China vs West: Is the Competitive Gap Real?

Earlier this year, Honda’s CEO Toshihiro Mibe walked through a fully automated Chinese EV supplier factory, (no human workers on the floor) and reportedly said, “We have no chance against this.”

In March, the Jaecoo 7, a Chinese SUV made by a company unknown in Britain just 18 months earlier, became the best-selling car there, outselling the runner-up by 70%. France’s President Emmanuel Macron called the flood of Chinese goods a “question of life or death” for European manufacturing.

There’s a pervasive sense of futility in the West regarding China. You’ve probably heard it too: “China is playing chess while we’re playing checkers.” I had a good chuckle about this cover from The Economist—but couldn’t help wondering: isn’t it a little too early to tell?

The Subsidization Machine Behind China’s Manufacturing Rise

Last week, the Financial Times published “China Shock 2.0: the flood of high-tech goods that will change the world.” It’s a devastating read. They profiled a Chinese sensor maker whose prices fell 95% in five years. Competitors sustained by government subsidies sell below cost and refuse to exit. “I know the costs,” one founder said. “Some of their prices don’t make commercial sense.” Indeed, unless the goal was never to compete with Western manufacturers but to destroy them—source.

Honda’s CEO wasn’t witnessing Chinese superiority. He was witnessing what happens when a state subsidizes its manufacturers at three to nine times the rate of ours (per the OECD), undervalues its currency by 16% (per the IMF), and sustains money-losing companies with state capital so they never exit the market. No Western manufacturer, no matter how efficient, can compete on these terms. The playing field isn’t tilted. It doesn’t exist.

Why China’s Economy Depends on Western Demand

Here’s the irony: China’s rise requires our willing participation. Without access to Western markets, technology, and capital, the whole machine stalls. What China doesn’t want us to focus on is the fact that it must export—because domestic demand is collapsing. Behind that factory floor lies an economy in deflationary crisis: 80 million unsold homes, a quarter of listed companies unprofitable, household spending below 40% of GDP. The world isn’t their market; it’s their life support system. We are not being outcompeted. We are choosing to lose.

Combining Honda’s CEO and the French president: this is an existential risk to Western manufacturing, literally “life or death.” So how do we explain this poll?

