The Shifting (Global) Order

We are living through a period of shifting order. Global alliances are outwardly frayed, old rules have been bent, and new ones are being formed. As Prime Minister Carney reminded the world in January: “The old order is not coming back. We shouldn’t mourn it. Nostalgia is not a strategy.”

Indeed, the shifts appear to be more rapid, with a near-constant stream of geopolitical surprises that have become almost routine. Amid shifting U.S. trade and tariff measures, evolving foreign policy and even war, uncertainty has grown and global conflict has widened. Even before recent events, there was a notable flight to safety in precious metals while the U.S. dollar declined. These defensive trades prompted some to ask once again: Is gold becoming the global reserve currency?

For now, they reflect a world placing greater focus on sovereign resource security and geopolitical insulation. Of course, geopolitics and economics remain intrinsically intertwined: while geopolitics explains how global leaders interact with their counterparts, economics can influence, and more importantly, constrain, their ambitions.

As events continue to reshape the global order, oil prices have spiked, renewing inflation worries. Over recent months, there have been broader shifts in markets. Technology stocks, long the market’s darlings, have faced pressure despite many posting solid earnings. Elevated capital spending has continued to draw scrutiny, even though returns on such investments can take years to materialize. Concerns about artificial intelligence’s potential to disrupt have also extended across sectors.

There has also been a rotation toward more undervalued market sectors. The Dow, considered by some young investors as “about as relevant as paper stock certificates or ticker tape,” outperformed the S&P 500 and NASDAQ to start the year, prompting headlines like “Boring is Back.”

Meanwhile, amid all of these shifts, some order emerged: the U.S. Supreme Court ruled that invoking tariffs under the Emergency Economic Powers Act was not legal. Although not expected to change the current administration’s approach, its clear legal boundaries augur well for the future. Nevertheless, uncertainty remains as renegotiations for the U.S.-Mexico-Canada Agreement (USMCA) draw near.

While the skies may appear cloudier for Canada’s economic prospects as a middle power, our position shouldn’t be underestimated: an energy superpower with vast natural resources, abundant fresh water, three coastlines, the world’s most-educated population and political stability. We have undoubtedly been dependent on the U.S., given our close proximity. Even so, an Oxford Economics analysis suggests that a full USMCA collapse would reduce Canada’s GDP by about 1.8 percent below baseline and cut private investment by 6 to 7 percent.2 By comparison, the early 1980s recession, driven by high inflation and high interest rates, saw output fall by 5 percent and unemployment reach 12 percent, a reminder that Canada has endured far more severe shocks and recovered.

Against this shifting backdrop, the growing dispersion we see today rewards a thoughtful and selective investment management approach. At a time when uncertainty feels amplified and global policy-making remains volatile, discipline becomes increasingly important, particularly when the range of possible outcomes is wide. The constant shifts should also remind us that no cycle, policy regime or market trend is ever permanent, reinforcing the importance of maintaining a longer-term view.

As advisors, we are here to help you navigate this shifting order. We continue to monitor the evolving global situation. If you have questions or concerns, please don’t hesitate to reach out.

Wishing you warmer days ahead.

In This Issue

The Debasement Trade Amid Geopolitical Tensions ………………………………………. 2

Global Equity Market Perspectives: Nothing Is Permanent …………………………….. 2

Tax Season: When It May Pay to Defer Deductions ………………………………………… 3

Canada: “Food Inflation Capital” of the G7 ……………………………………………………… 3

Planning Ahead: Six Ways to Minimize Taxes on Your Estate …………………………. 4

GOLD & SILVER’S RUN

The Debasement Trade Amid Geopolitical Tensions

Gold and silver opened the year with substantial momentum. By the end of January, silver had surged to around $120 per ounce (intraday), up 63 percent in the month alone and up more than 248 percent year over year. Gold futures posted their largest single-day dollar gain on record, rising about $231 per ounce, while spot prices reached $5,600 (intraday), up 92 percent from a year earlier. In early February, both metals corrected sharply, retracing part of January’s rapid advance.

