Stepping Back: The 30,000-Foot Market View

One of the recurring challenges in writing our quarterly commentary is that by the time it reaches publication, parts already feel dated. This feels especially pronounced today as the pace of change appears to be accelerating.

After the S&P 500 declined by roughly 10 percent by the end of March, it took just 11 trading sessions to fully recover — among the fastest recoveries on record. As one market observer noted, “for situation monitors, the whiplash is a thing to behold…for everyone else, they may not have even noticed.” More notable was the speed at which the narrative reversed. By late March, many big-tech valuations appeared more fairly valued; by late April, they again appeared stretched.

The increasing frequency of such rapid shifts raises a broader question: Does this reflect a changing market regime?

Part of the explanation may lie in how the investing landscape itself has evolved over recent decades. Information is now disseminated globally in seconds. Combined with trading automation and declining transaction costs, this has contributed to a significant increase in market activity. In the late 1980s, the New York Stock Exchange averaged around 500 million shares traded daily; by 2020, this figure had doubled to over one billion.1

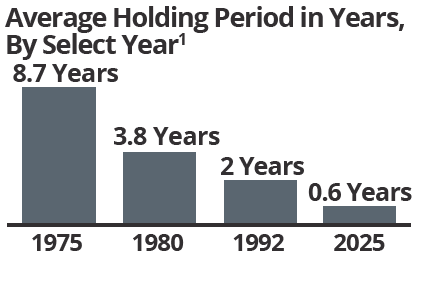

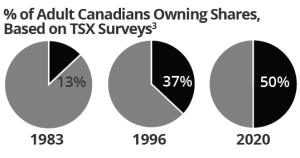

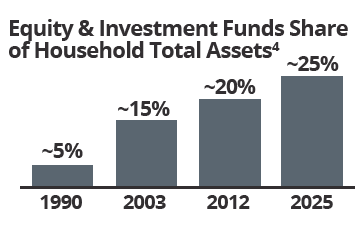

Participation has also become democratized. Building a diversified portfolio once required meaningful capital. Today, internet access and low-cost, diversified products have lowered barriers to entry. In 1990, equity and investment fund units represented just six percent of Canadian household assets. In 2025, they accounted for over 25 percent.2 This has also influenced investor behaviour. The average holding period for a stock, once spanning years, is now measured in months.

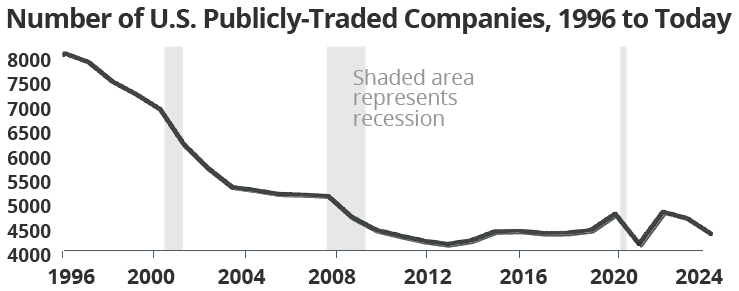

At the same time, market structure has shifted. What many may not realize is that the public company universe has contracted. U.S.-listed companies have halved from about 8,000 in 1997 to 4,000 today.3 Yet global market capitalization has expanded from about $50 trillion in 2011 to over $140 trillion today, with the rise of dominant U.S. and Asian corporates.4 Despite the shrinking public company universe, the range of investment products has expanded significantly. ETFs and derivatives now allow far more robust portfolio construction. Private equity and other alternatives, once largely reserved for institutions and ultra-high-net-worth investors, are more broadly accessible.

Meanwhile, even as total market values have risen, capital sitting on the sidelines has grown. U.S. money market funds have doubled to $8.2 trillion from their $4 trillion pandemic levels.5

Taken together, these shifts raise important questions: how should markets behave in an environment defined by faster information flow, lower barriers to entry, broader investor participation, yet fewer public companies and deeper sidelined liquidity? Do these changes imply a permanent shift in market behaviour? Are today’s valuations a reflection of these forces in action? It is plausible that markets have entered a period where sharper but shorter bursts of volatility and rapid narrative reversals become more common. Perhaps the anatomy of future bull and bear markets

will also differ from those of the past.

At the same time, it’s important not to lose sight of the broader context. If you invested $100,000 in the S&P/TSX Composite Index 30 years ago, it would have grown to over $1.4M today.* Markets may evolve and narratives may shift, but long-term wealth creation has remained remarkably consistent. Indeed, it may be the golden age of investing, where more investors participate in one of the greatest wealth-creation periods in financial history.

