INSIDE

Dispersion Is Back and It’s Changing Everything

Despite a strong earnings season—nearly three‑quarters of S&P 500 companies beating expectations and delivering double‑digit profit growth markets are increasingly focused on what lies ahead rather than what has already occurred. Global economic and geopolitical uncertainty remains near multi‑decade highs, driven by persistent flashpoints involving Iran, China, Russia and Venezuela, rising energy‑supply risks at a time when governments are heavily indebted, and growing constraints on policymakers’ ability to respond without destabilizing sovereign balance sheets. This backdrop is accelerating a rotation away from long‑duration assets, exposing vulnerabilities in software, SaaS, and private‑credit markets as artificial intelligence disrupts legacy business models and raises liquidity concerns. At the same time, stock dispersion has returned forcefully, with outcomes increasingly determined at the individual company level rather than by index exposure, while commodities—particularly critical minerals, precious metals and select energy assets—appear to be entering the early stages of a new cycle. In this environment, investors are rewarding certainty, balance‑sheet strength and visible cash flow, while punishing ambiguity, leverage and deferred payoffs. The result is a market that may appear calm on the surface, but is increasingly fragmented and volatile underneath one where disciplined portfolio construction, active security selection and thoughtful risk management matter more than they have in years.

Sovereign Debt in a World of Energy Uncertainty

The next few weeks may prove more consequential than markets currently assume, as a visible but constrained standoff between Iran and the United States raises the risk of sustained energy disruption through the Strait of Hormuz. While Iran’s leverage is imperfect and costly to itself, impairment of the Strait would likely keep upward pressure on oil prices, with the greater risk being a shift in the forward curve that would signal markets are no longer treating the situation as temporary. In a world already marked by trade fragmentation, supply chain stress, and declining cooperation, such a shift would unevenly impact countries depending on their energy security, fiscal capacity, and balance sheet strength, leaving regions like Europe particularly exposed and offering a cautionary lesson for others, including Canada. The most significant vulnerability lies in sovereign debt markets, which appear to be pricing a benign outcome and underestimating how sustained energy pressure could weaken growth, fuel inflation, and widen deficits. If those assumptions prove wrong, governments may be pushed toward reserve sales or monetary accommodation, further eroding purchasing power and financial stability. The core lesson is not that these outcomes are inevitable, but that when risks become asymmetric, the cost of being unprepared rises sharply.

CUSMA Complacency and the Cost of Ignored Risk

A recent poll showing that most Canadians believe the loss of CUSMA would have little or no economic impact highlights a dangerous disconnect between public perception and market reality. Canada’s economy is structurally dependent on the United States, with roughly three‑quarters of goods exports flowing south and 85–90% currently entering duty‑free under CUSMA. The agreement faces a formal review this June, and the U.S. can unilaterally withdraw or downgrade it, exposing Canada to WTO tariffs and powerful U.S. trade‑remedy tools that would disrupt just‑in‑time supply chains. Private‑sector modelling suggests such a shock could leave real GDP 1–2 per cent lower over time—an uncomfortable outcome given Canada’s already weak growth, widening GDP‑per‑capita gap versus the U.S., and persistent affordability pressures. For investors, this creates a discrete but underpriced policy risk, particularly for long‑term Canadian government bonds, which are vulnerable to a mix of trade uncertainty, fiscal slippage, and duration risk. While diversification is sensible, it cannot replace CUSMA’s role in Canada’s growth model, and prudence today argues for defensive positioning rather than complacency—because unacknowledged risk does not disappear; it merely waits.

The “Four-Burner Theory” of Building Wealth

A recent trip to the desert prompted a deeper reflection on how time and money ultimately reflect what we value most, leading to the “four‑burner” framework (Family, Work, Health and Friends) which reminds us that we cannot give full energy to everything at once without consequence. Work, in particular, is seductive and rarely punishes overinvestment, yet it often crowds out family, erodes health through small, seemingly harmless compromises, and quietly distances us from meaningful friendships. These trade‑offs are rarely dramatic but unfold gradually, often going unnoticed until the cost is already high. The lesson is not to extinguish any burner permanently, but to consciously rotate focus based on life stage, protecting what matters most in the present without starving what we will need in the future. This mindset extends naturally to financial planning, where wealth should serve as a tool to support life priorities, not override them. Thoughtful investing is therefore not just about maximizing returns, but about deliberately aligning capital with values—so that time, health, relationships, and purpose are preserved rather than sacrificed by accident.

