Australia’s Submarine Disaster: A Warning About Defence Megaprojects

We should start with a story, because it’s a good one. In the 1980’s Australia spent A$5 billion building six Collins-class submarines. The final bill came in at A$20 billion. The boats weren’t reliably operational until 19 years after the first one launched. The hulls leaked. The engines were too noisy. And here’s the detail you couldn’t make up: at the launch ceremony, entire hull sections were actually sheets of timber painted black so the submarine would look finished for the cameras!

HMAS Rankin, Collins-class submarine. Budget: A$5B. Final cost: A$20B. Time to operational readiness: 19 years. (image generated by Gemini)

Undaunted, Australia then hired France to build twelve next-generation submarines. After spending A$4 billion, they cancelled the whole thing in 2021. Not a single boat was delivered. They’ve now pivoted to nuclear-powered submarines under the AUKUS deal, projected at A$268-368 billion—which, for what it’s worth, is larger than the GDP of most countries. The Australians are nothing if not persistent.

We laugh, but we shouldn’t. Our own track record is just as bad.

Canada’s River-Class Destroyer Program and Cost Overruns

The River-Class Destroyer program—replacement frigates for the Navy—was budgeted at $26.2 billion in 2008. The Parliamentary Budget Officer now puts it at $84.5 billion, with some projections north of $108 billion. That’s a 312% overrun, and it’s still climbing.

Each ship will cost roughly $7.4 billion. The United Kingdom builds the same design for about half that. The difference is simple: Canada required domestic construction at Irving Shipbuilding, creating a sole-source monopoly. Without competitive pressure, costs settled at 30-40% above international benchmarks—and the schedule slipped by over a decade. This isn’t a scandal. It’s what happens every time. Everywhere.

Gemini’s rendering of the River-Class Destroyer (Type 26 variant). Original budget: $26.2B. Current estimate: $84.5–108B.

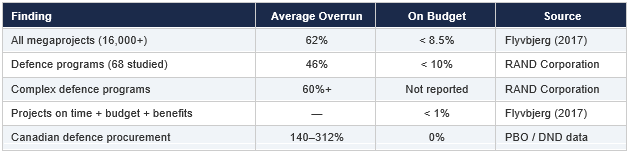

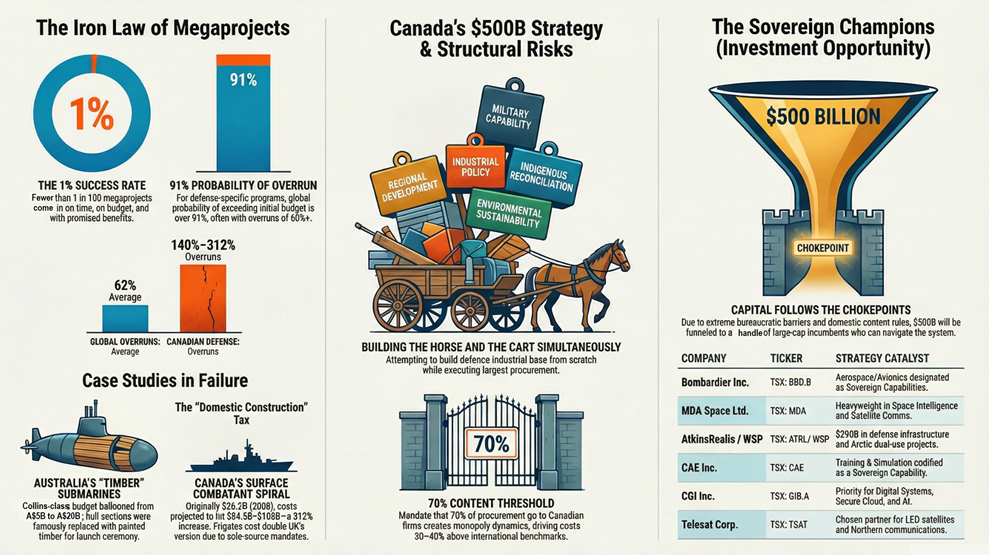

The Iron Law of Megaprojects: Why Defence Spending Goes Over Budget

An Oxford professor named Bent Flyvbjerg has spent his career studying this phenomenon. He looked at 16,000 megaprojects across 136 countries over seven decades and found something that won’t surprise anyone who’s watched government procurement up close: projects go over budget, over time, and under-deliver on benefits—with the reliability of a law of physics. He calls it the Iron Law of Megaprojects. Defence programs are among the worst offenders, and no country is immune.

Here’s what the data shows:

Source: Flyvbjerg (2017), RAND Corporation, Parliamentary Budget Officer. Canadian figures reflect Surface Combatant and National Shipbuilding Strategy overruns.

The bottom line: fewer than one in a hundred megaprojects comes in on time, on budget, and delivers what was promised. For defence programs specifically, the global probability of significant cost overruns exceeds 91%.

Canada’s $500 Billion Defence Spending Strategy

Against this backdrop, Prime Minister Mark Carney’s government has released the most ambitious defence spending plan in Canadian history. The numbers are genuinely impressive: over $500 billion in total defence-related spending by 2035, backed by $81.8 billion in Budget 2025, with a target of reaching 5% of GDP—up from 1.37% today.

Let’s give credit where it’s due. The security threats are real: Arctic sovereignty, NATO commitments, a world that looks markedly different than it did five years ago. The strategy identifies ten “sovereign capabilities” and commits to directing 70% of procurement to Canadian firms. As a statement of national ambition, it’s stirring stuff.

But here’s the thing: Carney is a McKinsey man, a Goldman man, a former central banker. He knows the Iron Law of Megaprojects. He almost certainly knows this document will not deliver what it promises—at least not on the timelines and budgets advertised. Which raises an interesting question: what if we’re reading it wrong?