What was driving demand? Some market observers point to the “debasement trade”: an effort to preserve purchasing power amid monetary expansion and fiscal strain. The investment thesis is simple: when governments expand the money supply aggressively, keep interest rates below inflation or run large fiscal deficits,t he real value of cash and fixed-income assets erodes. For investors worried about weakening currencies, gold and silver act as tangible assets with no sovereign liability attached. Recent developments have reinforced these concerns. In Japan, long-term government bond yields surged to record levels after the government unveiled a plan to increase spending while cutting the consumption tax in January.

Geopolitical Tension & the Commodities Imperative

Monetary concerns are only part of the story. Geopolitical tensions are reshaping capital flows and reserve strategies. Trade wars, tariffs and sanctions risks have pushed some governments to prioritize resource security, including stockpiling critical commodities. At the same time, the broader shift from global interdependence toward national self-sufficiency is strengthening demand for real assets. Since 2022, central banks including Poland, Turkey, India, China and Kazakhstan have significantly increased gold reserves partly as protection against geopolitical pressure or financial sanctions. This has raised the question: Is a commodities supercycle underway?

U.S. Dollar & Treasuries: Under Pressure

Traditional safe-haven assets are also facing scrutiny. For decades, the U.S. dollar and Treasuries were regarded globally for their stability, but this view may be changing. The dollar fell to a four-year low in January, fuelling headlines such as “How Trump Is Debasing the Dollar and Eroding U.S. Economic Dominance.” With lower interest rates and pressure for further cuts, the relative appeal of Treasuries may be diminishing. Other safe-haven currencies are also under pressure. The Japanese yen has weakened amid inflation and fiscal stimulus, leaving the Swiss franc as one of the few currencies still widely viewed as reliable. What comes next? Given the scale and speed of gains, it’s reasonable to ask whether certain defensive trades were overextended. By historical standards, gold and silver’s early-year surge was steep. Still, the underlying drivers persist, including monetary expansion and geopolitical fragmentation. In such an environment, diversified exposure to defensive sectors, including commodities, alternative assets and resilient segments of the equity market, can help mitigate risks tied to inflation, currency erosion and geopolitical shocks.

A BRIF LOOK ACROSS FOUR DECADES

Global Equity Market Perspectives: Nothing Is Permanent

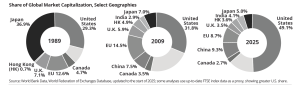

The share of global GDP among the world’s largest economies continues to shift, shaped by economic policy, technology and demographics. Equity market share has also shifted over decades. How have things changed? Seasoned investors may recall a time when the prevailing view was that Japan would surpass the U.S. as the world’s largest economy. During the late 1980s Japanese asset price boom, the Nikkei 225 rose from about 12,000 in 1985 to 38,915 in 1989: a 225 percent gain in four years. At that time, land under Tokyo’s Imperial Palace was said to be worth more than the entire state of California. In 1989, Japan held nearly 40 percent of global market capitalization. Two decades later, its share had fallen to just 7 percent.

Meanwhile, the developing economies of China and India largely absent from charts in 1989, were rapidly expanding. Today, they together account for over 13 percent of global market value. Where will we be in the next 20 years? Japan’s experience reminds us that economic leadership is never fixed, and today’s assumptions about global dominance may look very different in the future.

TAX SEASON IS HERE AGAIN

When It May Pay to Defer Deductions

Tax season is here again. Most taxpayers are eager to maximize deductions to minimize the taxes they pay. However, careful attention to tax planning may mean doing the opposite. In some situations, it may be beneficial to defer making deductions to achieve a greater future tax benefit. Here are some perspectives:

Registered Retirement Savings Plan (RRSP) — There may be situations in which delaying your RRSP deduction makes sense. If you expect that you will be in a higher tax bracket in future years, you can make a contribution up to your limit but not take the RRSP deduction in the year of contribution and, instead, carry that amount (or a portion of it) forward. Or, you can defer contributing until the year when you anticipate being in the higher tax bracket to maximize the taxes saved. Unused RRSP tax deductions can be carried forward indefinitely.

