Gold Seal Monthly Review

Patience is easy in theory. Harder in practice. Especially when markets are strong, headlines are loud, and artificial intelligence (AI) is rewriting the investment narrative in real time.

This month’s edition draws directly from the CFA Society Okanagan Forecast Dinner, where Ryan once again had the privilege of hosting an evening of thoughtful debate and market insight. Two keynote speakers approached 2026 from different angles, yet landed on strikingly similar conclusions.

From forecast to formation: What we learned from the 2026 CFA Society Okanagan Forecast Dinner

Every January, we get a rare chance to sit down with some of the sharpest minds in the business, reflect on the past year, and talk about where the markets may be headed. This year’s CFA Society Okanagan Forecast Dinner brought two clear and timely messages: earnings matter more than headlines, and portfolios should be built to withstand a more concentrated and less predictable market.

Brent Joyce, CFA (BMO Private Wealth), focused on the idea of market resilience. His takeaway: companies that keep earning money tend to keep driving markets forward. Sam McClellan, CFA (BlackRock), looked at portfolio strategy in a world increasingly shaped by AI and shifting investment patterns. Despite their different approaches, both offered practical takeaways we’re applying directly in Gold Seal client portfolios.

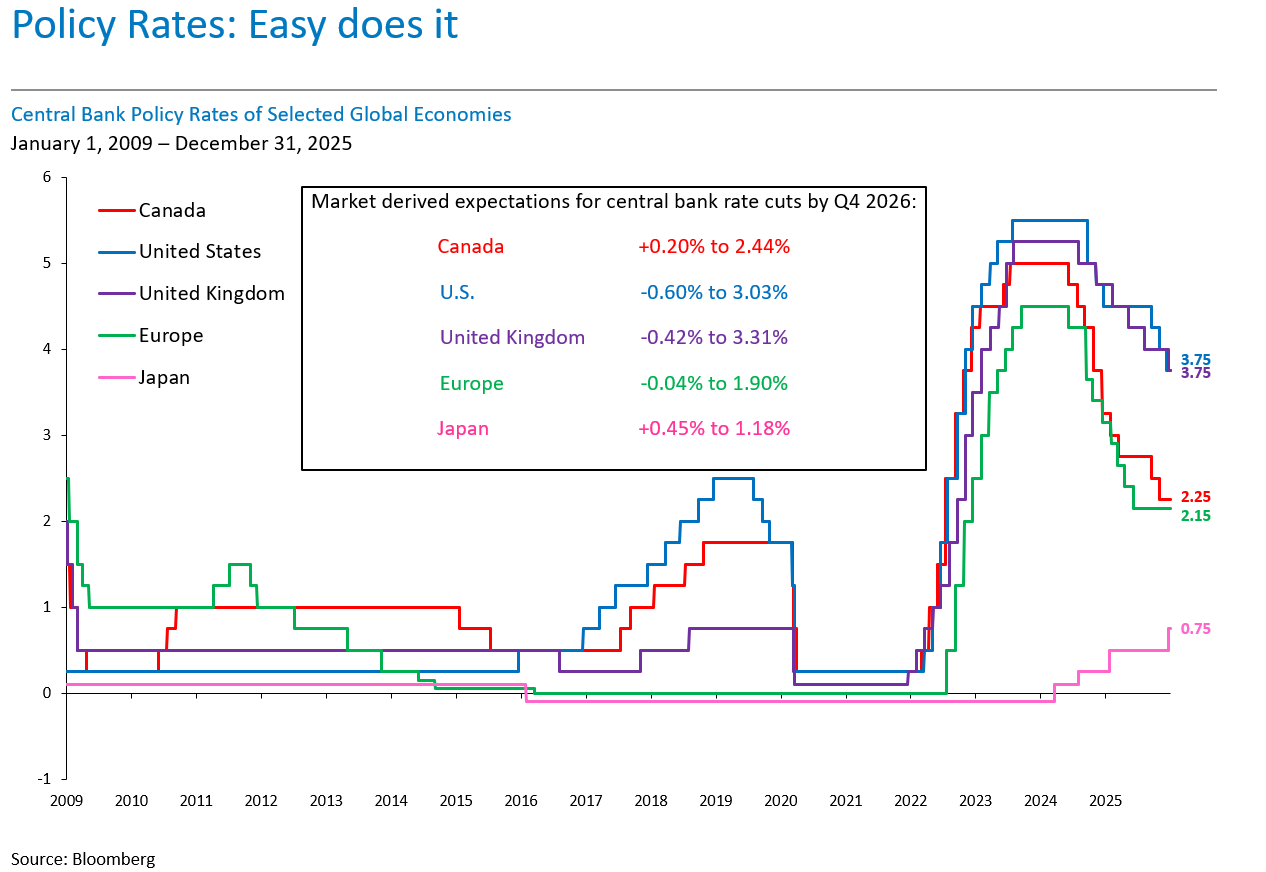

Interest rates: a slow shift, not a sudden change

We’re past the aggressive rate hikes of the last couple of years. Most central banks are now approaching interest rates like a dimmer switch by not rushing to lower rates, but stepping back from the brakes. In Canada, the policy rate is holding at 2.25%, while the U.S. sits between 3.5% and 3.75%. Other regions are following their own timelines.

