When bond markets start talking

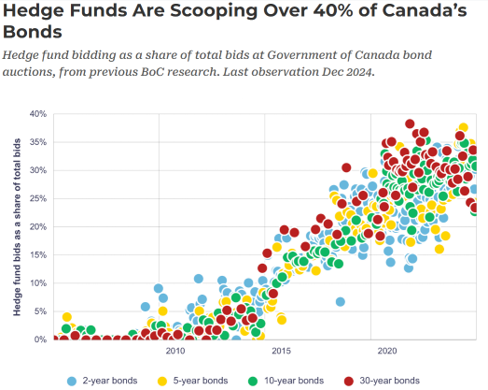

Few if any know that offshore hedge funds are now buying a massive 40 to 50 per cent of newly issued Government of Canada bonds. That level of participation reflects a meaningful change in the composition of demand over the years, as it was only five to 10 per cent a decade or more ago. This is important for many reasons including measuring the level of global liquidity and sovereign debt risks.

Dialing back risk amid market strength

Markets have had a remarkable run. Over the past 12 months, it’s been one of the strongest periods we’ve seen for client portfolios. At times like this, the question becomes less about chasing returns and more about managing what we’ve already earned. There is always a temptation to press harder when markets are working. We take a different approach. After strong performance, discipline matters more than ambition.

Sandboxes and motorcycles

When it comes to managing wealth over many years, I have come to realize that its true value extends well beyond money. Building a nest egg to support a desired lifestyle in retirement is a common and worthwhile goal but the problem is that the habits we rely on to get there often end up standing in the way of finally enjoying it.

Time is by far your most valuable currency, and its importance sharpens with age, especially as it seems to accelerate. I wrote about this before in a piece titled: If life gets shorter, like a roll of toilet paper, why do we work so long? It sounds flippant, but the point is quite serious. The closer you get to the end, the more aware you become of just how finite your time really is.

Please reach out to any of our team members should you have any comments or questions about markets, your portfolio or just wanting to catch up

Your TriVest Team

June 2026

When bond markets start talking

Once in a while, something meaningful turns up in a place most people would not think to look, and we have found that more often than not it begins in the bond market. For example, we recently discovered that hedge funds were the major buyers of newly issued United States Treasury debt and it got me wondering if this is also happening in Canada, who these hedge funds were, why they were doing so, are there any auxiliary effects and what would be the consequences if they stopped?.

This brought us to the Bank of Canada’s (BoC) 2025 Financial Stability Report thanks to a piece we came across in Better Dwelling that appeared to go down the same rabbit hole. According to the BOC report, hedge funds are now buying a massive 40 to 50 per cent of newly issued Government of Canada bonds. That level of participation reflects a meaningful change in the composition of demand over the years, as it was only five to 10 per cent a decade or more ago.

The strategy itself isn’t that complicated. Capital is borrowed in short-term funding markets, often tied to overnight rates such as Canadian Overnight Repo Rate Average (CORRA), and deployed into longer-dated government bonds across the five-, ten- and sometimes thirty-year maturities. The return comes from the spread between those funding costs and bond yields, while using leverage to make what would otherwise be modest differences more meaningful. The trade can also produce significant gains when longer-term yields fall and the yield curve flattens.

Demand for government bonds therefore becomes directly tied to the shape of the yield curve. As long as the spread between short-term rates and longer-term yields remains sufficient and there is a continued expectation that longer-term rates will drop, the trade attracts capital, and a lot of it. This has supported strong auction demand and allowed a growing amount of government issuance to be absorbed without a significant increase in borrowing costs. The market appears very liquid and well supported, even as supply expands. This is good news for the Canadian federal government, which is running the largest deficits outside of the 2020 COVID-19 pandemic response.

However, this type of demand brings a completely different set of sensitivities and risks. Because participation is influenced by the relationship between funding costs and bond yields, when that relationship shifts, demand can change with it. Suddenly a government may find half of its buyers gone and then has to choose between cutting back spending or printing money. The problem is that adjustments would not remain confined to just the government. Mortgage rates, corporate financing and other borrowing costs tend to move from that same base, also taking liquidity away from the economy and market.