Please reach out to any of our team members should you have any comments or questions about markets, your portfolio or just wanting to catch up.

February/March 2026: Dispersion Is Back and It’s Changing Everything

By traditional measures, this has been a strong reporting season. Nearly three‑quarters of S&P 500 companies have exceeded earnings per share (EPS) expectations and are delivering an impressive 13.2 per cent growth rate, marking the fifth consecutive quarter of double‑digit earnings growth, according to FactSet data as at the last week of February. Markets have also been relatively forgiving, with negative EPS surprises punished by roughly two per cent share losses, which is below the five‑year average decline of 2.8 per cent.

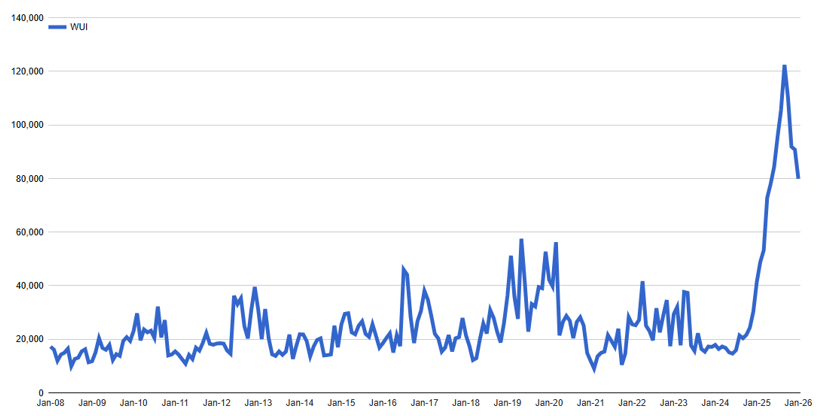

But headline numbers only tell part of the story. Despite these robust results, the global uncertainty backdrop remains extreme. The Global Economic Policy Uncertainty Index—built from newspaper-based measures across major economies—recently surged to levels near the highs seen during the most stressed periods in the series, and remains materially elevated versus long‑run norms. This matters because markets tend to tolerate ambiguity—right up until they don’t. When uncertainty reaches these extremes, backward‑looking beats and misses matter far less than the forward path and share prices can reprice abruptly.

Our broader view is that this is the most complex macro setup we’ve seen in years: geopolitical flashpoints remain unusually elevated (Iran, Venezuela, China and Russia), and the oil market sits uncomfortably close to a regime shift where supply disruption risk is rising at the same time policymakers are trying to cut rates.

Layer on top of that the reality that many sovereigns are already over‑levered, leaving less room for policy error. To illustrate the pressure: the UK’s own fiscal watchdog estimates income tax will raise about £329 billion in 2025–26, while major social outlays are enormous—welfare and state pensions alone total roughly £293 billion under current-year allocations—before even considering healthcare or debt interest.

At the same time, stock dispersion is back in force, meaning index-level returns are increasingly masking sharp performance gaps underneath. And that dispersion is being amplified by a notable sell‑off in software/SaaS and the private credit ecosystem that helped finance large swaths of the sector—raising fresh questions about liquidity, refinancing windows, and whether legacy cash flows remain as “durable” as investors assumed in the low‑rate era. Put simply, this is a market rotating away from long-duration assumptions, and the leadership baton is being passed more often than most investors are used to.

As a result, this earnings season has been less about beats and misses and more about the durability of earnings and how clearly management teams can see the road ahead. That shift helps explain why several stocks have sharply sold off, in some cases losing close to double digits in a single session. The list cuts across sectors: Charles Schwab Corp., CBRE Group Inc., Raymond James Financial Inc., PayPal Holdings Inc., Robinhood Markets Inc., Salesforce Inc., Netflix Inc., Shopify Inc., Allied Properties REIT, H&R REIT and First Quantum Minerals Ltd., among others. Despite their differences, these companies generally shared one or more common traits. Some offered guidance that was vague, cautious or difficult to model. Others faced visible margin pressure, whether from higher costs, competitive intensity or slowing end markets. A third group leaned heavily on a familiar refrain: trust us, the payoff comes later. That message isn’t landing well in this environment.