A personal note: Just as we’ve stepped back from the headlines for this commentary, we hope you, too, will find time to step away

this summer. We remain here taking care of things on your behalf and are available should you require assistance. Enjoy the sun!

*With reinvested dividends.

1. www.visualcapitalist.com/the-decline-of-long-term-investing/

2.https://www.nbc.ca/content/dam/bnc/taux-analyses/analyseeco/

mkt-view/market_view_250313.pdf

3. https://data.worldbank.org/indicator/CM.MKT.LDOM.NO?locations=US

4. https://en.wikipedia.org/wiki/Market_capitalization

THE INTERSECTION OF OIL & ARTIFICIALINTELLIGENCE

What Jevons Paradox Tells Us About the World Around Us

Jevons Effect (Jevons Paradox, “Jee-vons”):

An economic theory suggesting that efficiency gains can increase, rather than reduce, total consumption.

In 1865, British economist William Jevons observed a seeming paradox with the rise of the steam engine and its effect on coal consumption. As coal use became more efficient, he expected total coal consumption to decline. Instead, it surged. This observation remains relevant to the world around us.

Will the Middle East Conflict Reshape Global Energy Strategy?

In the spring, the Strait of Hormuz exposed the risks of routing roughly 20 percent of global supply through a single chokepoint. The resulting disruptions not only drove fossil fuel prices sharply higher but reinforced a broader reality: energy security is inseparable from national security. This has raised the question of whether it will accelerate a structural shift in global energy strategy.

Indeed, recent developments have prompted many nations to revisit their energy policies, including renewed interest in alternative sources aimed at reducing dependence on imported fossil fuels. However, expectations of a rapid decline in fossil fuel use may be overly optimistic. Even as efficiency improves, total oil demand has proven resilient — an outcome consistent with the Jevons effect. Today, while energy use per unit of GDP has declined over two decades, total energy consumption has not. Global oil consumption now exceeds 100 million barrels per day, up from around 60 million just half a century ago. In the U.S., per capita energy use has only declined at around half the pace of efficiency gains.1

What Jevons May Explain About Artificial Intelligence (AI)

This same effect may also apply to the evolving technological landscape. Given the rapid advancement of AI, there has been significant debate over whether it will replace labour. However, some economists argue that a Jevons-style dynamic is more likely: as the cost of AI-powered cognition falls, the total market for human intelligence may expand.2 For example, as AI makes professional services, such as legal work, accounting, consulting and financial analysis, cheaper and more efficient, overall demand could increase. Some studies already show that AI-exposed industries continue to see job and wage growth, suggesting that productivity gains may be complementing workers rather than replacing them. At the same time, certain entry-level roles, particularly for recent graduates, appear to be under pressure.

Of course, technological inflection points have always reshaped labour markets, with some jobs being displaced. Yet history also reminds us that new jobs are created and others augmented. For instance, when ATMs were introduced, many predicted the end of bank tellers. While teller roles initially declined per branch, ATMs reduced operating costs and enabled banks to open more branches. Similarly, in healthcare, advances in medical imaging raised concerns about radiologists becoming obsolete. Instead, imaging demand increased substantially due to lower costs and

an aging population, and radiologists continue to be essential for interpreting and integrating results.

1. https://www.eia.gov/todayinenergy/detail.php?id=48976

2. https://www.apollo.com/wealth/the-daily-spark/the-jevons-employment-effect-from-ai

CHANGE IS IMMINENT: FOUR GRAPHICS

The Difference 30 Years Makes: How the Investing Landscape Has Changed

As the front-page story highlighted, the investing landscape has changed dramatically over recent decades. Here are four ways:

1. Holding periods have become shorter — The average holding period of shares has fallen from roughly 8 years in the 1970s to just 7 months today. Automated exchanges have led to the rise of high-frequency trading using computer algorithms to analyze and execute trades. Retail investors have also become more active due to online trading platforms.

2. Public markets have shrunk — The number of publicly listed companies has declined by roughly 50 percent since the mid-1990s, largely in favour of private markets.2

3. Equity market participation has grown — Lower barriers to entry have democratized participation. Canada has the second highest equity market participation

globally, at roughly 50 percent of households. The U.S. leads at 55 percent, with Australia ranking third at 37 percent.3

4. Equities account for a greater share of wealth — Alongside rising equity participation, Canadian household wealth has reached new highs. As the saying goes, “a rising tide lifts all boats.“

1. Based on TOTMKUS Index; holding period = 1/turnover ratio; https://www.cibc.com/content/dam/cibc-public-assets/asset-management/pdfs/short-term-orientationof-equity-market-en.pdf#