First Home Savings Account (FHSA) — Similar to the RRSP, if you have opened and contributed to a FHSA, you can carry forward undeducted contributions to a later year — and, generally, even beyond the FHSA’s closure. This may be beneficial for younger folks who might expect to be in a higher tax bracket in future years.

Charitable Donations — Eligible donations don’t have to be claimed in the year made and can be carried forward and claimed within the next five years. The federal tax credit has two tiers: 14.5 percent (for 2025, or 14 percent for 2026) on the first $200; 29 percent on amounts above $200 (33 percent if taxable income is in the highest tax bracket), with additional provincial credits. If you make smaller donations over different years, it may be beneficial to delay a claim and combine donations together to maximize the amount that generates the higher tax credit. As well, spouses may be able to claim each other’s unused charitable donations (including carried-forward amounts) from previous years to optimize the tax credit.

Capital Losses — If an investment is sold for less than its adjusted cost base in a non-registered account, the loss may be recorded as a capital loss. Net capital losses can be carried back three years or forward indefinitely to offset taxable capital gains. You can choose to apply them in a year when you have larger gains or a higher income to maximize the tax benefit.

Medical Expenses — Eligible medical expenses may be claimed as a federal non-refundable tax credit once they exceed a threshold. The claimable amount is the portion of expenses above the lesser of 3 percent of net income or $2,834 (for the 2025 tax year). Provincial or territorial medical expense tax credits also apply. Medical expenses

do not need to be based on the calendar year and may be claimed for any 12-month period ending in the tax year (provided they were not claimed previously). Therefore, it may be beneficial to delay claiming expenses if doing so allows you to include them in a 12-month period that produces a larger claim.

Tuition Tax Credit — Many students don’t use their tuition tax credit to reduce taxes because they have limited income at school. Up to $5,000 of unused tuition amounts can be transferred to a spouse, common-law partner, parent or grandparent. Any remaining amount can be carried forward indefinitely to future years. However, once a student has federal tax payable, they must generally use available carried-forward tuition amounts to reduce that tax before claiming certain other non-refundable credits.

INFLATION & AFFORDABILITY CHALLENGES

Canada: “Food Inflation Capital” of the G7

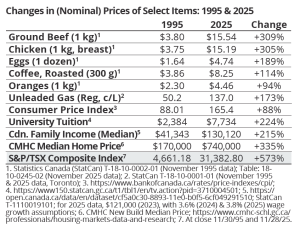

It may be difficult to recall a time when a litre of gas was 52 cents and a carton of eggs was just $1.64. That was 30 years ago. Fast forward to today, and Canada has now earned the title of “food inflation capital” of the G7 (Group of Seven advanced economies), with food prices rising by 6.2 percent in 2025 alone. In response, Prime Minister Carney recently introduced the Canada Groceries and Essentials Benefit (CGEB) rebate (an expansion of the existing GST/HST rebate) targeted at low-income earners.

While the Consumer Price Index (CPI), the federal government’s official measure of inflation, suggests average prices have risen roughly 88 percent over three decades, your grocery bills likely tell a very different story (chart). Inflation becomes especially troubling when incomes fail to keep up. For a growing portion of the population, this is a reality. When expenses, especially those like education and housing, become harder to afford, the impact is not just financial; it can influence confidence in economic

opportunity and heighten social divides. While affordability has come under increasing pressure, long-term investment performance paints a more encouraging picture.

Throughout the same period, investors have seen the S&P/TSX Composite Index rise more than 573 percent, even before accounting for reinvested dividends. That growth has outpaced the price increases across every category on the chart, including average home prices during a prolonged housing boom. Of course, those gains did not come without volatility, including four bear markets spanning a combined 40 months, two of which saw declines of more than 45 percent. Still, for those who stayed

the course, equities have proven to be one of the most effective tools for building wealth and offsetting inflation over the long run. If history is any guide, that’s encouraging news for long-term investors looking ahead to the next 30 years.

TAX SEASON PERSPECTIVES

Planning Ahead: Six Ways to Minimize Taxes on Your Estate

It is tax season once again. While many of us focus on reducing this year’s tax bill, it’s also a good time to consider how to manage future tax obligations. After all, as the old saying goes, “nothing is certain but death and taxes.” Planning ahead can help preserve more of your hard-earned wealth for your heirs, rather than the tax authorities.

