Trade and Tariffs: Perspectives on Where We Stand Today

As renegotiations over the U.S.-Mexico-Canada Agreement (USMCA) approach, it’s worth taking a brief look at trade to share perspectives on the framework that has governed North American trade since July 2020. The USMCA replaced the North American Free Trade Agreement (NAFTA), which as designed to support an integrated market based on free trade. It provides reciprocal tariff-free access among members, provided certain rules are met. Together, these agreements have shaped supply chains, supported investment and increased trade flows across North America for decades.

One of the greatest beneficiaries of the agreement has been the automotive sector, due to the scale, complexity and integration of supply chains across the continent. To qualify for zero tariffs, automobiles must meet strict regional value content thresholds, generally requiring that at least 75 percent of components be produced in North America, along with wage-related labour requirements. Production is now deeply integrated, with components often crossing borders multiple times during assembly.

In Brief: Where We Stand Today

Given geographic proximity, Canada and the U.S. have long had extensive trade relations. Without a doubt, Canada’s dependence on the U.S. is substantial: roughly two-thirds of total exports go to the U.S., representing around 24 percent of Canada’s GDP.1

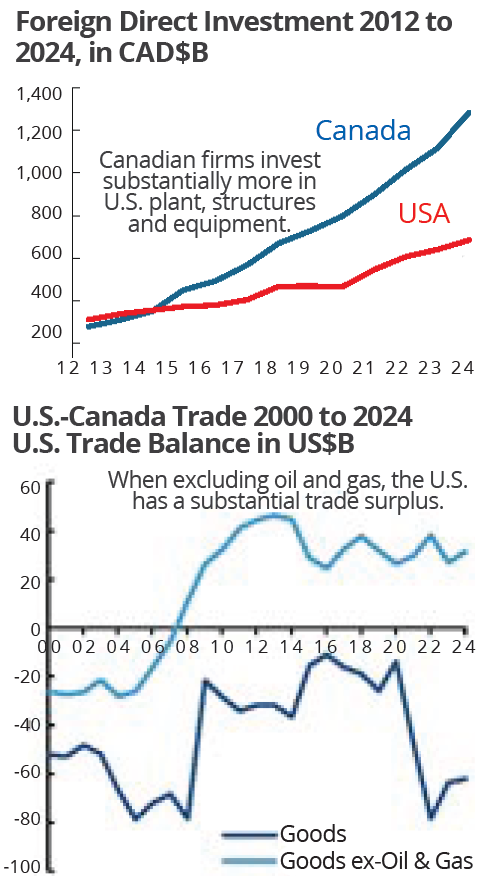

However, it’s not all one-sided. Claims that Canada is being “subsidized” overlook substantial reverse flows. Canadian firms invest more in U.S. plant, structures and equipment than U.S. firms invest in Canada. About 59 percent of Canadian imports come from the U.S., representing roughly one-quarter of Canada’s GDP, while the U.S. has a non-energy trade surplus with Canada (see charts).1

The Path Forward

Many economists expect the USMCA to survive in some form, likely on terms favourable to the U.S. A full dismantling would risk inflation, job losses and supply-chain disruption, particularly during a U.S. midterm election cycle.

It’s also worth noting that existing U.S. tariffs have had adverse effects on Americans. According to a report by the Federal Reserve Bank of New York, roughly 90 percent of the economic burden of the tariffs was borne by U.S. firms and consumers through 2025 . Until now, they haven’t triggered broad inflation, largely because many firms initially absorbed the cost through slimmer margins or cost-cutting measures. But that buffering has limits. Recent reports suggest companies under sustained cost pressure are increasingly raising, or planning to raise, prices.2 This comes at a time when many Americans are already struggling with affordability.

Other economic effects have been more visible:

U.S. manufacturing has weakened. The expected tariff-driven revival has not materialized. More than 200,000 manufacturing jobs have been lost since 2023, and the Institute for Supply Management index of factory activity declined for 26 consecutive months through December 2025. Since many manufacturers rely on imported inputs, tariffs often raise production costs more than they provide protection.

Retaliation has had tangible consequences. While China suspended many retaliatory tariffs in 2025, it left duties on soybeans for most of the year, cutting off what had historically been the largest U.S. export market, worth roughly US$12 billion

Retaliation has had tangible consequences. While China suspended many retaliatory tariffs in 2025, it left duties on soybeans for most of the year, cutting off what had historically been the largest U.S. export market, worth roughly US$12 billion

annually. By October 2025, five consecutive months had passed without a single U.S.

soybean export to China,3 an unprecedented stretch, prompting roughly $12 billion in U.S. farm support by December. Purchases resumed before the month’s end, following a meeting between Trump and Xi Jinping.

Closer to home, Canadian travel to the U.S. has dropped sharply over the past year, with an estimated US$4.5 billion in lost tourism revenue.4 Last year, it was reported that U.S. spirits exports to Canada, valued at about $250 million annually, were down by 85 percent.

Political pressure is rising. The economic effects of tariffs are translating into political action. In February, six Republican senators joined Democrats in supporting the repeal of tariffs on Canada, breaking with President Trump. While a full repeal remains unlikely, the vote signalled mounting concern about their economic impact.

1.https://www.scotiabank.com/ca/en/about/economics/economics-publications/post.other-publications.global-week-ahead.january-23–2026.html

2. https://www.wsj.com/business/price-increases-consumers-businesses-b70e4542

3.https://www.forbes.com/sites/kenroberts/2026/01/17/china-purchased-no-ussoybeans-an-unprecented-sixth-straight-month/

4. https://www.forbes.com/sites/suzannerowankelleher/2026/02/12/canadian-visits-falljanuary-trump-slump/

The information contained herein has been provided for information purposes only. The information has been drawn from sources believed to be reliable. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document. Wellington-Altus Private Wealth Inc. (WAPW) does not guarantee the accuracy or completeness of the information contained herein, nor does WAPW assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact your financial advisor. Transactions of the type described herein may involve a high degree of risk, and the value of such instruments may be highly volatile. Such risks may include without limitation risk of adverse or unanticipated market developments, risk of issuer default and risk of illiquidity. In certain transactions prospective investors may lose their entire investment or incur an unlimited loss. This brief statement does not disclose all the risks and other significant aspects in connection with transactions of the type described herein, and prospective investors should ensure that they fully understand the terms of the transaction, including the relevant risk factors and any legal, tax, regulatory and accounting considerations applicable to them, prior to transacting. The information contained herein may include the opinions of representatives of third-party companies or organizations and may not necessarily reflect that of Wellington-Altus (WA) or its representatives. All third-party products and services referred to or advertised are sold by the company or organization named. While WA may have referral arrangements with some third-party companies or organizations, WA does not specifically endorse any of these products or services and is not liable for any claims, losses or damages however arising out of any purchase or use of third-party products or services. All insurance products and services are offered by life licensed advisors of Wellington-Altus Insurance Inc. or other insurance companies separate from WAPW.

© 2026, Wellington-Altus Private Wealth Inc. ALL RIGHTS RESERVED. NO USE OR REPRODUCTION WITHOUT PERMISSION. www.wellington-altus.ca

If you no longer wish to receive commercial electronic messages from Wellington-Altus Private Wealth Inc., please send an email to unsubscribe@wellington-altus.ca