The great disconnect: strong markets, strained consumers

The current cycle is increasingly defined by a K-shaped divergence in which strong corporate earnings, artificial intelligence (AI)-driven capital spending, and resilient equity markets stand in sharp contrast to a weakening consumer facing mounting affordability pressures, softening sentiment, and rising economic strain beneath the surface. While Wall Street continues to benefit from concentrated wealth, robust profit margins, and unprecedented investment in technology, Main Street is contending with higher costs, declining discretionary spending, and fragile confidence, raising the central question of whether a pressured consumer ultimately drags the economy into recession or whether asset-rich households can continue to sustain growth. At the same time, rising bond yields and elevated debt levels are limiting policy flexibility, creating a stop-go environment that heightens the risk this divergence persists until either economic conditions deteriorate more meaningfully or policymakers are forced to respond.

Private markets, public lessons

We have been watching a familiar pattern unfold, with retail capital steadily moving into parts of the market closer to their peak under the banner of exclusivity and access, much like the “hot deals” once passed down from capital markets desks to advisors and on to clients, only now repackaged as private equity and private credit opportunities. These strategies were built in an era of falling rates, abundant liquidity, and a relentless search for yield — conditions that flattered returns and masked risk — and are now being introduced more broadly just as the cost of capital has reset higher and those same assumptions are being tested. The appeal often rests in what is not seen, as the absence of daily pricing creates the illusion of stability, even though the underlying businesses face the same pressures, risks, and cycles as their public counterparts. What ultimately changes in stress is not just outcomes but the investor’s ability to respond, as liquidity, flexibility, and behaviour become constrained at precisely the wrong time. While private markets can play a role, they were designed for institutional investors with permanent capital and long horizons, not individuals with real world liquidity needs, which makes sizing and suitability far more important than access. In the end, the pattern does not change, only the wrapper does, and if something appears consistently attractive while being widely distributed, it is worth remembering that if you cannot identify the mark at the table, it is probably you.

The importance of emotional stewardship in manager selection

Fiduciary duty is often defined in terms of regulation, process, and acting in a client’s best interest, but in practice its deeper meaning is frequently overlooked, particularly in volatile markets where emotional pressure can quietly shape decisions before it is fully recognized. True stewardship extends beyond portfolio construction and compliance into the ability of a portfolio manager to remain emotionally grounded when uncertainty rises, as markets themselves reflect human behaviour and can transmit stress in subtle but powerful ways. Research shows that people respond to fear instinctively and often unconsciously, and this dynamic plays out in financial markets where anxiety can compress time horizons and lead to poor decisions at precisely the wrong moments. As a result, managing capital ultimately begins with managing oneself, and the most reliable stewards are those who combine technical skill with emotional discipline, maintaining clarity and composure when it matters most so they can guide clients safely through inevitable periods of market stress.

Finally, some exciting news, our very own Martin Pelletier has written a book that will be published this upcoming December by Harriman House. It’s entitled Investing Through the Storm, and takes his years of investing experience and transforms it into a modern guide for navigating today’s increasingly unpredictable financial landscape. PRE-ORDER your copy here.

Please reach out to any of our team members should you have any comments or questions about markets, your portfolio or just wanting to catch up.

Your TriVest Team

May 2026

The great disconnect: strong markets, strained consumers

It is becoming increasingly clear that we are operating in a K-shaped economy, where the lived experience of Main Street is diverging sharply from the reality reflected in markets.

On one side, consumers are grappling with affordability pressures from housing to lingering inflation, higher tariffs, and growing anxiety around job security as AI reshapes the labour market. On the other, a corporate economy is thriving on AI-driven capital spending, resilient profit margins, and equity markets that remain largely indifferent to escalating geopolitical tensions.

The central question in the United States is whether a weakening consumer ultimately tips the economy into recession, especially if commodity and energy prices move higher, or whether a wealthier, asset-owning cohort continues to carry growth, supported by elevated financial markets. What happens in the U.S. is key, not only given its dominance in global capital markets and its disproportionate influence on asset prices and economic conditions but, as the saying goes, when the U.S. sneezes, Canada catches a cold.

Wall Street is winning

This cycle continues to be defined by a divergence that appears likely to persist longer than many expected, supported by a wealthy, asset-owning cohort and an unprecedented wave of AI-driven investment that may keep certain segments of the market moving higher.

