INSIDE

Markets getting Trumped by tariffs

Markets have been overly volatile over the past few weeks. As portfolio managers, we worry that this uncertainty has the potential to cause real economic damage, even a global recession. Our thesis is that a global trade war will cause a temporary spike in pricing causing consumers to reduce spending and debt levels.

Near-term cautious on oil and gas, but material upside if the right changes are made

We’re waiting to see if there is finally a change in government here in Canada brave enough to finally change course by streamlining regulations instead of purposely adding to them and encouraging the build out of a national oil and gas infrastructure network. Should this be the case, then we expect a material bump in valuations of Canadian oil and gas companies but until then we’re still taking a cautious approach.

Slow and steady always wins the race

We’ve continued to make some allocation changes to add some downside protection and have shored up cash a bit to take advantage if weaker markets persist. Overall, our TWC Risk-Managed Balanced Growth fund is continuing to post some decent results to start 2025 despite some incredibly volatile markets. As at the end of February the fund is up 1.8 per cent this year boosting its 5-year annualised return to 8.3 per cent.

March 2025: How not to get Trumped by tariffs

Welcome to this month’s Market Strategy. In this edition we share our latest views on the market along with how we’re positioned strategically.

Martin recently returned from an exciting trip to Vienna, where he was asked by many locals about the reason for U.S. President Trump’s recent aggressive positioning against its once closest economic allies, Canada and Mexico. This, while appearing to be taking a much softer position against adversarial countries such as Russia. He really didn’t have an answer but one thing is for certain: What we are witnessing is a fundamental shift in geopolitics that could have a profound and lasting impact on the global stage.

As portfolio managers, we worry that this uncertainty has the potential to cause real economic damage, even a global recession. Our thesis is that a global trade war will cause a temporary spike in pricing causing consumers to reduce spending and debt levels.

The U.S. isn’t as protected as it thinks it is, as targeted countries respond with counter-tariffs of their own. Canada responded with counter tariffs totalling 25 per cent on $155 billion of U.S. imports, though tariffs remain in flux as the U.S. hints at some relief measures tinkers with deadlines and relief measures and world leaders plan on negotiating attempt negotiations with Trump. The Chinese Embassy in the U.S. posted on X that, “If war is what the U.S. wants, be it a tariff war, a trade war or any other type of war, we’re ready to fight till the end.”

Meanwhile, all of this is happening at the same time as Elon Musk is undertaking massive government cuts that will have a negative multiplier effect on the economy. According to Apollo Investments, DOGE-related layoffs could potentially be closer to one million when including contractors.

And just earlier this month, the Atlanta Federal Reserve model is predicting that U.S. gross domestic product (GDP) will contract by 2.83 per cent in the first quarter, revised lower from its 1.48 per cent contraction forecasted at the end of February.

We think this has the potential to suck liquidity out of the market, sending the highest-valued, levered beta segments such as U.S. tech companies like Nvidia Corp. and Tesla Inc. even lower than what we’re currently witnessing. The safety of the broader segments of the U.S. market, such as the Russell 2000, will also be affected by this.

Closer to home, about one-third of Canada’s GDP comes from exports with more than 70 per cent of that going to the U.S. So our economy is certainly going to be harmed with tariffs. The issue is that Canadian households are among the most levered in the G7 but hopefully we will see timely rate cuts by the Bank of Canada and ideally some smart policy out of Ottawa, such as the immediate scrapping of the carbon tax, that will help ease some of the pain.

That said, the S&P TSX Composite could be affected, as it is dominated by Canadian financials and energy sectors, both of which are exposed to the broader economy. That said, we have to admit some stocks within these segments have currently sold off to some enticing levels and would be well poised for a nice bounce should Trump soften his current positioning.

The bottom line is we think the world will look different in six months than it does now and perhaps so should your portfolio. Therefore, having a game plan is essential to navigating today’s uncertainty beyond simply buying the dip, as so many pundits are recommending.

One area that we like is the Canadian and U.S. bond market, which has gone nowhere in the past few years. We are seeing the best opportunities at the longer-end of the curve, meaning 10 years and longer. This ties into our thesis that rate cuts are on the horizon as the temporary inflationary impact of tariffs wears off and deflation ultimately sets in. Those with bond duration exposure will directly benefit from this, finally returning this asset to its historical relationship as a hedge against equity corrections.

In case we get it wrong on the equity front, as there is always the chance that tariffs become reversed and markets recover, we have a large weighting to structured notes that offer varying levels of upside exposure but with built-in downside protection.

