When President Donald Trump ordered plans for a U.S. sovereign wealth fund in 2025, the criticism came quickly. What sovereign wealth? The United States runs chronic deficits. The funding was vague. Governance seemed to depend on whatever was politically expedient. Even former Trump Treasury Secretary Steven Mnuchin warned that the U.S. would have to borrow to fund it and cautioned against using the vehicle to buy private assets like TikTok.

At that point, the jokes almost wrote themselves.

What is the Canada Strong Fund and Why it Matters for Investors

But here’s the awkward part for Canadians: Prime Minister Mark Carney’s new Canada Strong Fund is built on a remarkably similar idea and, in one important respect, may be even bolder in its overreach. That may sound provocative, but as investors our job is to compare risks, incentives, structures, and outcomes before we make the investment.

To be clear, Carney’s plan addresses a real problem. Canada badly needs more investment in ports, mines, transmission lines, pipelines, LNG capacity, data centres, trade corridors, and faster approvals. Canada has long faced a business investment crisis. The need is real. The issue is whether another shiny financial vehicle solves the problem.

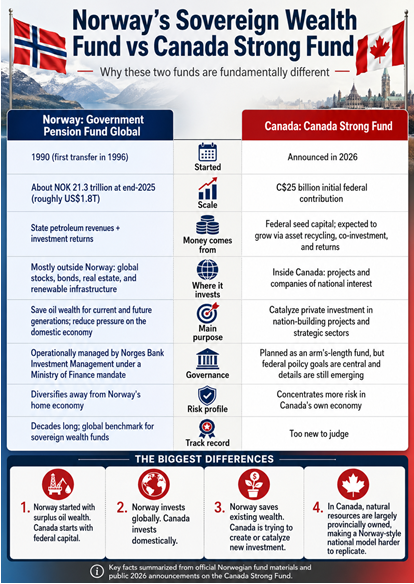

Sovereign Wealth Funds vs Canada Strong Fund

Take a minute to compare Norway’s Sovereign Wealth Fund to the Canada Strong Fund depicted below.

Why Canada Doesn’t Have Surplus Wealth to Deploy

A real sovereign wealth fund normally begins with surplus wealth. Norway’s fund was built from national petroleum revenues. Canada’s resource wealth is different. It is not sitting in Ottawa waiting to be swept into a national account. Alberta’s oil royalties belong to Alberta. Saskatchewan’s potash wealth belongs to Saskatchewan. Provincial resources are not a loose pile of national treasure waiting to be directed by the PM.

That’s not a political opinion. It’s Canada’s constitutional architecture. Even the Globe and Mail’s own explainer eventually acknowledged the problem: Canadian natural resources are owned and managed provincially, which makes it difficult to pool national resource wealth at the federal level without triggering a constitutional crisis.

That matters at any time. It matters even more in a country already straining under federal-provincial tensions. A constitutional crisis will make Canada even less attractive for investment.