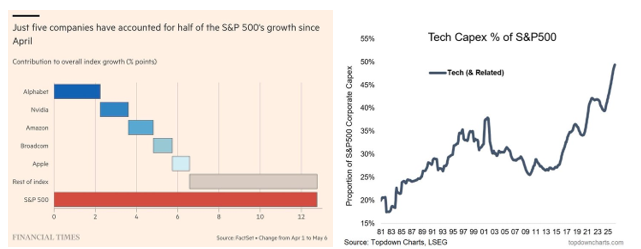

First-quarter earnings were exceptionally strong — one of the best quarters in two decades according to Deutsche Research — with roughly 84 percent of the two-thirds of S&P 500 companies that have reported beating expectations, well above long-term averages. Blended year-over-year earnings growth for the index is running near 27 percent, more than double initial analyst forecasts, while aggregate net margins have climbed to 13.4 percent, the highest level in more than a decade.

Capital spending offers an equally powerful signal. Just four hyperscalers — Amazon.com Inc., Microsoft Corp., Alphabet Inc. (parent of Google), and Meta Platforms Inc. — are guiding toward roughly US$700–$725 billion in combined capital expenditures for 2026, largely tied to data centres, chips, power infrastructure, and AI build-outs.

Companies do not commit resources on this scale if they are worried about the next few quarters, and so this long-duration spending is rooted in strategic conviction — for now.

However, that strength is coming with growing consequences for Main Street, where affordability pressures are building and weighing on more consumer-sensitive areas of the economy.

Main Street is telling a very different story

The core consumer is under increasing strain as affordability erodes, although part of that pressure is being masked by wealthier, asset-owning households, particularly baby boomers, who remain supported by strong markets and continue to spend. That dynamic is helping sustain overall consumption, even as underlying conditions soften.

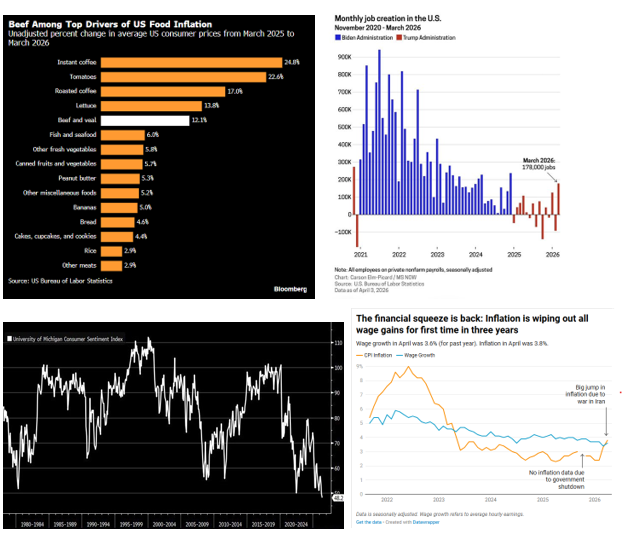

Beneath the surface, the U.S. domestic economy is sending less reassuring signals. The National Federation of Independent Business (NFIB) Small Business Optimism Index fell to 95.8 in March, below its 52-year average and the weakest reading in nearly a year, as input costs rise while pricing power softens. Consumer sentiment reflects a similar unease, with the University of Michigan Index dropping to 49.8 in April, near levels last seen during the 2022 inflation shock, and weakness evident across income groups, age cohorts, and political lines.

That stress is beginning to show in discretionary spending. New vehicle sales are tracking toward a decline of roughly 2.6 percent this year, with several months already showing double-digit year-over-year drops, while the ratio of leading to coincident indicators has slipped to 0.84, a level consistent with past recessions, including the Global Financial Crisis.

At TriVest Wealth Counsel, we see a risk that these pressures intensify before they ease. Government efforts to secure critical resources, alongside massive investment tied to AI, are pushing commodity prices higher. Rising costs for power, water, and energy are feeding directly into affordability challenges, increasing the risk of broader economic strain and even public pushback against the very infrastructure currently supporting corporate earnings.