We are favoring those called contingent coupons with 30 per cent downside barriers and on average seven to nine per cent annual coupons paid out monthly. This way investors can get an attractive yield while markets do their thing. Maximizing exposure to this within registered accounts has proven to be very beneficial, as notes are not tax efficient.

Finally, we are not going to cash but admittedly have been shoring up cash levels a bit in order to have some dry power to boost our equity allocations on any meaningful correction. Or, as Warren Buffett describes, using cash as a tool to take advantage of the inefficiencies in the market, not as a fixed part of his portfolio.

There can be uncertainty in markets, in economies and in geopolitics but it doesn’t have to live in your mind rent-free. Having a plan to mitigate risks is something not only within your control but also a great first step to at least collecting rent from your portfolio while the world is becoming a more hostile place.

Thank you for reading, and please feel free to reach out to any of our team members should you have any comments or questions about markets, your portfolio or just wanting to catch up. All the best, and keep investing wisely!

![]()

A closer look at energy markets – by Martin Pelletier

When looking at today’s environment for oil markets and the level of attractiveness for investment, we divide it into near-term versus long-term from a risk and return standpoint. Overall, we’re currently more defensively positioned in the near-term such that we expect to see more downside risk than upside potential. This is because OPEC has agreed to slowly return barrels to the market at a time where there remains the potential that a tariff war sends the global economy into a recession thereby impacting demand.

However, when looking over the next decade or so, we would have to agree with OPEC’s analysis that there could be a global supply shortage with peak U.S. shale production expected within the next past 5 years while global demand keeps rising. The situation could even be worse than expected should the coordinated attack by environmental organisations and government agencies continue to disrupt capital allocation decisions in the oil and gas sector thereby impairing new supply as a means to try and accelerate the ongoing transition to renewables.

In this regard, I recently attended Workshop on Communications and Robust Data held at OPEC’s headquarters in Vienna hosted by OPEC’s Secretary General, his Excellency Haitham al-Ghais for advisors, journalists, and energy sector professionals. I was impressed with the extensive work that goes into their data collection and analysis and there was no agenda other than trying to reinforce the importance of letting the data speak for itself.

The problem is you have Organisations such as the International Energy Agency (IEA) and others know full well the amount of capital required to offset global production declines and yet they are advocating for an all-or-nothing approach to energy transition. This is despite the fact that we still live in a world dominated by rising global oil demand with renewables still being very long way from making a meaningful dent in meeting global energy needs despite trillions of dollars being spent on this transition.

For example, did you know that despite a whopping $9.5 trillion being spent on “transitioning” over the past 20 years wind and solar only make up a paltry 4 per cent of today’s global energy mix, while electric vehicles have a total global penetration rate of between 2 to 3 per cent? And yet you have a company like Telsa with a market cap representing two-thirds of all vehicle manufacturers worldwide. It is as if this transition has already taken place according to today’s narrative.

It has even reached the point where outright false OPEC stories have been published by the main stream media with an immediate impact on oil prices with little to no repercussions from the perpetrators. I recently wrote about this back in October as the Biden Administration was doing everything it could do to get gasoline prices down ahead of the fall election.

All of this is having its desired effect as the price of oil is now back to where it was 20 years ago. Even without adjusting by inflation, in mere nominal terms, Brent is trading at the same level as it was in 2005. We do worry about future price spikes should this continue to impact capital investment and oil supply is suddenly no longer able to keep up with demand.

We do think that this combined with the expected downturn in U.S. shale presents an excellent opportunity for Canada to steal market share should we be able to get our oil to global markets and even eastern Canada that has imported US$200M of Russian oil in 2024 despite sanctions. Think about that.

There are even opportunities for us in global natural gas markets as we have seen reports indicating that the U.S. is actually aligning itself with Russia to provide the restart of its Nord Stream 2 gas pipeline to Europe. Back in August of 2022 Canada was visited by Germany’s Scholz whereby Prime Minister Trudeau at the time replied saying there was no business case for a natural gas export terminal – yet another outright false narrative this coming straight out of our Prime Minister’s Office. We worry very much that the exact same situation will play out should Mark Carney take office when instead we need to collectively reposition ourselves to gain share in the global LNG market instead of relinquishing it to hostile regimes like Russia.

Therefore, we’re waiting to see if there is finally a change in government here in Canada brave enough to finally change course by streamlining regulations instead of purposely adding to them and encouraging the build out of a national oil and gas infrastructure network. Should this be the case, then we expect a material bump in valuations of Canadian oil and gas companies but until then we’re still taking a cautious approach.