By contrast, a smaller group of companies has been rewarded and in some cases quite decisively. Names such as Meta Platforms Inc., Nvidia Corp., Broadcom Inc., Intact Financial Corp. and Toromont Industries Ltd. delivered what investors are actively seeking: immediate monetization, visible cash flow and a clear, credible link between capital investment and returns. The market has shown a willingness to pay up for certainty when that is paired with balance‑sheet strength. The takeaway is straightforward: in an uncertain world, people crave certainty and hit the sell button when they don’t get it.

That has important implications for portfolio construction. Diversification matters most precisely when uncertainty is high, and recent market action reinforces that point. Correlations are breaking down, dispersion is rising and outcomes are increasingly determined at the individual stock level. This environment is also creating opportunities for those brave enough to navigate the uncertainty because value is being instantly created and destroyed one company at a time. Some sell‑offs are justified; others are clearly overdone. That dispersion is precisely where disciplined investors can add value if they get it right.

This is where the role of a skilled portfolio manager becomes critical. Relationship management alone isn’t enough. Investors need professionals who can genuinely interpret company fundamentals, balance sheets, cash flows and capital allocation and then pair that bottom‑up work with a strong grasp of the macro backdrop. That includes understanding the long‑term consequences of excessive fiscal and monetary stimulus when it comes to currency debasement and the erosion of real returns. Layer on top of that the accelerating disruption from artificial intelligence—where markets are rapidly repricing winners and losers—and you have a market that may look calm on the surface, but is increasingly chaotic underneath.

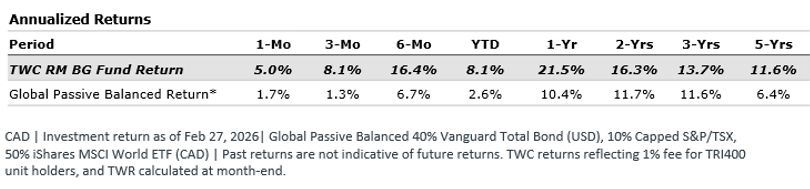

Against that backdrop, we have positioned client portfolios with large asset allocation changes that have yielded one of the best 12‑months and starts to a new year that we’ve ever had. Our TWC Risk‑Managed Balanced Growth fund gained approximately 5 per cent in February, bringing our year‑to‑date return to 8.1 per cent and boosting our 12‑month return to 21.5 per cent—both of which are well ahead of our global passive balanced benchmark portfolio that posted only 2.6 per cent over the past two months and 10.4 per cent over the past 12 months to the end of February.

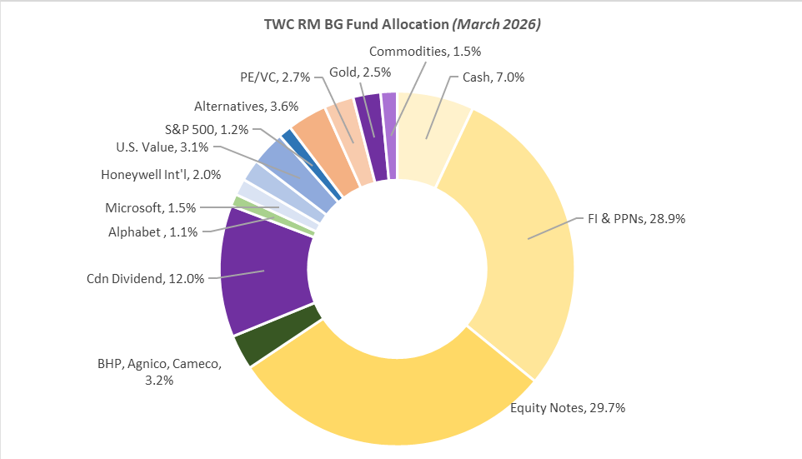

That said, we would like to highlight three main trades that have not only assisted us but also leave us well positioned for the current market environment.