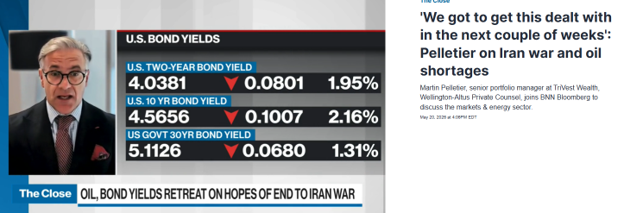

Rising yields leave little room for error

The elephant in the room few want to talk about is the bond market. With yields rising, currencies under pressure, and sovereign debt levels elevated, policymakers have limited room to respond if conditions deteriorate. Cutting rates into volatile energy prices risks reigniting inflation, yet maintaining higher-for-longer rates steadily increases government debt-service burdens. The result is a stop-go environment oscillating between growth scares and inflation scares.

Japan offers the clearest warning. After decades of ultra-low yields, rising Japanese rates and periodic currency intervention show how bond markets can force painful policy trade-offs. If one large, developed economy faces this constraint, investors inevitably begin asking which country is next. In this context, the K-shaped economy is not just a snapshot of today’s divergence. It may be the defining risk of the cycle ahead.

How to position portfolios?

For investors, this divergence creates real tension. What they are experiencing in their daily lives often feels disconnected from what markets are signaling, and that gap is understandably unsettling. Yet stepping aside entirely has carried its own cost, as those who moved to cash have missed meaningful upside while exposing their capital to the quieter risk of erosion through inflation and currency debasement.

A more durable approach is to remain invested but with a deliberate structure that recognizes the risks that lie beneath the surface. This is easier said than done though, especially with an industry built on telling you to simply buy, hold, and ride out near-term volatility.