The same dynamic is widely believed to exist in the U.S., although the structure is a lot more complex and not as directly observable. This is because the Treasury market is significantly larger and more fragmented, involving a broader mix of participants. Much of the activity takes place through repo markets, derivatives and other channels that are not as tied directly to public issuance data.

Interestingly, when looking at the relationship to broader equity markets, there is a pattern where equities tend to correct when these spreads narrow and strengthen when they widen. It suggests that keeping a close eye on these spreads may offer a useful way to gauge underlying liquidity conditions and, by extension, the general direction of markets.

In the end, the concern is not simply who is buying government debt but why they are buying it. We do worry that a growing share of sovereign issuance now depends on a large set of investors responding to pricing relationships rather than long-term ownership or fundamental conviction.

While equity markets tend to capture the headlines, it is often the bond market that sets the tone for everything else. When it is functioning smoothly, liquidity moves freely and risk assets generally find support. As funding conditions begin to evolve, those changes tend to work their way through the system rather than remain contained in one corner.

Therefore, it is an area that warrants closer attention. Looking past the surface, asking a few additional questions and staying attuned to how capital is actually sourced and priced can offer a different vantage point on both risk and opportunity. That’s a spread worth spending some time on.

Dialing back risk amid market strength

Markets have had a remarkable run. Over the past 12 months, it’s been one of the strongest periods we’ve seen for client portfolios. At times like this, the question becomes less about chasing returns and more about managing what we’ve already earned.

There is always a temptation to press harder when markets are working. We take a different approach. After strong performance, discipline matters more than ambition. Importantly, we have already exceeded what we would typically expect to achieve in a full year as our TWC Risk-Managed Balanced Growth fund is up 11.5 per cent so far this year, with a one-year gain of 26.8 per cent and three- and five-year annualized returns of 15.1 per cent and 9.9 per cent, respectively (net of fees as of May 31).

![]()

With that in mind, we have been selectively trimming some of our better-performing positions and gradually building cash, currently around 10 per cent, with the flexibility to move closer to 15 per cent if markets continue to rally.

Cash is often viewed as a drag on performance—and over the long term, it is. But in environments where risks may not fully reflect in asset prices, it serves a different role. It provides optionality. It acts as a form of insurance. And when markets inevitably correct—as they did earlier this year—it gives us the ability to act rather than react.

Our focus remains consistent: protect capital first and provide peace of mind to our investors. We’re not trying to predict market turning points. That’s a difficult, and often futile, exercise. Instead, we position portfolios so that we can navigate a range of outcomes and respond when opportunities arise. From an asset allocation standpoint, we’ve now raised cash to near 10 per cent, taken equities down to 25 per cent, maintaining a 10 per cent% weighting to commodities and alternative strategies, with the remainder being in structured notes.

In particular, the market rally this year has meant that a meaningful portion of our structured notes have been called away earlier than expected. Rather than simply replacing them with similar structures, we have taken the opportunity to reposition more defensively within this part of the portfolio. We are redeploying capital into notes that offer more attractive downside protection, including wider barriers that can better absorb potential market volatility. At the same time, we are prioritizing structures that generate consistent income, either through contingent monthly coupons or opportunistic yearly autocalls, so the portfolio continues to work even in a flatter or more uncertain market.

Equally important is the underlying exposure. We are focusing on more diversified and higher quality indices, reducing single name risk and emphasizing broader, more resilient segments of the market. This allows us to maintain participation if markets continue to grind higher, while being better positioned should conditions deteriorate. It is a subtle shift, but an important one. In periods of strength, the goal is not just to reinvest, it is to upgrade the quality of protection, improve income consistency, and ensure the portfolio is positioned for a wider range of outcomes.

In global equity markets we have been looking for opportunities, adding to some positions as per below.