First, we don’t own traditional government bonds. Instead, we’ve looked for functional replacements—including structured notes—that can provide higher levels of income and more defined outcomes without relying solely on duration exposure. This is imperative in an environment that increasingly resembles material currency debasement, where investors often bleed purchasing power in real terms, particularly in fixed income. Consider this: approximately one‑third of all U.S. dollars in circulation were created in the three years following the pandemic, and Canada experienced a similarly dramatic expansion, with roughly 30 per cent of its broad money supply issued over the same period.

Second, we own commodities, but primarily through the highest‑quality producers operating in low‑risk jurisdictions. For example, we own copper through BHP Group Ltd., gold through Agnico Eagle Mines Ltd. and uranium through Cameco Corp. We’re watching oil closely and if we re‑enter the space, it will be selective as well. What these companies share is disciplined capital allocation, strong balance sheets and long reserve lives—exactly the traits the market is rewarding.

Third, we’re highly tactical, taking a laser‑focused approach rather than a broad‑brushed one. For example, we locked in significant gains in Alphabet Inc., sold roughly half the position, and redeployed capital into Microsoft Corp. following its roughly 20 per cent sell‑off. We also initiated a position in Honeywell International Inc., where a restructuring is underway and we believe the market is only beginning to recognize the value that can be unlocked.

We were buyers of Telus Corp. during tax‑loss selling in December. While its recent quarter was mixed, it is implementing meaningful change, including a new CEO and the sale of its health‑care division, which we believe improves the forward outlook while continuing to support an attractive dividend.

We’ve also been adding to WSP Global Inc., a world‑class infrastructure company that sold off about 10 per cent in one day after the market briefly priced in artificial intelligence disruption risk originating from a Florida‑based penny stock best known for its early days making karaoke machines.

In this market, certainty isn’t cheap but it’s becoming increasingly valuable for those willing to do the work.

A World of Energy Uncertainty

The next few weeks may prove more important than markets currently assume, and not only for energy. What appears to be developing is a standoff between Iran and the United States that is visible to all but constrained by limited options on both sides.

Iran’s remaining point of leverage is the Strait of Hormuz. While this is an imperfect tool, given that most OPEC production depends on the same route, it would be a mistake to dismiss its relevance. The more important question is how much additional change would be required within the Iranian regime to bring it back onside, as it is clearly more than what was attempted in Venezuela.

If the Strait remains impaired, upward pressure on spot prices is likely to persist. Global oil demand has a substantial non-discretionary component, and higher prices alone do not eliminate demand in the short term. The more consequential risk lies not in the spot market, but in whether this pressure begins to influence the forward curve.

A shift in forward pricing would signal that markets are no longer treating the situation as temporary. That transition would materially change expectations and behaviour, with uneven effects across regions, industries, and balance sheets.

The problem with significantly higher oil prices is that they are emerging at a moment when governments globally are already running large fiscal deficits and carrying unprecedented levels of debt. Policymakers may want lower interest rates, but sustained energy inflation makes that difficult, as bond markets push yields higher. This is occurring at the same time unemployment is rising and the affordability crisis is worsening, with escalation involving Iran carrying the potential to tip already fragile economies into recession.

This environment tends to separate those who are prepared from those who are not. In a world shaped by trade fragmentation, supply chain reconfiguration, and declining cooperation, countries increasingly act in their own interest regardless of stated intentions. Those without reliable access to energy and critical inputs, or the financial flexibility to absorb higher costs, are more vulnerable.

Europe, particularly countries with limited domestic energy and constrained fiscal capacity, appears more exposed. This is a reality other developed economies, including Canada, would do well to consider carefully.

The area of greatest concern, in our view, is sovereign debt. Bond markets appear to be assigning a low probability to adverse outcomes. Yields do not reflect the risk that sustained energy pressure poses to growth, inflation, and fiscal stability, implicitly assuming that energy prices will normalize quickly.

Should that assumption prove incorrect, deficits are likely to widen as revenues weaken and expenditures rise. Political constraints make meaningful fiscal retrenchment unlikely, increasing the probability that governments will rely on reserve sales or central bank accommodation.

If demand for sovereign debt weakens under these conditions, the policy response is familiar. Monetary expansion becomes the path of least resistance. Over time, this erodes purchasing power, undermines affordability, and increases economic and social strain. This would not represent a new regime so much as a continuation of trends accelerated earlier this decade.