Market strategy and asset allocation

Much of the market attributed the downturn to U.S. President Donald Trump’s weekend comments about his willingness to accept short-term economic pain to advance his tariff policy, we as asset managers believe there are deeper and more structural factors at play.

One key underlying issue is the current administration’s need for significantly lower interest rates. Historically, the most effective way to push the U.S. Federal Reserve toward easing monetary policy is through signs of economic weakness and a declining equity market. This strategy may be particularly critical now, given the looming wall of U.S. debt maturities.

Nearly US$3 trillion in U.S. debt is set to mature in 2025, with about US$2 trillion consisting of short-term Treasury bills issued under former Treasury Secretary Janet Yellen. Compounding this pressure is the bond market’s need to absorb an additional US$2 trillion in the form of the U.S. budget deficit. This convergence of factors increases the urgency for lower rates to manage the mounting debt burden while stabilizing financial markets.

Investors can have several strategic approaches to market conditions, depending on their outlook for the global economy. One perspective is to view the current downturn as a buying opportunity. If you believe the economic weakness is temporary and expect Trump to stimulate growth through corporate tax cuts once rate reductions are in place, there are attractive entry points across the market.

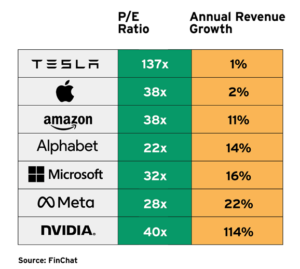

Last year’s market darlings, such as U.S. tech stocks, are trading at significantly lower levels. For instance, Tesla Inc. has fallen nearly 50 per cent from its peak, Nvidia Corp. is down 30 per cent and Amazon.com, Inc. has declined 20 per cent. If the Federal Reserve pivots to an easing stance, these stocks could rebound strongly, making this a potentially opportune moment for bullish investors to increase exposure.

However, we remain more cautious and are actively seeking ways to position defensively while incorporating embedded downside protection. This approach has already paid off in areas such as our Russell 2000 exposure, where our put protection has established a 100 per cent floor through November 2025, safeguarding us against further declines. In volatile environments such as these, capital preservation becomes as critical as seeking returns.

Our more bearish outlook stems from a reluctance to rely on the Federal Reserve to drive profits. We anticipate further downside in areas of the market that we categorize as “levered beta” — highly sensitive sectors that are disproportionately affected by economic slowdowns and policy shifts. As a result, we are focusing on defensive sectors that historically perform better in uncertain, recessionary environments.

Among our preferred areas of exposure are U.S. health care, where we have recently increased our positions due to the sector’s resilience and steady cash flows. We also maintain holdings in Canadian and U.S. utilities and dividend-focused equities, which offer stability and consistent income. Additionally, we have exposure to consumer staples through our U.S. value strategy, as these companies provide essential goods and are less susceptible to economic downturns.

In line with our protective stance, we have been employing principal-protected structured notes as a key component of our strategy. These instruments provide leveraged upside participation while safeguarding principal over a defined period. For example, we recently executed a note offering 1.55 times upside participation in specific indices with full downside protection for the next 2.5 to three years. This approach allows us to maintain equity exposure while mitigating the risks associated with further market volatility.