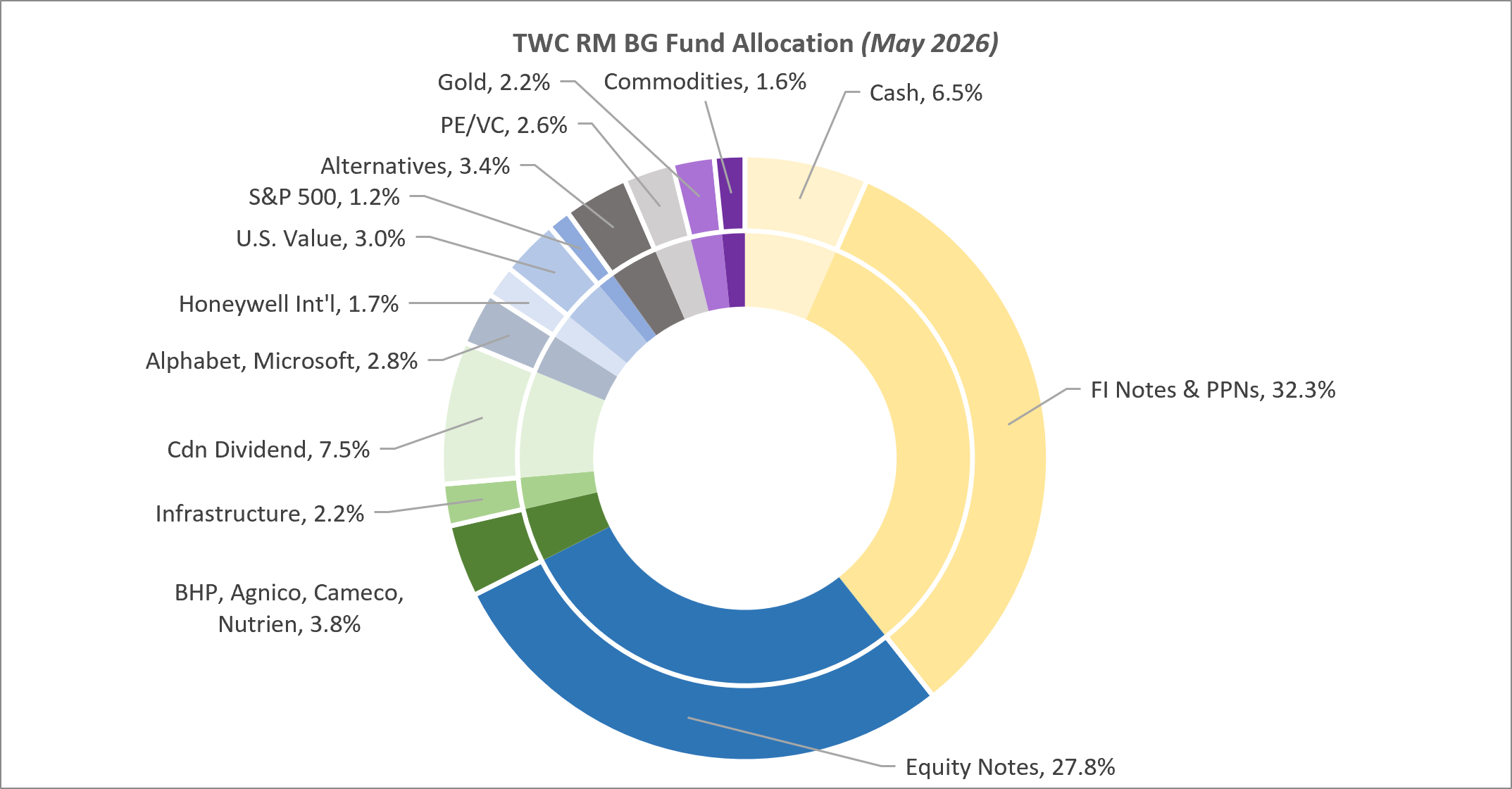

In our case, we prefer a less traditional and more active risk-managed approach. For example, this has meant stepping away from traditional fixed income and instead using structures such as principal-protected notes and extendible linear accruals (structured fixed-income investments that offer higher yields than traditional bonds).

For example, we recently sold a note within registered accounts that made a 100 percent return in just over a year due to the levered upside. We redeployed the proceeds into a number of new notes with large, embedded downside and monthly or annual coupons ranging from 7 to 12 percent. We also created a large booster twin win note on Canadian large caps that, as long as it is -35 percent or higher, it will receive a 27.5 percent positive return in 3 ½ years with full tracking should the large caps deliver a higher return than 27.5 percent.

On our equity portfolio, we have shifted exposure away from areas most sensitive to the strained consumer, favouring segments of the market supported by structural capital flows and policy tailwinds. This includes global infrastructure, materials, and direct commodity exposure, all of which stand to benefit from the scale of investment tied to the AI build-out and resource security.

Complementing this are high-quality Canadian dividend-paying companies operating within oligopolistic industries, where durable competitive advantages are reinforced by regulatory frameworks that limit competition and support stable cash flows.

All of this is resulting in some very favourable results for our client portfolios. As at the end of April, our TWC Risk-Managed Balanced Growth Fund is up 8.9 percent this year-to-date and 26.3 percent over the past 12 months.

Looking ahead, we worry that this cycle may not resolve with a clean handoff between Wall Street and Main Street, but rather with tension that persists until something breaks or policy is forced to respond. Until then, markets may continue to climb on strong capital flows and earnings, even as the underlying economic foundation grows more fragile. And we are ready for it.

Private markets, public lessons

We have been watching a familiar pattern unfold over the past few years, with retail investors steadily moving into a segment of the market closer to its peak. I wrote about this years ago, drawing on lessons from my time as a research analyst, when I noticed that underwater bought deal equity offerings were being handed off, along with the associated commissions, from capital markets desks to investment advisors and then repackaged and marketed to clients as a so called “hot deal.”

The intent is to signal exclusivity and sophistication by offering access to strategies that were once the domain of pensions and endowments, and while that access can be real in a narrow sense, it rarely comes without cost. At some point it becomes a matter of applying some basic common sense, because one has to ask why an opportunity would be sliced into thousands of small allocations for individuals rather than placed in a single transaction with a large institution that has the scale, resources, and bargaining power to take it down.

For much of the past decade private equity and private credit were built and sold in a world defined by falling rates, abundant liquidity, and a persistent search for yield, which encouraged investors to move further out on the risk spectrum in exchange for incremental return. As rates compressed and traditional fixed income offered little in the way of income, private credit in particular emerged as an attractive alternative, while private equity benefited from cheap financing, rising multiples, and an environment that allowed time and leverage to do much of the work.

Now that rates have moved off their lows and the cost of capital has reset higher, these strategies are increasingly being brought to a broader audience in search of incremental demand, arriving at a point in the cycle where the assumptions that supported their past success are beginning to be tested.

