There are many reasons to consider a Registered Education Savings Plan (RESP) to save for a child’s future education: tax-deferred growth within the plan, earnings taxed at the child’s tax rate when eventually withdrawn and, of course, the Canada Education Savings Grant (CESG). The CESG consists of funds paid into the plan by the federal government as a 20 percent matching grant, to an annual maximum of $500 ($1,000 if there’s unused grant room from a previous year) and a lifetime maximum of $7,200 per beneficiary. There are no annual limits on RESP contributions, however, the lifetime limit is $50,000.

Conventional wisdom suggests we should take advantage of the CESG – after all, it’s essentially ‘free’ money. But is this always the best decision? One way to maximize the CESG involves contributing $2,500 per year over 15 years to receive the full $7,200 in grants. However, will this achieve the greatest outcome for the RESP?

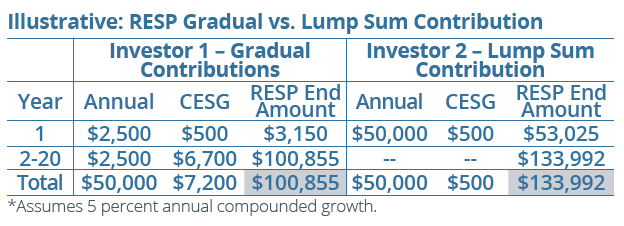

To answer this question, let’s compare investor 1, who gradually contributes and maximizes the CESG, and Investor 2, who contributes a lump sum amount and doesn’t maximize the CESG. The outcome may be surprising. Both investors are assumed to earn an annual rate of return of 5 percent. Investor 1 contributes $2,500 each year starting in the first year of the child’s life until year 20, to a maximum contribution of $50,000, and receives the full $7,200 CESG grant. After 20 years, the RESP produces $43,655 of growth, resulting in a value of $100,855. Investor 2 contributes a lump sum of $50,000 – the full RESP limit – in the first year of the child’s life, so the RESP receives only $500 of CESGs. Yet, the RESP grows to $133,922 over the same period.

This shows the profound impact of compounding over time. Front loading the initial contribution yields a larger outcome, even without receiving the full CESG, all else being equal. Despite lower total contributions (funds paid into the plan plus CESGs) for investor 2, or $6,700 less in CESGs, the outcome is $33,137 greater.

A Lesson for the RESP – And Investing in General

Of course, not many investors have $50,000 of discretionary funds at the start of a child’s life. As such, maximizing the CESG where possible is a prudent strategy. Yet, this example illustrates why, as advisors, we often remind investors not to overlook the impact that compounding can have over time on any investment – not just RESP. One takeaway? The sooner you start, the more time funds have to grow and, when it comes to growth, the larger the initial investment, the better.

| When was the last time you reviewed account beneficiaries?

A recent article in the Wall Street Journal is a reminder: “His Ex Is Getting His $1 Million Retirement Account. They Broke Up in 1989.” Before year end, consider reviewing account beneficiaries, especially if you’ve left a job or had changing life circumstances. If you need assistance with investment accounts, please call. |