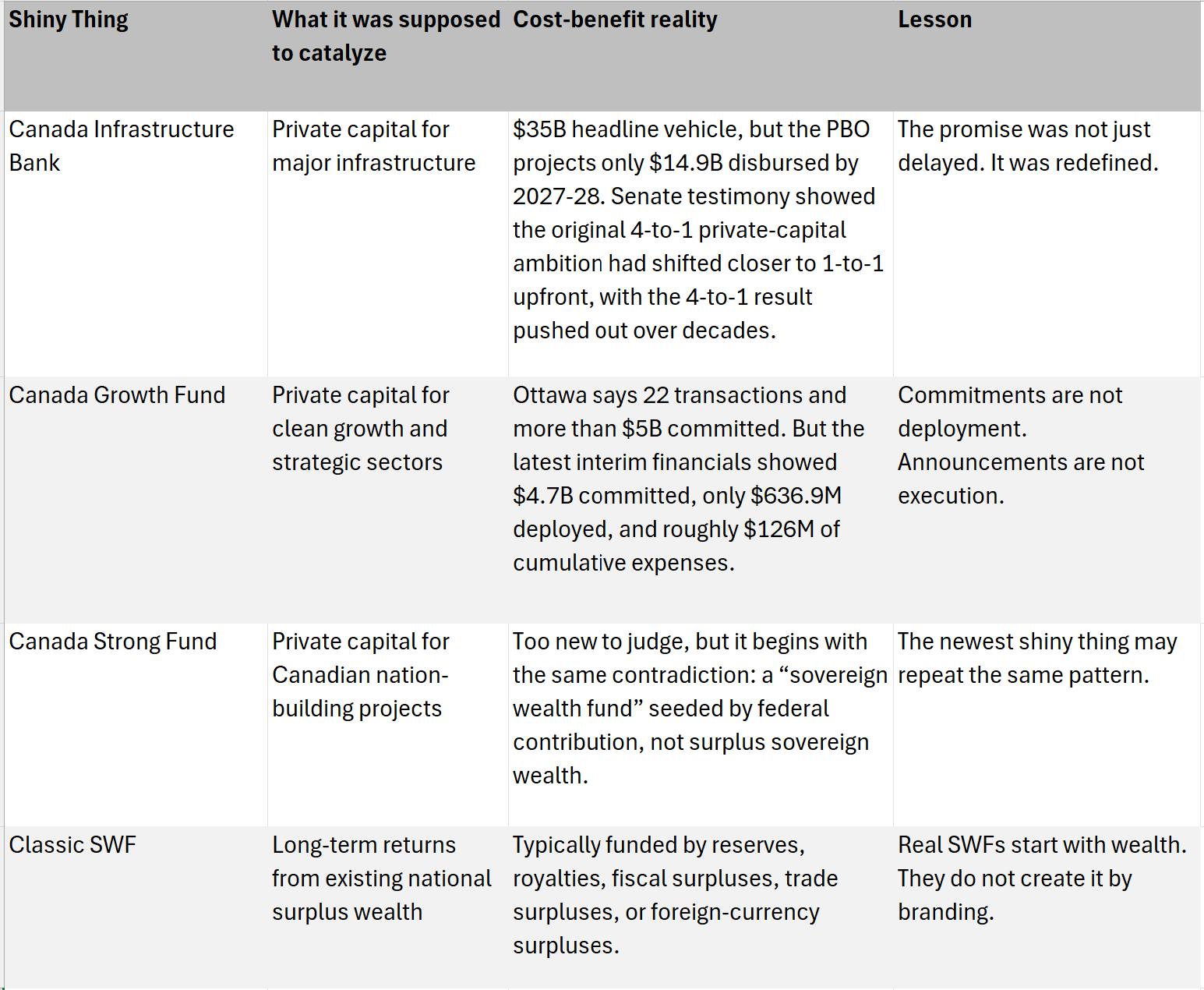

The Pattern of “Shiny” Investment Vehicles in Canada

The Canadian Strong Fund is the latest in a string of “Shiny Things” that have been aimed at addressing the lack of business investment over the past decade – let’s recap:

Why More Government Capital Isn’t Always The Answer

The Canada Infrastructure Bank was former Prime Minister Justin Trudeau and former Finance Minister Bill Morneau’s solution to the same problem way back in 2017. It was sold as a $35-billion catalyst that would attract $4 to $5 of private investment for every federal dollar. Years later, the Parliamentary Budget Officer estimates it will disburse less than half that headline amount by 2027-28. In Senate testimony, the private-capital promise had already been softened: closer to 1-to-1 at the front end, with the original 4-to-1 ambition pushed into the distant future. So much for “catalyzing” investments.

The Canada Growth Fund tells a similar story in newer clothes. It was launched as a $15-billion vehicle to unlock private investment in clean growth and strategic sectors. Some of its investments may prove useful. But the public headline is commitments, while the harder number is deployment. The latest available interim financials showed $636.9-million actually deployed against $4.7-billion committed. Meanwhile, cumulative expenses had already reached roughly $126-million. The machine is being built. The question is whether the machine is solving the problem, or becoming part of it.

Let’s be honest: none of this should surprise investors. No investor needs to be cajoled or incentivized to act in their own best interest. The inducement only is required when the returns and risk don’t align. So we see a series of failed or partially failed prior initiatives that haven’t addressed the core problem.

And before anyone fully reckons with the last shiny thing, a new shiny thing appears.

The Real Barrier: Regulation, Not Capital

To be fair, Mr. Carney is responding to an investment problem that predates him. The Financial Times recently reported that Canadian industry groups see red tape as a bigger problem than Trump’s tariffs. Forestry, energy, auto, telecom, mining, and pipeline leaders all pointed to overlapping rules, slow approvals, regulatory uncertainty, and a tax regime that repels investment. One representative described resource projects requiring hundreds of permits. Another put it bluntly: “Capital goes where it is welcome. And for too long, it hasn’t felt welcome here.” source.

Why Private Investment Isn’t Flowing to Canada

That is the elephant in the room. Capital does not need to be coaxed into genuinely attractive opportunities. It needs confidence that the rules will be clear, approvals will be timely, contracts will be respected, and returns will not be retroactively politicized.

There’s a deeper risk: this investment crowds out private investments, increases the debt and the leverage of the country. There have been musings about deploying some of “Canada’s” CPP investments and even private pension plans. Those are Canadian savings that should be sacrosanct.

The Bottom Line: Fix the Conditions, Not Just the Capital

Canada does not lack catalysts. Canada lacks the conditions for the reaction.

That is why the Canada Strong Fund deserves scrutiny, not cynicism. It may do some good. It may help finance projects Canada genuinely needs. But it cannot do the work of regulatory reform, permitting discipline, policy certainty, and respect for capital.

Fix those conditions, and private investment will not need to be dragged into Canada with another shiny vehicle. Leave those conditions broken, and no sovereign wealth fund, infrastructure bank, growth fund, or patriotic acronym will change the chemistry.

Glen