Part of the appeal of private investments lies in what is not seen, because without continuous market pricing the volatility appears muted and the return profile looks smoother, which can create the impression of stability and control. In truth, this is often just the absence of a quotation rather than the absence of risk. For example, if you were to price your home every day, you would likely experience the same swings that investors endure in public markets. However, because that does not happen, you rely on occasional appraisals and only discover its true value when you go to sell. The underlying economics of the asset do not change simply because they are not being constantly observed.

The businesses held within private structures are no different from their public counterparts in that they are still subject to margin pressure, refinancing risk, competitive threats, and economic cycles. Defaults still occur even if they are less visible along the way. What changes during periods of stress is not only the eventual outcome of the investment, but also the investor’s ability to respond in real time, as liquidity, flexibility, and behaviour move from being secondary considerations to the primary drivers of experience. It is precisely here where private market structures tend to impose the greatest constraints at the exact moment they matter most.

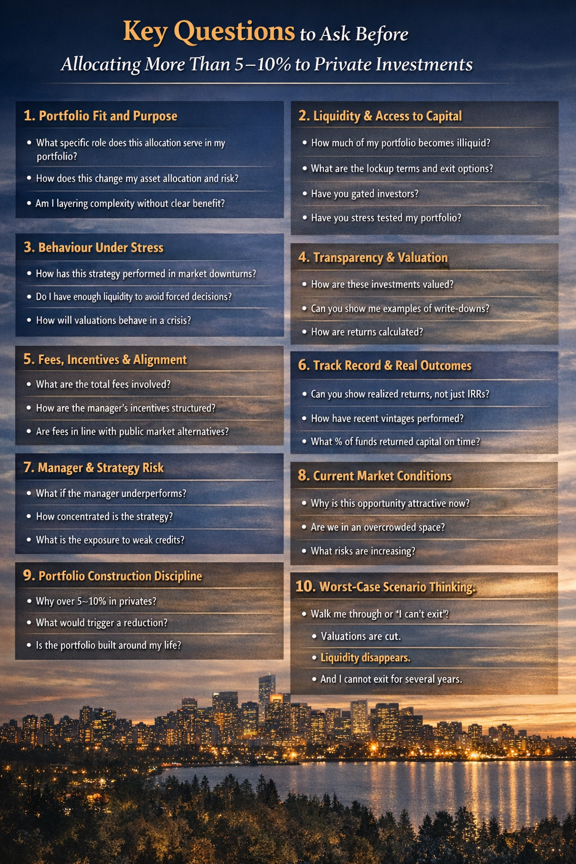

The issue is not that private markets are inherently flawed or unworthy of consideration, but rather that their design can amplify problems for individual investors if approached without discipline, given illiquidity, limited transparency, and incentive structures that tend to favour larger investors with incredibly long time horizons. Institutional and family office portfolios are built around a very different set of conditions, including effectively permanent capital, predictable inflows, long governance cycles, and, most importantly, the ability to remain invested through difficult periods without being forced into action, which is a constraint most families simply cannot replicate.

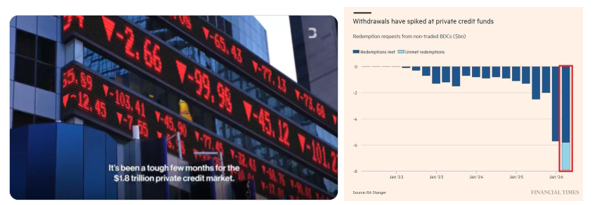

Fast forward to today and we are now beginning to see some of these risks materialize particularly within private credit, where rapid growth has brought the asset class to a scale that is now being tested by tightening financial conditions and rising borrower stress.

The conclusion is not that private investments should be avoided altogether, because they can play a useful role in a portfolio diversification by providing exposure to areas of the economy that are not publicly listed and by offering differentiated sources of return. The mistake is in treating them as a straightforward upgrade to traditional portfolios rather than as distinct instruments with their own advantages, limitations, and behavioural implications, which require a different mindset and a higher tolerance for uncertainty around timing and liquidity.

In practice, the real question is more of sizing and suitability rather than access, as a high-net-worth investor with stable cash flow, a long time horizon, and a clear understanding of how these structures behave under stress may choose to allocate a modest portion of capital to them. For most individuals, this points to a range that is measured often in the area of five to 10 percent, and even then, it requires that you are being compensated appropriately for the illiquidity risk you are taking on.