This long-term view of global interest rates shows why 2026 will likely bring small, gradual changes rather than big, sudden moves.

For investors, this means cash and very short-term bonds may not remain as rewarding as they were. As central banks ease off, passive cash returns (such as those from GICs) could shrink and portfolios need to adapt. Income will need to be sourced more deliberately rather than assumed from short-term rates alone.

Stock markets: strong, but narrow

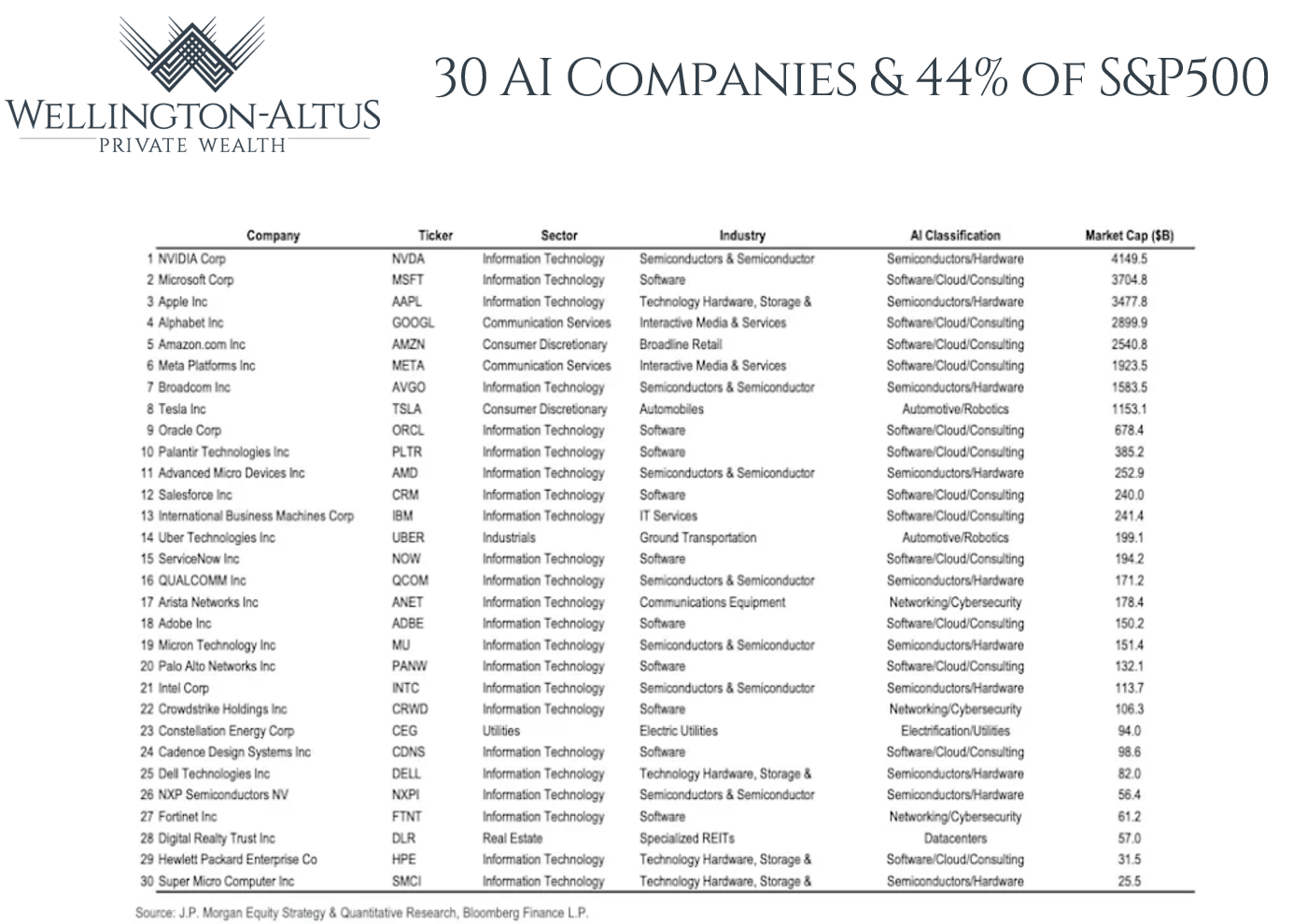

Last year was a good one for stocks, with the S&P 500 up 16.4%, the TSX nearly 29%, and emerging markets up more than 30%. But much of that success came from a handful of very large companies. Today, just 10 stocks make up over 40% of the S&P 500’s value, yet they only contribute around 32% of the index’s earnings.