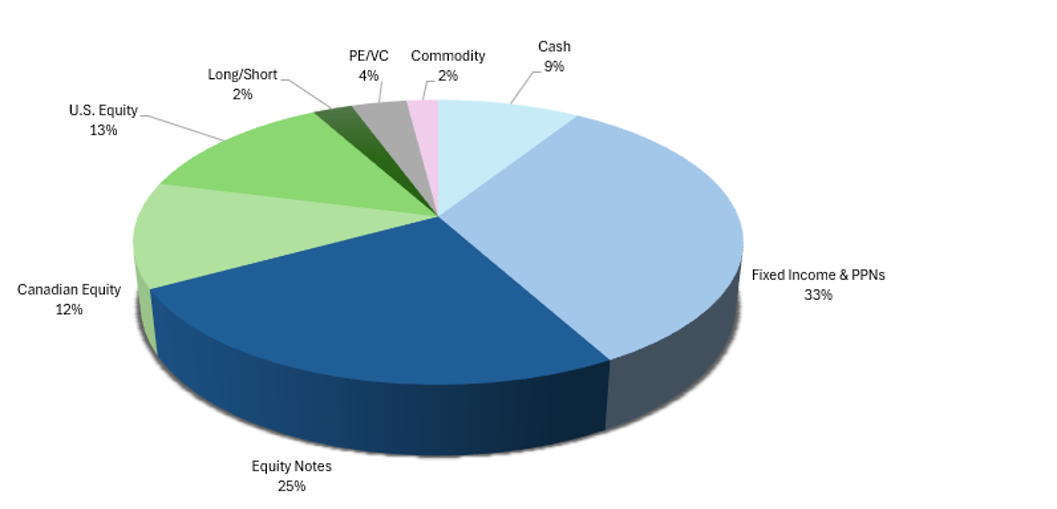

Overall, our strategy remains focused on balancing risk and reward. We have a sizable 9 per cent cash position to deploy should equity markets continue to weaken. We have boosted our fixed income exposure and principle protected notes to 33 per cent. Martin recently talked about this on BNN Bloomberg.

We also have a 25 per cent weighting to equity notes with a larger focus on monthly contingents with larger 30 per cent downside barriers. Canadian equity is at 12 per cent with a notable drop in energy as we discussed in our last monthly update. U.S. equities are at 13 per cent of which over 80 per cent is hedged with embedded put protection. This includes a recently added a position in the Health Care Select Sector SPDR Fund (XLV) which holds U.S. health care companies that will do very well in a recessionary environment. All of this is rounded out with a 2.5 per cent weighting to a long/short fund out of Toronto, 3.5 per cent in private equity and roughly 2 per cent in commodities.

Research, media, and reads of the month

A new regulation will soon require Canadians who stay in the United States for 30 days or more to register with the federal government. This notice was obtained by ABC News and signifies a shift from the traditional rule where Canadians crossing the northern border by land and staying for longer than 30 days did not have to register. The Secretary of Homeland Security has the authority to change this rule unilaterally. Starting from April 11, Canadians who stay for over 30 days will need to apply for registration with the federal government and will also be required to be fingerprinted. See Here

A new regulation will soon require Canadians who stay in the United States for 30 days or more to register with the federal government. This notice was obtained by ABC News and signifies a shift from the traditional rule where Canadians crossing the northern border by land and staying for longer than 30 days did not have to register. The Secretary of Homeland Security has the authority to change this rule unilaterally. Starting from April 11, Canadians who stay for over 30 days will need to apply for registration with the federal government and will also be required to be fingerprinted. See Here

What does Navy SEAL Team 6 and investing have in common?

Martin Pelletier: The importance of weighing the trust factor in relation to winning performance. Read Here

Its time in the market not timing the market – well here is another consideration

Dollar Cost Averaging: Over 20 years, the average CAGR is +4.0 per cent. The best return was +9.1 per cent and the worst return was -0.7 per cent. While the worst loss was minimal, it does show that equities have not always kept up with inflation, even if held for 20 years. Read Here If you bought European Stocks in 2000, you have finally broken even after 25 years! See Here S&P 500 Free Cash Flow Yield is at its lowest level in over 20 years. Probably Fine? See Here

Does history repeat itself?

This is one interesting chart showing the S&P 500 2018-19 during the first Trump Trade War in green versus the S&P 500 2025 during Trump Trade War 2.0 in red. See Here And the S&P 500 is right on top of its 200 day moving average See Here High flying tech stocks come with no free lunch but with plenty of risk and drawdowns. See Here Atlanta Fed is now projecting that Q1 GDP will be a whopping -2.8 per cent. See Here This current drawdown in the Nasdaq is the 30th time it declined 10%+ from an all-time high. See Here If your entire strategy is buying and holding an S&P 500 Index fund, you may need to adjust your expectations (or consider a different strategy)” See Here 31 of the last 32 times that SPY has opened down 1 per cent or more and then fallen another 1 per cent or more from the open to the close, it has been up 3 months later (65 trading days). See Here Vanguard forecasts US stocks to return 3.9 per cent annually over the next decade. Large-cap growth 0.6 per cent. See Here

U.S. recession watch

US employers cut more jobs last month than any February since 2009, new data shows, fueled by the Trump administration’s federal layoffs Read Here February Challenger job cuts +103.2 per cent year over year and the largest spike since August 2023 See Here US firms add 77,000 jobs, smallest gain since July, in ADP Data Read Here “The trouble with tariffs, to be succinct, is that they raise prices, slow economic growth, cut profits, increase unemployment, worsen inequality, diminish productivity and increase global tensions” Read Here Bernstein models that 25 per cent tariffs on Canada and Mexico adds $2700 per car, would wipe out 65 per cent of GM’s FCF, and lead to lower profits and lower investment in the U.S. See Here Vegas feels like a simulation glitch. No packed tables, no high rollers, just $27 cocktails and empty slot machines. Even the scammers look bored. The economy is worse than they’re admitting. See Here Delta CEO confirms that the US economy hit stall speed in February. See Here

Comrade Krasnov?