And if you are being sold anything that simply looks too good to be true, remember that old poker saying that if you sit down at the table and cannot identify the mark, it is probably you. That’s a hot deal that you may just want to pass on.

The importance of emotional stewardship in manager selection

One of the discussions that comes up most often in the investment industry is fiduciary duty, yet it rarely receives more than a surface level examination. I’ve had this conversation many times with advisers and portfolio managers, and what has consistently stood out is how differently the concept is interpreted and how easily its deeper meaning can be blurred.

At its core, a fiduciary is someone entrusted with something that is not their own. In portfolio management, trust is placed in overseeing capital that took years of hard work to accumulate and is meant to support future security and peace of mind. The responsibility that follows is clear in principle: act in clients’ best interest, place their needs ahead of your own, avoid conflicts, and exercise care, diligence, and loyalty in every decision.

Most discretionary portfolio managers understand this definition intellectually. Fiduciary duty is built into regulation, reinforced through compliance and referenced frequently in marketing materials. Yet in practice, it is often treated as if it lives primarily in portfolio construction, documented process, and disclosure. Those elements are certainly very important, but they capture only part of what true stewardship demands, particularly in today’s environment, which is characterized by uncertainty and rapid change.

Stewarding capital through volatile markets requires more than sound models and disciplined frameworks; it requires the capacity to remain emotionally grounded when pressure builds. A portfolio manager who struggles to maintain composure during times of stress places the very trust they are meant to protect at risk, regardless of how thoughtful their strategy appears during calmer periods.

Markets themselves are not neutral forces. They reflect a constant aggregation of human behaviour, emotion, and expectation, which is why they have a way of provoking reaction when uncertainty rises. Long stretches of patience are often followed by sudden tests that compress decision making and reward clarity of mind over speed. In those moments, portfolio managers are not only managing risk and capital, they are managing themselves in an environment where fear seeks a response.

This challenge is rooted deeply in human biology. Research outside of finance has shown that people are highly sensitive to the emotional states of others, often in ways that bypass conscious awareness altogether. In one well-known set of experiments, researchers collected sweat samples from two groups of individuals, one calmly exercising on a treadmill and the other preparing for a first-time skydive. The samples were deodorized so no identifiable smell remained, and participants could not consciously tell them apart.

Their bodies, however, responded quite differently. Exposure to sweat taken from the skydivers led to elevated heart rates and heightened physiological responses associated with fear and vigilance, while the treadmill samples produced no such effect. Stress was communicated chemically, without words, expressions, or conscious detection, and behaviour shifted before the mind had time to interpret what was happening.

Financial markets operate in much the same way. Fear rarely arrives with an announcement. It emerges quietly through tone, pacing, defensiveness, and urgency, shaping behaviour beneath the surface before it is fully understood. When it appears, effective portfolio stewardship depends on having both the discipline and the emotional regulation required to manage that response on behalf of the wealth entrusted to them.

This is why emotional self-regulation belongs at the centre of fiduciary responsibility. Managing capital for others begins with managing personal reactions. Under emotional strain, thinking narrows, time horizons shorten, and behaviour drifts toward instinctive fight-or-flight responses, which have a way of producing poor decisions at precisely the wrong moments.

The industry offers no shortage of examples. Sound processes abandoned near market lows because pressure became overwhelming; investment teams destabilized by unaddressed fear; and portfolios unable to survive market cycles.

True stewardship rests on emotional reliability alongside intelligence, experience, and technical skill. When choosing someone to oversee your wealth, it is worth asking about periods when they faced genuine emotional pressure, both in life and in markets, and how they navigated those moments. Understanding how a portfolio manager regulates their behaviour offers insight into how steady they are likely to be when conditions become difficult.

When it comes to handing over your wealth, trust becomes everything. Managing money feels straightforward during quiet periods, much like running comfortably on a treadmill. Yet markets have a way of forcing sudden, uncomfortable leaps. When that moment arrives, it helps to know that the person you are strapped to, like a skydiving instructor, understands how to stay calm, maintain perspective, and guide you safely through those unexpected market corrections.