Agnico Eagle Mines (AEM): We began building a position last year and have been adding more recently. The stock is down meaningfully from its highs, yet the underlying business remains strong, with high-quality assets and a very solid balance sheet. It’s a leveraged way to own gold, which we continue to favour as a hedge against currency debasement in a world of persistent U.S. deficit spending. WSP Global (WSP): We initiated this position last summer and have been adding on weakness. The stock has been hit alongside peers on concerns that artificial intelligence (AI) could disrupt parts of the engineering consulting model. Our view is different. We believe AI will enhance productivity across procurement, design, and project execution, ultimately supporting margin expansion. With a ~US$16 billion backlog and continued infrastructure spending tailwinds, the fundamentals remain intact. Nutrien (NTR): We started building this position in early May. The market is currently signalling weaker fertilizer demand due to higher input costs, and the stock has pulled back accordingly. In our view, a lot of this risk is already reflected in the price. Nutrien remains the world’s largest crop input player, with a low-cost potash franchise and strong free cash flow generation. Longer term, demand is supported by the need to maintain crop yields in a world with constrained arable land.

Discipline isn’t just about buying—it’s also about knowing when to step back and take some profits.

Alphabet (GOOGL): We trimmed roughly half of our position earlier this year after capturing close to a 75 per cent gain. We originally built the position when the market questioned Google’s standing in the AI race, which we believed was overly pessimistic. As the stock re-rated, valuation became more of a consideration. We still like the business. However, recent developments including the departure of key AI leaders from DeepMind and Gemini to competitors highlight that competitive dynamics in this space remain fluid. More broadly, we used the proceeds to reallocate into Microsoft (MSFT), where we currently see a more attractive risk-reward profile.

Sandboxes and motorcycles – by Martin Pelletier

When it comes to managing wealth over many years, I have come to realize that its true value extends well beyond money. Building a nest egg to support a desired lifestyle in retirement is a common and worthwhile goal but the problem is that the habits we rely on to get there often end up standing in the way of finally enjoying it.

A friend of mine, one of the coolest institutional investment professionals I have ever known, sent me a note after unexpectedly retiring. I had asked him why he pulled the rip cord so abruptly.

“Sorry I jumped without saying goodbye. At this stage of my life, time is worth more than money. There are three phases of retirement: Go Go, Go Slow and No Go. I didn’t want to cut into the first phase anymore. I’ve been busy. Gaspé snowmobiling, cat skiing in Kazakhstan, an 8,000-kilometre motorcycle ride from London to The Gambia through the Sahara Desert, hitchhiking to Guinea Bissau then Cape Verde, Belfast. I’m leaving this morning to ride offroad from Mexico to Utah. Next year I plan to cycle from Beijing to Istanbul.”

There is something honest and raw in that decision. My friend recognized that delaying any longer meant trading away his most valuable years of freedom and he actually took a risk and did something about it.

The challenge for most people is that we get comfortable, and comfort is often the enemy of progress. This does not mean you need to cross deserts on a motorcycle, but it does raise reasonable questions: Why not push yourself to actually enjoy the fruits of your labour? Why not start allocating your time differently once you have built the financial foundation to do so? Waiting until “Go Slow” almost guarantees you will run into “No Go” sooner than expected. There will always be reasons to maintain the status quo, but that usually comes at the cost of deferring what matters most.

For younger people earlier in their careers, this perspective can feel completely out of reach, especially given the rising cost of living and worsening affordability crisis. Yet the idea is not to abandon discipline but to rethink how you measure return on your time and your money.

I recently encouraged a younger colleague in the investment business to share his own experience. Instead of chasing expensive vacations, he had been more intentional and directed with how he spends his time. He posted this on LinkedIn:

At its core, your time is your real wealth, and the returns you experience in life come from how you choose to allocate it. Every day we are deploying our time across work, family, health and experiences. Some of those decisions compound in ways no market return ever could. And so, what are you going to do about it?

I choose sandboxes and motorcycles because there are no happy endings.