Understood as an industrial policy, this strategy has serious problems we’ll get to in a moment. Understood as a political document (a vote-getting statement of intent, like the 500,000 homes pledge) it’s brilliant politics. It gives Canada a muscular answer to Trump’s 51st-state taunts. It plays well in every region. It wraps industrial subsidies in a flag. And it positions Carney as the serious leader for a dangerous time. None of that requires the Gripens or F-35s to arrive on schedule.

We say this with admiration, not as criticism, but for investment purposes we need to assess what will actually happen when this money hits the procurement system. And that’s where it gets complicated….

Canada’s Missing Defence-Industrial Base

Here is the fundamental problem: with the notable exception of Irving Shipbuilding’s yards in Halifax, Canada does not have a defence-industrial base. Not at scale. Not in most of the ten sovereign capability areas the strategy identifies.

Source: Gemini

There is no domestic manufacturer of armoured vehicles, no fighter jet production line, no torpedo factory, no established ammunition supply chain capable of wartime output. The strategy isn’t proposing to spend $500 billion through an existing industry. It’s proposing to build the industry and execute the largest procurement program in Canadian history at the same time. That’s like jumping out of an airplane and sewing a parachute on the way down!

The EV Battery Subsidy Lesson for Defence Policy

Even those of us who most ardently support the initiative have to acknowledge the uncomfortable recent precedent of the EV battery debacle. Just two years ago, Canada committed $52.5 billion in federal and provincial subsidies to build a battery manufacturing industry from scratch. The results: Northvolt—bankrupt. Honda—frozen for at least two years. Stellantis—construction halted, restarted, still no firm production date. The Parliamentary Budget Officer estimates it will take twenty years for taxpayers to break even on just the Volkswagen and Stellantis deals—not the five years the government promised. That works out to roughly $5 million in subsidies per job created.

For perspective, that $52.5 billion is more than the $34 billion it cost to build Trans Mountain and the $16 billion it cost to build the Site C hydroelectric dam—combined, with change to spare. Both projects had their own legendary overruns, but both are actually working: Trans Mountain tripled Pacific export capacity and pushed crude production to record highs, and Site C is now powering half a million homes. The battery subsidies could have funded a pipeline and a dam, and we’d have hard infrastructure generating revenue today instead of bankruptcy filings and indefinite pauses.

We’re not making an argument against ambition. We’re pointing out what Carney must already know: that reliably, predictably, and globally, governments fail when they try to conjure entire industries into existence with a chequebook. The EV battery strategy was one bet on one industry. The Defence Industrial Strategy is ten bets at once, at ten times the scale. As a taxpayer, are you comfortable with those odds?

None of this means the spending won’t happen—it likely will. The political will is real, the allied pressure is real, and the cheques will be written. But the gap between what gets announced and what gets delivered is going to be very, very large. That’s not cynicism. That’s how investors preserve their capital—by avoiding bad bets.

Which brings us to our actual job. We’re not the Auditor General. Our job is to understand where the capital flows—and who captures it. Here the news is much better for investors!

Source: illustration by Notebook LLM and Glen Evans

Investing in Canada’s Defence Spending: Follow the Capital

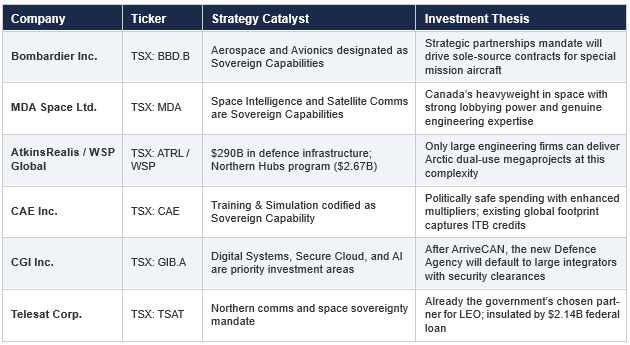

The strategy’s domestic content rules, compliance requirements, and enhanced multipliers for training and Indigenous workforce development create enormous barriers for anyone who isn’t already in the club. In practice, the capital will likely funnel to a handful of entrenched, large-cap incumbents who know how to navigate Ottawa and check every box. That’s not a flaw in the system—from an investment standpoint, it’s the whole point.

Currently, we’re asking ourselves, “who benefits most?” Our work has just begun, but these names are part of the list we’re considering. Time is on our side and this list will not doubt change over time (some are names we already own).

These TSX-listed companies (and others) may be structurally positioned to capture the largest share (Evans Family Wealth is not recommending any of these stocks):

Conclusion: What Canada’s Defence Strategy Means for Investors

Look—we want this to work. The threats are real, the armed forces are in genuinely poor shape, and the country needs to get serious. Carney has read the room correctly, and the ambition is welcome.

But the Iron Law of Megaprojects tells us how we should expect this movie to end. Based on past experience (some of it very recent), investors should expect these projects to disappoint. Indeed, history’s lesson is that 91% of the time Megaprojects fail to deliver. Expecting otherwise isn’t patriotic—it’s betting on hope over experience. As risk managers, we know that two things can be true at the same time. This policy may well be bad news for tax-payers while simultaneously being good news for investors.

For investors, we need to know the game we’re playing. When a government commits half a trillion dollars through a system built for political outcomes, the companies sitting at the chokepoints capture value whether or not the stated objectives are met. Ships may arrive late. Satellites may cost double. Arctic bases may take a decade longer than planned. But the contracts get signed, the invoices get paid, and the incumbents grow. That’s the opportunity we’re looking at.

We’re on it!

Glen