Three Signals That the Global Order is Shifting

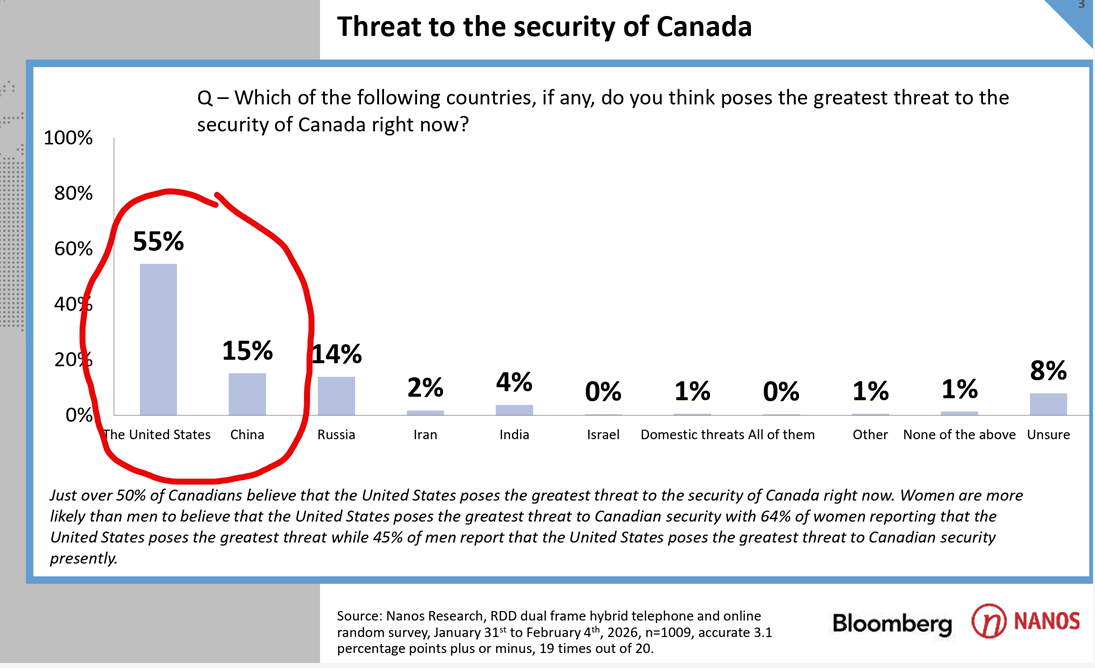

A Bloomberg-Nanos poll found that 55% of Canadians believe the United States poses the greatest threat to Canada’s security—more than China, Russia, and Iran combined. Canadians have legitimate grievances with America, and particularly with its leader. That said, the past six weeks should settle the question of who our real adversary is:

- The Veto. China vetoed the UN Security Council resolution to reopen the Strait of Hormuz—even though it receives roughly 40% of its oil through that waterway. Beijing sided with Iran over the global economy.

- The Hoard. While IEA nations coordinated the largest emergency reserve release in history—400 million barrels—China banned refined fuel exports at the worst possible moment. South Korea measured its LNG supply in single-digit days. Japan released 80 million barrels. Australia rationed. China kept its billion-barrel reserve largely intact. This is the COVID-19 playbook revisited: hoard supplies, let the world absorb the shock, gain relative advantage from the wreckage.

- The Weapon. China controls 94% of global permanent magnet production and imposed rare earth export controls that drove European prices to six times Chinese levels—while flooding those same markets with subsidized finished goods. This is not the behaviour of a trading partner. It is the behaviour of an adversary.

The Cold War 2.0 framing we introduced in January is no longer a metaphor. It is the operating reality.

The Strategic Response: How the U.S. is Changing the Game

The U.S. appears to be systematically cutting off the chokepoints through which China’s trade and energy flow—Venezuela, the Panama Canal, and now the Strait of Hormuz. Whether this is grand strategy or chaotic improvisation is debatable. That the board is changing is not.

The Hormuz gambit may well backfire—that’s the current consensus. But with oil back below $100 and Iran negotiating, outright pessimism might be premature. The war reminds Beijing that the strait through which it receives a third of its oil is not a free passage, and that Iran—a partner Beijing bankrolls but cannot control—no longer carries the same geopolitical weight.

Suspend disbelief for just a moment and ask yourself: now who’s playing chess and who’s playing checkers? It’s almost unthinkable, I know—but investors have to consider all possibilities. Increasingly, stock and commodity markets corroborate this story.

Keystone or Weak Link? What This Means for Canadian Investors

And then there’s us. After imposing 100% EV tariffs in 2024, our Prime Minister Mark Carney flew to Beijing in January and cut them to 6.1% on 49,000 vehicles—canola for cars, strategic protection traded for commodity access. Fair enough. Canada must act in its own best interest.

But the President of France and the CEO of Honda might have a different take.

We’ve written repeatedly, (in our copper thesis and our Cold War 2.0 analysis) that Canada is the natural keystone connecting American technology with secure raw materials. We have the rocks, the energy, the rule of law. But keystones only function when cemented into the arch. Canada’s China deal deepens dependency on the very adversary that vetoed Hormuz, hoarded oil while Asia rationed, and weaponized rare earths against our allies.

If you’re among the 55% who named the U.S. as our greatest threat, can I say something without you getting mad? Certainly, the U.S. is a difficult ally. But it is not the country that vetoed reopening Hormuz, hoarded reserves while neighbour’s rationed, or subsidized its manufacturers at nine times our rate to destroy our industrial base. Canadian investors can hold two thoughts at once: America is a bully, but China is no ally.

The Bottom Line: Reindustrialization is an Investment Opportunity

The mask is off. The West holds leverage it has barely begun to use: the consumer markets China desperately needs, the chokepoints its energy flows through, the technology it cannot replicate. The reindustrialization of the West is not a slogan—it is a security imperative backed by trillions in forced demand. Prime Minister Carney gets it, and with a new majority mandate he ought to get on with the job.

Canadians should wish him well. Our future depends on it.

Glen