Research, in-the-media, reads of the month

Valuations flashing some warning signs: Tech Stocks are now outperforming the S&P 500 by the largest margin in 30 years. See Here Big Tech share buybacks are collapsing as AI spending eats the cash. See Here Since January, the entire S&P 500’s gains have come from just two corners of the market, AI and energy, while everything else is actually trading at less than where it started – per Apollo See Here Over 51 per cent of the index’s total market value is in companies trading >10× sales See Here The indicator in this chart is based on a wide array of valuation measures, including the price/earnings (P/E) ratio, the price to book ratio, EV/EBITDA, and return on equity, and others. It just exceeded the previous high it made in January. Excellent interview here with Edward Dawd (Founder Phinance Technologies and author of Cause Unknown: The Epidemic of Sudden Death in 2021 & 2022) See Here History may not always repeat itself but sometimes it sure rhymes. This is a must watch from one of the greats – Chanos. Watch Here Former Treasury Secretary Hank Paulson warns the biggest economic risk from the Iran war may come from global shocks spilling into US markets Watch Here

Inverted vol skew is spiking hard especially in tech stocks: Traders are now “paying up” for upside protection as FOMO has taken over. As a risk manager, I really don’t like it when the “fear premium” gets nuked with calls getting way more expensive than puts. See Here

Equity issuance is exploding and why that matters: Equity issuance is exploding, ending the era of stock scarcity as IPO fever hits. So far 160 companies have announced IPOs with plans to raise over $120 billion, exceeding the combined total from previous two years, which should add $1.5T of stock to the U.S. equity market. See Here We are living through one of the two largest investment booms in the entire history of the U.S. Bigger than the internet. Bigger than the railroads. Bigger than Apollo. Only the Louisiana Purchase was larger. See Here This ties in perfectly to this great piece here Patrick Boyle on how the age of financial engineering may have come to an end. See Here

The U.S. dollar recking ball: Oil prices are no longer the dominant factor driving U.S. Treasury yields, with the correlation between the two breaking down. U.S. two-year yields have reached the highest levels since February 2025, even while crude continues to decline. See Here Japanese approaching its weakest level against the U.S. dollar in almost 40 years See Here U.S. 10-year yields versus Gold (inverted) See Here Monetary policy is tightening again (unweighted average of central banks) according to Bloomberg. See Here Gold reserves hit $5 trillion, overtaking U.S. Treasuries as the world’s top reserve asset See Here If you denominate U.S. GDP in gold instead of dollars, the chart is wild. See Here

Is Canada still a place where you can realistically build wealth, or are we watching a shift that most people haven’t fully felt yet?: Senior portfolio manager with Wellington-Altus, Martin Pelletier breaks down what’s happening beneath the surface of Canada’s economy, from housing becoming increasingly out of reach in major cities, to inflation reshaping the value of money, and why the gap between asset owners and wage earners keeps growing. We also get into what the bond market is signalling about debt and government spending, and why some Canadians, especially entrepreneurs, are starting to look elsewhere for opportunity. Watch Here

Big banks and big brother: TD tells some employees it will use software to monitor their work in an effort to increase productivity Read Here

A frontier without an ecosystem is not stable: In AI era, the firms that come out ahead will be those successfully able to build what Nadella calls a sovereign compounding cognitive learning loop. This is where human capital (judgment, ingenuity, relationships) and token capital (proprietary AI) mutually reinforce each other. If done right, it becomes the firm’s true, defensible IP: a unique hill-climbing machine that grows stronger with use. And it will be human agency that drives it all. Read Here

On the Positive

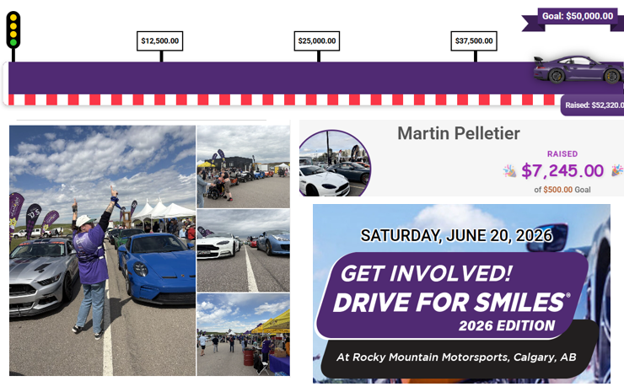

By Martin Pelletier: Starlight Children’s Foundation Canada, through its Drive for Smiles program, gives seriously ill children a once-in-a-lifetime experience— track tours in cars like Porsches, Ferraris, Aston Martins, Lamborghinis, and McLarens. More importantly, it creates moments of joy and lasting memories for children and families who truly need them. Given my love for cars and my passion for supporting young people, getting involved with this charity felt like a natural fit. I met some truly incredible people that Saturday—young and old. Many of the kids are facing serious illnesses, yet they carry a perspective on life that most of us spend decades trying to learn.