2. https://data.worldbank.org/indicator/CM.MKT.LDOM.NO?locations=US; https://www.apolloacademy.com/public-equity-markets-have-changed-why-do-portfolios-still-look-the-same/

3. www.visualcapitalist.com/ranked-top-countries-by-stock-market-ownership/; https://www.cbc.ca/news/business/survey-says-almost-half-of-canadian-adults-own-stocks-1.208778

4. https://www.nbc.ca/content/dam/bnc/taux-analyses/analyse-eco/mkt-view/market_view_250313.pdf

HOUSING SEASON IS BACK IN FULL SWING

Helping (Grand)Kids Buy a Home: Five Ways to Structure Support

In 2025, 41 percent of first-time homebuyers received down payment gifts averaging $74,570, highlighting the significant role family members play in helping the next generation enter the housing market.1 For many high-net-worth families, there is value in seeing wealth put to use during one’s lifetime. However, support can take many forms, each carrying different tax and family law implications. When there are multiple children, it may also be important to consider how financial assistance to one child may affect fairness among siblings, and revisit an estate plan accordingly.

Here are five ways to structure support and related considerations:

Provide a Gift — When providing a financial gift to a child, you relinquish ownership and control of those funds. As a result, there’s a risk that funds won’t be used for a home purchase, or could become subject to division in the event of a future relationship breakdown, depending on how the purchase is structured. While Canada does not impose a gift tax (unlike the U.S.), liquidating investments to fund a gift may trigger taxable

capital gains or other taxable income.

Leverage Tax-Advantaged Accounts — Rather than providing a large lump sum gift, consider planning ahead through smaller contributions over time to help a child maximize tax-advantaged accounts. Both the First Home Savings Account (FHSA) and Registered Retirement Savings Plan (RRSP) provide tax advantages through tax-deductible contributions. The FHSA is particularly compelling because investment growth is tax-free and qualifying withdrawals to purchase a first home are also tax-free. Under the RRSP Home Buyers’ Plan (HBP), withdrawals of up to $60,000 can

be made tax-free (subject to repayment) for the purchase of a first home. Beyond the significant tax advantages, these accounts can help reinforce the value of saving and longer-term investing.

Loan Funds — Instead of an outright gift, funds may be advanced as a loan, with or without interest. A formal loan agreement should clearly set out repayment terms to avoid future misunderstandings. Proper documentation may help preserve the characterization of funds as a loan in the event of a relationship breakdown.* If desired, the loan can later be forgiven.

Co-Sign the Mortgage — This may help children qualify for a larger mortgage, secure more favourable borrowing terms or enter the market when they might not otherwise qualify. However, a cosigner is legally responsible for the debt if the borrower defaults. The arrangement can also affect the co-signer’s credit rating and borrowing capacity. In addition, trust reporting requirements may apply where the co-signer is required to be registered on title.

Co-Sign the Mortgage — This may help children qualify for a larger mortgage, secure more favourable borrowing terms or enter the market when they might not otherwise qualify. However, a cosigner is legally responsible for the debt if the borrower defaults. The arrangement can also affect the co-signer’s credit rating and borrowing capacity. In addition, trust reporting requirements may apply where the co-signer is required to be registered on title.

Co-Own a Property — While co-owning a property may help protect your interest in the event of a relationship breakdown, if you already own another property, the share of any future appreciation may be subject to capital gains tax upon sale or disposition.

Supporting a child’s home purchase is a significant and generous act. Since each form of support carries different financial, tax and family law implications, thoughtful planning can help ensure the outcome aligns with your intentions. For a deeper discussion, please call.

*The effectiveness of the loan in protecting against division in the event of a relationship

breakdown may vary by jurisdiction and a family law lawyer should be consulted. This

article is not intended to be a definitive analysis of family law.

1. https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/

housing-research/surveys/mortgage-consumer-surveys/2025-mortgage-consumer-survey

SUMMER JOB? BUILD RRSP CONTRIBUTION ROOM & AETIREMENT NEST EGG

A Case Study: Why Help a (Grand)Child File a Tax Return?

As the saying goes, “Give the man a fish, and you feed him for a day; teach the man to fish, and you feed him for a lifetime. ”The same principle applies to financial literacy. Small lessons introduced early, including something as simple as filing a tax return, can create habits and opportunities that benefit young people for years to come.

Is there a teen in your family, perhaps a (grand)child, niece or nephew, working during the summer or part-time after school? Helping them file a tax return can be a simple but powerful way to begin building long-term wealth while introducing financial habits early in life.