In the near term, gold is often sold to fund dislocation, leaving few traditional safe havens. Oil has become the default hedge, but it is a precarious one. Should tensions ease after a prolonged period of much higher prices, oil could fall sharply in response to the economic damage caused by higher inflation and tighter financial conditions.

This is exactly why the situation needs to be resolved swiftly rather than drawn out. Those calling casually for significantly higher oil prices should be careful what they wish for. The second order effects tend to arrive faster, and with greater force, than most expect.

For more of our thoughts in Martin’s recent radio interview with Greg Brady:

CUSMA Complacency and the Cost of Ignored Risk

We recently came across a rather shocking new poll suggesting that fewer than half of Canadians believe the end of CUSMA would be bad for the country. Only 45 per cent say it would hurt Canada, while a majority believe it would make no difference or might even be beneficial.

As a portfolio manager I do not have the luxury of taking such a head-in-the-sand approach. This is because markets do not price public opinion; they price outcomes. Consequently, there are material risks whenever large economic risks like this are misunderstood, minimized, or ignored potentially resulting in large losses in areas traditionally viewed as safe.

Under CUSMA’s own rules, the agreement is up for formal review this June, and the United States has the unilateral ability to withdraw entirely with notice or pivot toward a bilateral framework on its own terms. A cancellation or downgrade does not require congressional gridlock or multilateral consensus.

The problem is that Canada’s economic trade is highly geographic with roughly three-quarters of goods exports go to the United States, and roughly 85–90% of these go into the U.S. currently enter duty‑free. Without CUSMA, trade defaults to WTO most‑favoured‑nation tariffs and exposes Canada to U.S. trade‑remedy tools such as Section 232, Section 301, anti‑dumping, and countervailing duties. Even small tariffs matter enormously in high‑volume, low‑margin, just‑in‑time trade, which describes much of Canada–U.S. commerce.

Private‑sector modelling suggests that, in the absence of CUSMA, Canada’s real GDP would likely be 1–2 per cent lower than otherwise over several years, reflecting reduced export competitiveness, weaker investment, and supply‑chain disruption. That may sound manageable but not when Canada’s real GDP performance in Q4 2025 was the worst in the G7 with a loss of 0.2 per cent.

And then consider this: Canada’s GDP per capita was roughly 90 per cent of the U.S. level particularly during the past WWI era (1945 to 1970s). Today it has fallen to about 65–70 per cent, representing the widest sustained gap between the two countries in the post‑World War II era.

Trade disruption would also likely weaken the Canadian dollar and introduce stagflation‑like dynamics. Higher import costs and tariffs would create short‑term inflation pressure, adding to the affordability crisis in this country. For example, Canada still has some of the worst food inflation in the entire developed world, nearly double the rate they have in Japan, the next closest G7 country.

From an investor’s perspective, this introduces a discrete, time‑bound policy risk that is currently being priced as if it does not exist.

Canadian long‑term bondholders are exposed to a dangerous mix of policy drift, fiscal slippage, trade vulnerability, and duration risk, all while being inadequately compensated for bearing those risks. The issue is not whether Canada would “collapse” without CUSMA, but whether its economic trajectory would quietly and persistently continue to deteriorate. Long‑term bonds are promises about the future, and right now that future is being priced far too optimistically.

For those wondering what the impact would potentially simply take a look to the UK, New Zealand and Australia, all countries Prime Minister Carney appears to be emulating economic policy frameworks from including aggressive energy transition goals layered onto mature, heavily regulated economies.

Canada’s 10‑year yield currently sits near 3.25 per cent, while the UK, Australia, and New Zealand trade roughly 100 basis points higher. If Canadian yields were to migrate even partway toward that peer group, long‑term Canadian bondholders could face mark‑to‑market losses in the range of 9–10 per cent, without any recession or credit event. This is pure duration risk, magnified by policy uncertainty.

The bottom line is that trade diversification is sensible, but it is not a substitute for CUSMA. Geography, infrastructure, and supply chains make the United States structurally irreplaceable for Canada. Even optimistic diversification strategies take decades, not years. In the meantime, investors must price the risk that Canada’s growth model becomes less efficient rather than more resilient under our current leadership.