One young man—18 years old—has had much of his digestive system removed. He relies on intravenous feeding every day and lives with constant medical support. When I asked how he manages, he simply said it’s okay—he grew up this way and doesn’t know anything different. That kind of perspective stays with you. What also stood out was the impact on families. Events like this give caregivers and especially siblings, who are often overlooked in families dealing with serious illness, a chance to simply be kids for a day. I met one family where the grandparents had moved in to help their daughter care for her child. It’s a reminder that behind every sick child is an entire support system quietly carrying the load.

Thanks to the generosity of so many supporters, the event raised over $50,000 for local kids. I’m deeply grateful to everyone who contributed and made the day possible.

Building with purpose: Profit is important, but purpose is everything. Success comes from having the biggest impact instead of the biggest margins. This is exactly what playing the long-game means. Relationships over transactions. Watch Here

Nothing captures the shallow decay of our time better than this: Social media trends have turned the world’s most beautiful places into endless bathroom lines at a concert, where everyone waits for hours just to take the same photo to show to people who couldn’t care less. Watch Here

I wanted to share my nighttime grateful routine in case it may help you as much as it helps me: I bet you didn’t know: In the U.S., men account for ~70 to 80 per cent of suicide deaths (nearly 4x the rate of women). Globally, men die by suicide 2–4x more often. Yet only ~17% of men received mental health treatment last year vs ~29% of women. Men, if you’re struggling with depression or feeling hopeless, you’re not alone, and it’s not weakness to ask for help. Reach out. Stay. You matter. Watch Here

To find out more about the TriVest team and how we manage wealth, follow us on Twitter, or LinkedIn. Please email us if you want to find out more about our services.

Trivest Wealth is a trade name of Wellington-Altus Private Counsel Inc. (WAPC). WAPC is a Portfolio Manager and Investment Fund Manager registered with the Manitoba Securities Commission as its primary regulator. The advisors associated with Trivest Wealth are registered with WAPC. WAPC is a subsidiary of Wellington-Altus Financial Inc. The information contained herein has been provided for information purposes only. The information has been drawn from sources believed to be reliable. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document.

Transactions of the type described herein may involve a high degree of risk, and the value of such instruments may be highly volatile. Such risks may include without limitation risk of adverse or unanticipated market developments, risk of issuer default and risk of illiquidity. In certain transactions counterparties may lose their entire investment or incur an unlimited loss. This brief statement does not disclose all the risks and other significant aspects in connection with transactions of the type described herein, and counterparties should ensure that they fully understand the terms of the transaction, including the relevant risk factors and any legal, tax, regulatory and accounting considerations applicable to them, prior to transacting. This report may contain links to third-party websites. WAPC is not responsible for the content of any third-party website or any linked content contained in a third-party website. The inclusion of a link in this report does not imply any endorsement by or any affiliation with WAPC.

Structured Notes are not suitable for all investors. The notes do not pay dividends, and any dividends paid on the underlying constituent’s may not factor into the return calculation that determines your return. The protection and potential augmented returns on these notes are only available when

Wellington-Altus Private Counsel Inc. (WAPC) does not guarantee the accuracy or completeness of the information contained herein, nor does WAPC assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact your financial advisor.

Wellington-Altus Private Counsel is registered as a Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland & Labrador, Nova Scotia, Northwest Territories, Nunavut, Ontario, PEI, Quebec, Saskatchewan, Yukon and an Investment Fund Manager in Alberta, Manitoba, Ontario, and Quebec.

All trademarks are the property of their respective owners.

© 2026, Wellington-Altus Private Counsel Inc. ALL RIGHTS RESERVED.

NO USE OR REPRODUCTION WITHOUT PERMISSION.

www.wellington-altus.ca