“Four senior members of Donald Trump’s entourage have held secret discussions with some of Kyiv’s top political opponents to Volodymyr Zelenskyy, just as Washington aligns with Moscow in seeking to lever the Ukrainian president out of his job.” Read Here President Donald Trump is planning to revoke temporary legal status for about 240,000 Ukrainians who fled Russia’s invasion of the country. Read Here The US has cut off intelligence-sharing with Kyiv in a move that could seriously hamper the Ukrainian military’s ability to target Russian forces Read Here “I’m afraid the brutal truth is: Donald Trump’s America is a better friend of Russia than it is of Europe.” Donald Trump sees the world divided by three power blocs: one dominated by Russia, another dominated by China and the third dominated by himself, says @AfNeil Watch Here Putin agrees to broker talks between the Trump administration and Iran on the Islamic Republic’s nuclear program Read Here Hegseth orders pause in US cyber-offensive against Russia See Here The Trump Administration has officially stopped financing new weapons sales to Ukraine and is considering freezing weapons shipments from US stockpiles, per WSJ Read Here The United States is drawing up a plan to potentially give Russia sanctions relief as President Donald Trump seeks to restore ties with Moscow Read Here A former spy and close friend of Vladimir Putin has been engineering a restart of Russia’s Nord Stream 2 gas pipeline to Europe with the backing of US investors, a once unthinkable move that shows the breadth of Donald Trump’s rapprochement with Moscow Read Here

Beyond tariffs

Some excellent work here by our friends over at GasBuddy on U.S. refineries and the continued reliance on Canadian crude oil. See Here In 1890, the Tariff Act came into place in the United States. It placed tariffs on imports of up to 50 per cent. While touted as a way to build American industry, there was also the hope it would force an annexation of Canada. It backfired. Let’s learn more. Read Here “Over time, they are a tax on goods. I mean, the Tooth Fairy doesn’t pay ’em!” Buffett said with a laughter. “And then what? You always have to ask that question in economics. You always say, ‘And then what?’” Read Here

On the Positive

We could all use a little bit of this

Citigroup mistakenly credited a customer account with $81 trillion. Read Here

Perception vs perspective

There is no advantage in your perception. The way that you win is when you move into perspective which is giving you an information advantage. Watch Here

The trouble with umbrellas

This will surely give you a good laugh. Watch Here

Good to have you back

My name is Jeff and we are Canadian. Watch Here

Spark your motivation.

16 quotes that are truly uplifting. See Here

A beautiful reflection.

How do you define yourself? Watch Here

Thanks for visiting

To find out more about the TriVest team and how we manage wealth, follow us on Twitter, LinkedIn or Facebook . Please email us if you want to find out more about our services.

The information contained herein has been provided for information purposes only. The information has been drawn from sources believed to be reliable. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document.

Transactions of the type described herein may involve a high degree of risk, and the value of such instruments may be highly volatile. Such risks may include without limitation risk of adverse or unanticipated market developments, risk of issuer default and risk of illiquidity. In certain transactions counterparties may lose their entire investment or incur an unlimited loss. This brief statement does not disclose all the risks and other significant aspects in connection with transactions of the type described herein, and counterparties should ensure that they fully understand the terms of the transaction, including the relevant risk factors and any legal, tax, regulatory and accounting considerations applicable to them, prior to transacting. This report may contain links to third-party websites. WAPC is not responsible for the content of any third-party website or any linked content contained in a third-party website. The inclusion of a link in this report does not imply any endorsement by or any affiliation with WAPC.

Structured Notes are not suitable for all investors. The notes do not pay dividends, and any dividends paid on the underlying constituent’s may not factor into the return calculation that determines your return. The protection and potential augmented returns on these notes are only available when held to maturity. These notes do not offer any protection if they are sold before the maturity date. If sold before the maturity date, returns may be positive or negative. These examples are for illustrative purposes only and should not be construed as an estimate or forecast of the performance of the Index or the return that an investor might realize on the Notes.

Wellington-Altus Private Counsel Inc. (WAPC) does not guarantee the accuracy or completeness of the information contained herein, nor does WAPC assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact your financial advisor.

All trademarks are the property of their respective owners.

© 2025, Wellington-Altus Private Counsel Inc. ALL RIGHTS RESERVED.

NO USE OR REPRODUCTION WITHOUT PERMISSION. www.wellington-altus.ca