In Canada, unlike the U.S., there is no estate tax in the traditional sense. Instead, you are deemed to have disposed of your assets at fair market value at death, and your estate is subject to tax on any accrued gains. For many estates, the greatest tax exposure comes from registered accounts such as Registered Retirement Savings Plans (RRSPs) or Registered Retirement Income Funds (RRIFs), capital gains in non-registered accounts and appreciated assets like vacation properties or other real estate.

Here are six ways to help minimize taxes on your estate:

1. Defer Taxes — In some cases, the tax liability on appreciated assets can be so significant that estates are forced to liquidate assets, such as a business or family cottage. Deferring taxes can help avoid this. A spousal rollover allows assets to transfer to a surviving spouse, spousal trust or certain eligible beneficiaries (i.e., disabled child, financially dependent child) on a tax-deferred basis, with the associated tax liabilities being deferred until your spouse dies or assets are sold.

2. Use Exemptions — Tax exemptions can provide meaningful savings. For example:

- Principal Residence Exemption (PRE): If you own more than

one property over time, careful planning around which property

is designated as your principal residence, and for which years,

can help reduce overall capital gains tax. - Lifetime Capital Gains Exemption (LCGE): Business owners

may be able to shelter gains on qualified business shares or

certain farm or fishing property.

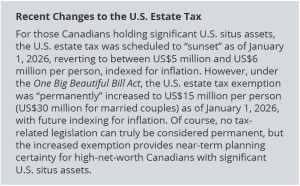

3. Don’t Overlook Foreign Estate Taxes — If you own assets outside Canada, or if your beneficiaries live in a country with an estate tax, planning is important. Many Canadians own U.S. assets. U.S. “situs” property, which includes U.S. real estate and shares in U.S. corporations, may be subject to the U.S. estate tax. (For dual citizens, U.S. citizens residing in Canada or Canadian citizens considered residents of the U.S., U.S. estate tax may apply to worldwide assets.)

There may be strategies to minimize potential U.S. estate tax, including disposing of U.S. situs assets before death, using joint ownership for U.S. property (which may help defer or reduce exposure, depending on ownership structure) or using a Canadian holding company, trust or partnership to own the U.S. situs assets. It’s also important to note that tax law can change (see inset for recent changes to the U.S. estate tax law).

4. Freeze Taxes — Business owners may choose to freeze the value of their business for tax purposes today, while transferring future growth to the next generation. By using an estate freeze, you can continue to control the business and lock in your future tax obligations, while the other party benefits from any increases in the value of the business (but is also liable for the future taxes on the growth).

5. Plan on Giving — Leaving a legacy through charitable donations can create a lasting impact while reducing taxes. Properly structured gifts may significantly reduce tax in the year of death and the preceding year. In the year of death, the maximum donation amount increases to 100 percent of net income (up from the 75 percent limit in a normal year). Gifts made during your lifetime, such as contributions to family members or charitable causes, can also reduce the size of your taxable estate while providing immediate benefits.

6. Use an RRSP/RRIF Drawdown Strategy — Registered retirement accounts often represent one of the largest tax liabilities at death. A proactive drawdown strategy may help reduce this exposure. Instead of withdrawing only the required minimum amounts, some retirees choose to gradually withdraw additional funds during lower-income years, smoothing income over time and potentially paying tax at lower marginal rates. This approach can also allow assets to be reinvested in more tax-efficient vehicles, such as a Tax-Free Savings Account (TFSA), or support gifting strategies. However, be aware that higher withdrawal amounts may have other consequences, such as potentially triggering the OAS clawback.

Plan Ahead

Estate tax planning can significantly affect what you leave behind. Professional advice can help ensure your strategy is structured properly, allowing you to preserve more of your estate for the people and the causes you care about.

Note: Tax minimization is only part of the planning equation. There may be

planning techniques, including the use of insurance, to help fund estate taxes

and avoid the forced sale of assets. For a deeper discussion, please call.