Owning the index used to mean being broadly diversified. Today, it often means betting big on a few tech giants.

McClellan pointed out that AI is driving real investment, not just hype. In 2025 alone, over US$500 billion went into building data infrastructure. That’s a sign of lasting change and a capital expenditure cycle that extends beyond technology into energy, industrials, and infrastructure.

But that doesn’t mean investors should chase the biggest tech stocks. Encouragingly, earnings growth is beginning to spread beyond the narrow AI cohort. If that broadening continues, markets become inherently more resilient. Diversification within equities matters more than ever.

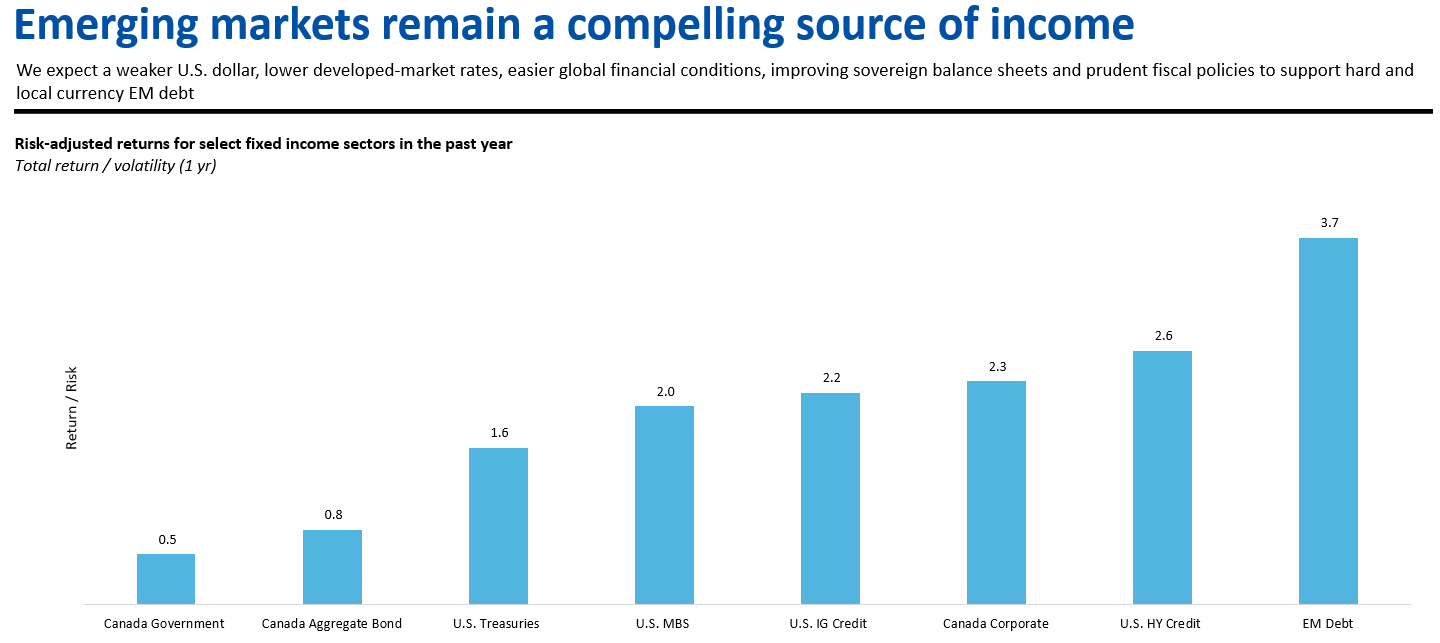

Bonds are useful again

Fixed income hasn’t been exciting for a long time, but that may be changing. With inflation easing and central banks slowing down, bonds are once again helping portfolios with both income and stability. McClellan warned that yields from cash and short-term investments may decline. To earn more income, investors may need to look across the portfolio and take a more active approach.

Source: ETF Implementation Guide – 2026 Year Ahead

Bonds like emerging market debt and investment-grade credit offered some of the best risk/reward profiles in 2025. Joyce also reminded us that higher starting yields make bonds more useful again, especially when the market faces unexpected volatility.