For fixed‑income investors, caution argues for defence over complacency. That can mean selectively replacing Canadian long bonds with foreign sovereign exposure, or, in our case, eliminating Canadian government bonds entirely in favour of structured notes with substantial downside buffers. We also view gold as a useful partial hedge against sovereign and policy risk especially striking given Canada’s status as the only OECD country with no official gold reserves.

Unacknowledged risk doesn’t vanish; it waits often with serious consequences for those who choose to never see it coming.

The ‘Four-burner Theory’ of Building Wealth –

by Martin Pelletier

I recently took a trip to the desert. The desert has meaning. It has deep roots. It strips away excess and leaves only what is essential. There is no distraction and no ornamentation, just heat, distance and time, and enough open space to finally hear what actually matters.

While I was participating in a meditative sound bath, I was able to reflect on the idea that how I spend my time and money is a representation of what I value in life. This brought me to the four-burner theory, often attributed to American humorist David Sedaris.

Imagine your life as a stovetop with four burners, one for Family, Work, Health and Friends, respectively. Each one demands attention and requires your time as fuel. The uncomfortable truth is that you do not have enough gas to run all four on full at the same time and so you have to choose. To be successful at what you choose you usually have to turn one burner down or completely off, and to be really successful you may have to turn off two.

Work is the hardest burner to turn down, particularly in a culture that celebrates hustle and busyness as a proxy for success. Work provides identity, status and momentum, and at times it even offers escape from everyday life. It tells you who you are when you are not entirely sure yourself, giving structure and validation in a world that rarely pauses long enough to ask deeper questions. But work can be very greedy by nature, and when it is given too much flame the other burners do not simply dim, they slowly starve.

Careers rarely punish overinvestment, at least not at first. They reward it with promotions, recognition and opportunity, right up until the moment you look around and realize that in climbing higher and higher, you have quietly traded breadth for altitude, flying you very close to the sun at great cost.

Family represents connection through marriage, kids, parents and presence. Yet it is the burner most often sacrificed by high achievers, not because it lacks value but because it feels permanent, as though it will always be there waiting. It seems safe to borrow from and safe to delay. And so it fades quietly, not in a single dramatic moment but gradually, slipping behind inboxes, travel schedules and conference calls.

Health rarely announces itself in dramatic terms, with small compromises that feel harmless in the moment, in nights of shortened sleep, daily exercise skipped or delayed, quick meals over healthy ones for convenience and that regular alcoholic drink meant to help you unwind after a long day. You tell yourself it is temporary, that you will deal with it later, that you will reset and recover when everything returns to normal. And then, often without warning, the body revolts, not out of spite but out of necessity, and by the time it finally has your full attention the bill is already due.

Friends are often the quietest casualty of all, not lost in a single decision but slowly eroded by time, distance and competing priorities. You grow and change, pulled forward by career, family and responsibility, while others remain rooted where they are, and without any ill intent on either side the space between you widens. Life fills up, calendars crowd and one day you realize you are surrounded by contacts rather than connection, rich in likes but short on the kind of relationships you reach for when things begin to fall apart.

The choice of which burners to turn up and which to turn down often depends on the stage of life you are in. You cannot beat the burners but you can rotate them. There are periods when work deserves the flame, when family must come first, when health becomes non‑negotiable and when friendship is what keeps you whole. Life is not static and your burners should not be either. The goal is not to run out of fuel by trying to keep all four burning at once, but to decide which one matters most right now and protect it accordingly.

This way of thinking matters when it comes to money as well. Work is not your identity but a tool to build wealth, support you and your family, and eventually buy back time and freedom so you can spend more of it with the people you care about. At its best, work can also be a form of purpose, a way to contribute and make the world better not just for yourself, but for your family, your friends and others you may never meet.

A neglected lifestyle cuts that time short, often before you fully appreciate how valuable it was. These trade‑offs should not be accidental. They need to be acknowledged and deliberately integrated into a financial plan that protects what matters most at each stage of life. Savings, planning and portfolio design are not simply about maximizing returns but about aligning your capital with your priorities, ensuring the burners burning brightest today are supported, and that the ones you will need tomorrow are not left cold.

So as part of your next investment review be sure to take the time to reflect on how you are investing not just in your portfolio but also how you are spending your time, money and energy, and rebalance if needed.