Research, in-the-media, reads of the month

“Affordability’s the best it’s been in over a decade.” – Prime Minister Mark Carney, March 2026

A major leak on Main Street If you work for a living, your share of GDP is lower than it ever was. If you are the holder of capital, your share of GDP is higher than ever. See Here “In January, February, and March, 37,121 Canadians filed for insolvencies — amounting to 17 Canadians filing for insolvencies every hour.” Read Here McDonalds Corp. is now trading at its lowest price since 2024. See Here Global food prices climbed to their highest level in more than three years as the Iran war disrupted supply chains, raising the prospect of larger bills for shoppers. The United Nations’ index of food-commodity prices gained 1.6 percent in April from the previous month, led higher by vegetable oils, meat, and cereals, according to a Friday report from the Food and Agriculture Organization. That’s 2.5 percent higher than a year ago. Read Here Looking at the situation facing our youngest labour market participants, 22.3 percent unemployed in April — it has not been this high in over 30 years. See Here

“How Carney’s new sovereign wealth fund could backfire on the economy” “Markets have seen this story before, and they will also remember how it ends.” Read Here “Mark Carney’s new sovereign wealth fund is a solution in search of a problem.” Read Here “The 13 charts that prove the lost Liberal decade.” See Here

“How Europe Is Designing a Tax System You Can’t Escape.”

“The Netherlands is introducing a 36% tax on unrealized investment gains in 2028, even if you don’t sell your assets.” See Here “The European Commission literally just dropped a research bomb on how to collect more taxes without making you angry enough to leave.” Read Here

Trouble on the home front?

U.S. existing home sales over the first four months of 2026 were the lowest since 2009, making this the fourth straight year of recession-level home sales. See Here Just 25 percent of U.S. non-homeowners expect to buy a home within the next five years, the lowest reading since Gallup first asked the question in 2013. This is down from 30 percent in 2025 and from 49 percent in 2017. This shift is most pronounced among younger Americans, with only 29 percent of non-homeowners aged 18–34 expecting to buy within five years, down from 57 percent in 2013–2015. See Here

Bonds?

The U.S. bond market has now been in a drawdown for 69 months, by far the longest in history. See Here What if the biggest bubble of our lifetime isn’t crypto, AI stocks, or real estate? What if it’s the one asset every pension fund, every retiree, and every “safe” portfolio is loaded with: bonds. Two hundred years of rate cycles suggest the same thing: every peak lasts 56–67 years. The 1981 top was 14 percent yields. The 2020 bottom was 0 percent. Thirty-nine years of falling rates may have just ended. See Here

Physical vs financial oil

Dated Brent (physical) traded at a huge premium to Brent futures (financial) in early April. Since then, both markets have come down, with the physical-versus-financial premium completely disappearing. See Here “US gasoline inventories are at their lowest seasonal level for more than a decade.” See Here We do worry about an oil market without OPEC there to provide price stability. Read Here. Martin Pelletier shares our thoughts on oil markets, prices, and the United Arab Emirates leaving OPEC via CBC Radio. Listen Here

There has been a collapse of U.S. domestic uranium production since the 1980s

Domestic output (dark blue) has fallen to almost nothing, while imports (light blue) now supply 95 percent of America’s needs. The U.S. has the world’s largest nuclear reactor fleet (94 plants) and consumes roughly 40–50 million pounds of U₃O₈ per year, yet it produces only about 1 million pounds domestically. See Here

That’s gold

Monetary inflation of 15 percent since early 2025, but reported inflation is roughly 3.5 percent. See Here “Nonmonetary gold” refers to gold traded for commercial, industrial, or investment purposes (bullion, bars, coins, powder, etc.), excluding official monetary gold held by central banks as reserves. It was the single largest export in March, bigger than aircraft, semiconductors, oil, soybeans, pharmaceuticals, or cars, highlighting strong global demand for physical gold. See Here Global gold demand hit a new record high value. See Here Global central bank gold purchases surged 36 tonnes in Q1 2026 to 244 tonnes, the highest since Q4 2024. This significantly exceeds the five-year average of roughly 228 tonnes. By comparison, the five-year average in 2016–2020 was roughly 115 tonnes, or less than half the current level. See Here

“Compute Demand Cures All Ills”

“The real ‘north star for this market’: ‘is AI still improving,’ not 1’s CapEx is 2’s OpEx.” Watch Here “47 stocks in the S&P 500 are currently at or within 2 per cent of a 52-week high. 31 of them are in AI-sensitive industry groups, or roughly two-thirds.” See Here “This is one of the best earnings seasons in 20 years…All 11 top-level sectors are expected to show YoY earnings growth for the first time in 4 years” – Deutsche Bank research. Read Here

On the Positive

Think about this, these albums were all released within 57 days of each other in 1991.