Many teens choose not to file a tax return if their income falls below the federal basic personal amount, which is $16,452 for 2026. What is often overlooked, however, is that even modest earnings can generate valuable Registered Retirement Savings Plan (RRSP) contribution room.

A Case Study: Building a Retirement Nest Egg From Age 14

Here’s a simple case study: At age 14, Sam begins working part-time as a lifeguard, earning $5,000 each summer. Her aunt helps her file a tax return, allowing her to accumulate RRSP contribution room at a rate of 18 percent of earned income, or $900 annually. Even without making RRSP contributions immediately, unused contribution room carries forward indefinitely. By age 22, after graduating from university, Sam has accumulated $8,100 of available RRSP room.

When she begins full-time employment and faces a 30 percent marginal tax rate,* she contributes the full $8,100 to her RRSP, saving approximately $2,430 in taxes ($8,100 x 30%). More importantly, if investing at an average annual return of 6 percent, that single contribution could grow to nearly $75,000 by age 60 —not a bad head start for someone just beginning their career!

And the lessons extend well beyond building a retirement nest egg:

Building Lifelong Financial Habits — Supporting teens in filing taxes early can help instill financial literacy and disciplined money management habits that can carry into adulthood, when tax returns will become a necessary part of managing personal income.

Tax-Deferred Growth and Future Tax Savings Potential — Unused RRSP room accumulated in early years can later be used to reduce taxable income, potentially increasing tax savings by claiming deductions when income and tax rates are higher in adulthood.

Future Flexibility Through RRSP Programs — RRSP savings can later be accessed as an interest-free loan, including up to $60,000 under the Home Buyers’ Plan for an eligible first-home purchase, or up to $20,000 through the Lifelong Learning Plan for eligible education or training. With rising housing and education costs, every bit helps.

Encouraging a Long-Term Saving Mindset — Early exposure to saving and investing can help young earners develop consistency and discipline, reinforcing the value of long-term compounding even through small contributions.

*Illustrative. Tax rates will vary depending on income and the province/territory of residence.

BEYOND THE EXISTENTIAL FEAR OF AI

Challenging the Artificial Intelligence Job Apocalypse

Is artificial intelligence (AI) coming for your job? According to The Economist, one in three people believe AI will cause widespread job losses, while seven out of 10 believe it will make it harder for people to find work.

Beyond the geopolitical volatility dominating headlines, the “AI job-apocalypse” has become a common narrative. It doesn’t help that the unemployment rate has been creeping upward, and that many recent college and university graduates are struggling to find work.

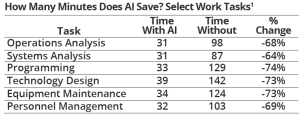

Of course, there’s no doubt that AI improves productivity. A recent paper from Stanford University examined how large language model tools (generative AI systems known as LLMs) are already significantly improving productivity across a range of knowledge based tasks. The results are striking. In every common work task that was studied, generative AI reduced completion time by at least half, and in most cases by around 70 to 75 percent (chart below). The study also found that LLM adoption among U.S. workers rose significantly from 30.1 percent as of December 2024 to 38.3 percent as of December 2025.1

Given the proven capabilities and rapid advancement of AI, it will undoubtedly eliminate some tasks and compress certain roles. There is evidence that this may already be happening.2 However, the notion that AI will imminently create permanent, widespread unemployment might be exaggerated.

Historically, productivity gains have often expanded economic activity rather than contracted it, creating new industries, new demand and ultimately new forms of employment. A related dynamic is seen in the Jevons Paradox: efficiency gains lower costs, which tends to increase overall consumption rather than reduce it. William Jevons observed this phenomenon in the 19th century when improvements in efficiency led to greater overall coal consumption, not less.

We’ve been here before. In 1951, when IBM introduced its electronic calculator, it was promoted as capable of replacing 150 engineers. Yet, 75 years later, engineers remain indispensable. Every major platform shift arrives with the familiar promise and worry: more output, fewer people, instant transformation. In recent decades, similar fears surrounded radiologists, telemarketers and travel agents. In practice, technology augmented these professions rather than eliminating them outright. Then there are the jobs that do not yet exist. One study suggests that technology has facilitated the creation of new occupations that now employ 60 percent of workers today (above). Indeed, the labour market

will evolve, as it always has when transformative technologies emerge. But worries of widespread and permanent unemployment may ultimately prove to be a shortsighted view of the world ahead.

1. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5136877

2. https://fortune.com/2026/04/06/ai-tech-displacement-effect-gen-z-

16000-jobs-per-month/

3. https://www.gspublishing.com/content/research/en/reports/2023/03/27/d64e052b-0f6e-45d7-967b-d7be35fabd16.html