Research, Reads of the Month

An outside-the-box review of Trump and the Middle East

He wants to bring back the manufacturing of electronic chips and semiconductors to the United States instead of producing them in Asia. He wants to sell American agricultural products to India, but the Indians completely rejected that. He wants Asian companies to sign long-term liquefied natural gas contracts with American companies and buy more American liquefied natural gas. He wants Asian countries to buy more American oil. Read Here

This isn’t the 1970’s

Oil raises headline inflation, raises core inflation through transport, food, and manufacturing AND suppresses growth at the same time. That puts central banks in a trap: Cut rates → and inflation accelerates OR Hold or raise rates → and debt sustainability deteriorates. In the 1970s, policymakers could choose inflation over austerity without risking solvency. Today, they can’t. See Here

Oil Price versus Global GDP growth.

Rystad Energy believes that interest rates are more important than the price of oil when it comes to GDP. That is also why being long bonds is like being short oil. See Here Bond buyers are short oil going into one of the largest geopolitical events in the middle east in decades. See Here

Why Europe is terrified of standing up to Iran

America’s war on Iran has revealed much about its allies. Israel is as steadfast as ever, as secretary of war Pete Hegseth. Australia and Canada have also made clear their unequivocal support for the military action. In Europe, however, the response has been lacklustre. Hegseth regretted the faintheartedness of ‘traditional partners who wring their hands and clutch their pearls, humming and hawing about the use of force.’ Read Here

Investors poured billions into private credit. Now many want their money back

The rush for the exits in private credit is prompting fresh scrutiny of the sector’s less-liquid structures and its rapid expansion into the retail wealth space. Blackstone has become the latest fund manager to be hit by a surge in requests from investors to withdraw from its flagship private credit strategy. Read Here Private equity returned fewer profits to investors for a fourth straight year as the industry sat on $3.8 trillion of unsold assets and struggled to raise money for new funds. See Here

Weaponization of currency, the final phase.

Governments around the world got a taste of control during the COVID lockdowns, don’t want to go back, but in fact take it even further. Both sides of the spectrum right and left. And we as citizens are so blindsided by our anger for those on the other side of our political beliefs that we miss it completely. Watch Here

Copper stocks are going to go crazy in the coming years.

Good copper juniors are going to 10X easily. S&P Global Vice Chairman Daniel Yergin: “We’ll need 50% more copper than we have today.” Watch Here

How are you positioned?

Oh Canada

If Ontario were a country, its marginal tax rate would be the 5th highest of any advanced economy. A Must See Chart

Canadian Natural Delays Oil Sands Project on Government Uncertainty

Canadian Natural Resources is delaying a C$8.25 billion ($6 billion) oil sands mine project due to the “lack of finalization” of government policies on carbon pricing and methane, President Scott Stauth said on an earnings call. See Here

Oil reserves in USA and Canada

B.C. small businesses suffered worst sales decline in Canada

A new report says B.C. small businesses suffered the worst decline in sales in Canada in the last quarter of 2025. As Aaron McArthur reports, one business advocacy organization says the B.C. government isn’t helping matters. Read Here

Number of UK young people not in work or education nears 1 million

Nearly 1 million Britons aged 16-24 were not in employment, education or training at the end of last year, the second-highest level in more than a decade. Read Here

Financial Advisors putting all of your money in index funds

See Here

Stock-Bond diversification offers less protection from market selloffs

Diversification has become harder since 2020 as stocks and bonds tend to move in tandem during sharp selloffs, adding to financial stability concerns. Read Here

On the Positive

A special shout-out to TriVest’s very own Senior Portfolio Manager Steve Rowles who raised over $51,000 for men’s mental health and the Calgary Counselling Center. Well done Steve!!

When Albert Einstein was asked about the speed of sound, he replied: “I do not carry such information in my mind since it is readily available in books… The value of a college education is not the learning of many facts but the training of the mind to think.”