Living on a prayer

Hard work, you are not your success, knowing what matters in life and staying grounded. Some sage advice from one of my favourite rock artists. Watch Here

Forget happiness, be grateful

Every once in a while, we all need a good old-fashioned reminder that we can either make progress or excuses, but we can’t make both. In today’s world, we’re hearing way too many of the latter and way too little of the former. A great first step is to be grateful for the progress made in one’s day and making it a habit to eventually change your mindset. How are you going to end your day, and week?

Progress or excuses?

One of the most important things I’ve learned over the past few years is that the two biggest obstacles to maximizing your life, wealth, and health are fear and ego. Fear keeps you stuck. Ego convinces you you’re already right. Together, they show up as stubbornness and an unwillingness to adapt and that’s exactly where progress goes to die.

Mini livers

“MIT engineers have developed ‘mini livers’ that could be injected into the body and take over the functions of the failing liver.” This would help patients who are on a waitlist for a liver transplant or those who aren’t healthy enough to tolerate surgery. Read Here

Gamestopped

An absolutely hilarious interview. Watch Here

That red circle is the data centre

Everything else is the solar farm powering it. See Here

Lessons from Jeff Bezos’s private retreat

When you can buy your way out of any mistake, when you can fire anyone who disagrees with you, when your social circle consists entirely of people who need something from you, the basic mechanism by which humans learn that other people are real goes dark. Read Here

What are we leaving behind?

“The truth hurts sometimes but how can we improve if we don’t acknowledge the problems. We have a responsibility when it comes to technology and our kids and we’re failing miserably.” Watch Here There are no maverick molecules in the universe. Watch Here Humility is starting where you are. Watch Here

“The best 3 minutes of video I’ve watched this year.”Watch Here and Jon Hamm’s closet picks. Watch Here

To find out more about the TriVest team and how we manage wealth, follow us on Twitter, or LinkedIn. Please email us if you want to find out more about our services.

Trivest Wealth is a trade name of Wellington-Altus Private Counsel Inc. (WAPC). WAPC is a Portfolio Manager and Investment Fund Manager registered with the Manitoba Securities Commission as its primary regulator. The advisors associated with Trivest Wealth are registered with WAPC. WAPC is a subsidiary of Wellington-Altus Financial Inc. The information contained herein has been provided for information purposes only. The information has been drawn from sources believed to be reliable. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document.

Transactions of the type described herein may involve a high degree of risk, and the value of such instruments may be highly volatile. Such risks may include without limitation risk of adverse or unanticipated market developments, risk of issuer default and risk of illiquidity. In certain transactions counterparties may lose their entire investment or incur an unlimited loss. This brief statement does not disclose all the risks and other significant aspects in connection with transactions of the type described herein, and counterparties should ensure that they fully understand the terms of the transaction, including the relevant risk factors and any legal, tax, regulatory and accounting considerations applicable to them, prior to transacting. This report may contain links to third-party websites. WAPC is not responsible for the content of any third-party website or any linked content contained in a third-party website. The inclusion of a link in this report does not imply any endorsement by or any affiliation with WAPC.

Structured Notes are not suitable for all investors. The notes do not pay dividends, and any dividends paid on the underlying constituent’s may not factor into the return calculation that determines your return. The protection and potential augmented returns on these notes are only available when

Wellington-Altus Private Counsel Inc. (WAPC) does not guarantee the accuracy or completeness of the information contained herein, nor does WAPC assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact your financial advisor.

Wellington-Altus Private Counsel is registered as a Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland & Labrador, Nova Scotia, Northwest Territories, Nunavut, Ontario, PEI, Quebec, Saskatchewan, Yukon and an Investment Fund Manager in Alberta, Manitoba, Ontario, and Quebec.

All trademarks are the property of their respective owners.

© 2026, Wellington-Altus Private Counsel Inc. ALL RIGHTS RESERVED.

NO USE OR REPRODUCTION WITHOUT PERMISSION.

www.wellington-altus.ca