational transfer of wealth with no income tax consequences or probate fees (where applicable) and protect against potential claims of estate creditors.

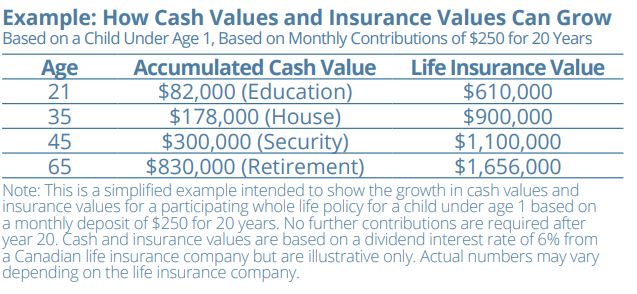

For HNW investors, life insurance may provide benefits beyond protection, including helping to support the growing education costs of a child or grandchild. To explore this or other ideas, please get in touch. *In this example, the $250 monthly contributions to the RESP would end in year 17 when the $50,000 RESP maximum contribution limit is reached, but contributions are assumed to continue until year 20 in a non-registered account. This is intended to provide a comparable example. The $133,000 outcome represents the growth of the RESP and non-registered account combined.

A Cascading Life Insurance Strategy

Some HNW grandparents are using insurance to pass along a legacy to grandkids while achieving estate planning benefits. With a cascading strategy, a grandparent would purchase a permanent life insurance policy on their adult child (as contingent owner) and name a grandchild as the beneficiary. The cash value could be accessed by the adult child to help pay for educational costs for the grandchild. Upon death, the policy’s ownership would be transferred to the adult child on a tax-free basis. When the adult child passes away, the grandchild would receive the death benefit on a tax-free basis. (It is important to note that the death benefit could be reduced by any withdrawals from the policy.) For estate planning, this would facilitate a generational transfer of wealth with no income tax consequences or probate fees (where applicable) and protect against potential claims of estate creditors.

For HNW investors, life insurance may provide benefits beyond protection, including helping to support the growing education costs of a child or grandchild. To explore this or other ideas, please get in touch. *In this example, the $250 monthly contributions to the RESP would end in year 17 when the $50,000 RESP maximum contribution limit is reached, but contributions are assumed to continue until year 20 in a non-registered account. This is intended to provide a comparable example. The $133,000 outcome represents the growth of the RESP and non-registered account combined.

The information contained herein has been provided for information purposes only. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information has been provided by J. Hirasawa & Associates and is drawn from sources believed to be reliable. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document. Wellington-Altus Private Wealth Inc. (WAPW) and the authors do not guarantee the accuracy or completeness of the information contained herein, nor does WAPW, nor the authors, assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact me for individual financial advice based on your personal circumstances. WAPW is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. ©️ 2023, Wellington-Altus Private Wealth Inc. ALL RIGHTS RESERVED. NO USE OR REPRODUCTION WITHOUT PERMISSION