In Michelangelo’s The Creation of Adam, God’s finger stretches fully outward, while Adam’s finger is bent at the last joint. It illustrates that God is always present, but it is up to humans to take the initiative to connect with Him…

Want to change the climate – plant more trees

A major city in Colombia cooled itself by 2°C simply by planting millions of trees and shrubs—demonstrating that nature provides one of the most effective cooling solutions available. Read Here

The damage they are doing in southern Spain will take generations to reverse

Large solar developers are targeting southern Spain because the region has 3,000+ hours of sunshine per year, making it one of Europe’s most attractive places for solar power. That same region is also the heart of Spain’s olive‑oil industry the world’s largest. Some proposed projects could require removing tens of thousands of trees, with one report citing up to 100,000 olive trees threatened across eight planned solar developments. Watch Here

Bird nests are some of the most impressive examples of natural engineering

Using nothing but their beaks and feet, birds create structures that look almost impossible to design-carefully adapted to their climate, surroundings, and predators. Watch Here

Generation X

Psychology says the 1960s and 70s accidentally produced one of the most emotionally durable generations in modern history — not through better parenting but through benign neglect that forced children to self-regulate, problem-solve, and develop emotional calluses. Read Here

Now that’s a bachelor party

Some legends just kidnapped their groom-to-be for the bachelor party, dressed him up as Maduro, and dragged him through the airport like it was totally normal. Watch Here

I didn’t know the jewel I was having

When Jean-Claude Van Damme openly admitted he regrets leaving his wife, the woman who stood by him when he had no fame or money. He chose Hollywood success and his ego over loyalty, but years later she forgave him and welcomed him back. Watch Here

Not your typical AI triumph, it’s a petri dish of actual human brain cells

In a groundbreaking fusion of biology and silicon, scientists at Cortical Labs have taught a cluster of lab-grown human neurons to play the iconic video game Doom. Read Here

Morning or Afternoon?

Ronald Regan, automobiles and plumbers. Watch Here

Gavin Baker – Truth-Seeking and Crossover Investing at Atreides

In Michael Jordan’s second to last year with the Chicago Bulls, Jerry Krause, GM of the Bulls said, “Listen players don’t win championships, organizations do. It isn’t just Jordan or Pippen. It’s how we scout, draft, train, it’s our system.” Well… after Michael Jordan left they never won another championship. Listen Here

This is how you grow a business

If you go back to a restaurant a third time and have another flowless experience, the statistical chance of coming back is 72 per cent, up from under 50 per cent. Watch Here

Thanks for visiting

To find out more about the TriVest team and how we manage wealth, follow us on Twitter, LinkedIn or Facebook . Please email us if you want to find out more about our services.

The information contained herein has been provided for information purposes only. The information has been drawn from sources believed to be reliable. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document.

Transactions of the type described herein may involve a high degree of risk, and the value of such instruments may be highly volatile. Such risks may include without limitation risk of adverse or unanticipated market developments, risk of issuer default and risk of illiquidity. In certain transactions counterparties may lose their entire investment or incur an unlimited loss. This brief statement does not disclose all the risks and other significant aspects in connection with transactions of the type described herein, and counterparties should ensure that they fully understand the terms of the transaction, including the relevant risk factors and any legal, tax, regulatory and accounting considerations applicable to them, prior to transacting. This report may contain links to third-party websites. WAPC is not responsible for the content of any third-party website or any linked content contained in a third-party website. The inclusion of a link in this report does not imply any endorsement by or any affiliation with WAPC.

Structured Notes are not suitable for all investors. The notes do not pay dividends, and any dividends paid on the underlying constituent’s may not factor into the return calculation that determines your return. The protection and potential augmented returns on these notes are only available when held to maturity. These notes do not offer any protection if they are sold before the maturity date. If sold before the maturity date, returns may be positive or negative. These examples are for illustrative purposes only and should not be construed as an estimate or forecast of the performance of the Index or the return that an investor might realize on the Notes.

Wellington-Altus Private Counsel Inc. (WAPC) does not guarantee the accuracy or completeness of the information contained herein, nor does WAPC assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact your financial advisor.

Wellington-Altus Private Counsel is registered as a Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland & Labrador, Nova Scotia, Northwest Territories, Nunavut, Ontario, PEI, Quebec, Saskatchewan, Yukon and an Investment Fund Manager in Alberta, Manitoba, Ontario, and Quebec.

All trademarks are the property of their respective owners.

© 2026, Wellington-Altus Private Counsel Inc. ALL RIGHTS RESERVED.

NO USE OR REPRODUCTION WITHOUT PERMISSION. www.wellington-altus.ca