Diversification still matters, but it looks different now

Both speakers agreed: traditional diversification still works, but it needs a refresh. In 2022, stocks and bonds fell together, leaving many portfolios exposed. In 2025, that improved, but the lesson remains: not all “diversifiers” are created equal.

Gold made a comeback in both presentations, not as a flashy bet, but as a thoughtful way to add balance. Central banks bought over 860 tonnes of gold in 2025, showing that demand remains strong. Gold behaves differently than stocks and bonds, especially when the unexpected happens. It is not meant to lead in bull markets. It is meant to buffer portfolio when concentration risk or geopolitical stress surfaces.

How we’re applying this at the Gold Seal Financial Group

- We’re keeping equity exposure, but paying closer attention to how much risk is tied up in just a few names. More clients are benefiting from capped strategies and broader global equity exposure.

- For income, we’re shifting from relying on cash yields to combining high-quality credit, select non-Canadian bond markets, and dividend-paying investments.

- Bonds are back in favour, not because they’re exciting, but because they’re doing their job again.

- Diversification is being rebalanced. Gold and other “non-correlated” assets are being reviewed not as a bet, but as a buffer.

In short: the themes from this year’s dinner were timely and practical. Markets are delivering, but they’re doing so unevenly. Risks haven’t gone away, they’ve just changed shape. By staying thoughtful and selective, we’re helping clients participate in growth while staying prepared for the twists that may come.

Gold Seal Insights

Tanya’s Tips: Building Resilience in 2026

Understand concentration risk before it understands you.

Understand concentration risk before it understands you.

Broad market indices are more concentrated than many investors realize. Owning “the market” today often means owning a meaningful allocation to a handful of mega-cap technology companies. That is not necessarily a problem. In fact, many of those companies are exceptional businesses. But it does mean that diversification needs to be measured beneath the surface. Review your exposure not just by asset class, but by sector, geography, and even individual company weight.

Expect cash yields to decline and plan income deliberately.

GICs were unusually generous over the last two years. As central banks normalize policy, those yields will likely compress. Rather than relying on passive cash returns, income strategies should be designed intentionally across bonds, global credit, dividend payers, and other complementary sources.

Separate volatility from permanent impairment.

Markets move. Sometimes sharply. Volatility is uncomfortable, but it is not the same as permanent loss. A temporary drawdown in a fundamentally strong business or diversified portfolio is very different from owning a structurally impaired asset. Staying disciplined during volatility often determines long-term success more than identifying the perfect entry point.

Treat diversifiers as insurance, not performance leaders.

Gold, alternatives, and certain global fixed income exposures are not meant to outperform equities in strong bull markets. Their purpose is balance. When growth leadership narrows or unexpected stress emerges, true diversifiers can dampen portfolio swings. The key is understanding their role before you need them.

Focus on earnings durability, not headlines.

Headlines are designed to provoke reaction. Earnings are designed to measure business health. In an environment where artificial intelligence, policy shifts, and geopolitical uncertainty dominate the news cycle, anchoring decisions in earnings strength and cash flow resilience provides a steadier framework for decision-making.

Remember that discipline compounds.

Markets reward patience more often than prediction. Staying invested, rebalancing thoughtfully, and resisting the urge to chase recent winners are not dramatic strategies. They are effective ones. Over time, disciplined construction tends to outperform reactive positioning.

Mallory’s Memo: Your 2025 Tax Package

Tax season is approaching and your 2025 tax documents will be available through our secure client portal. To access your Tax Package:

Tax season is approaching and your 2025 tax documents will be available through our secure client portal. To access your Tax Package:

Visit: MyPortfolio+

First-time user? Click “Start here”; Forgot your password? Click “Forgotten password?”; Don’t know your User ID? Contact the Gold Seal team.

Once logged in: Open the Documents menu> Select Reports to download your Tax Package> Select Tax Slips to download your T-slips

If you prefer to use the Client Connect website, sign in and select “Vault” to see your Tax Slips and Tax Package.

Reminder, our tax slips are being issued up until April 1 2026. Third-party tax slips, such as those from mutual fund companies, are sent to you directly from those institutions. We strongly recommend not submitting your tax return early unless you are confident that all slips have been received. Missing documents can result in reassessments and unnecessary delays.

As always, if you are unsure whether your documents are complete, our team is happy to help.

Noteworthy Links

- OECD Economic Outlook (2025–2026)

- World Gold Council – Central Bank Gold Demand (2025)

- Bank of Canada Rate Announcement

- RBC iShares ETF Implementation Guide (2026)

- BMO Private Wealth 2025 Year-End Commentary

- Reuters 2025 Market Recap

Picture of the month