Gold Seal Monthly Review

“If you are distressed by anything external, the pain is not due to the thing itself, but to your estimate of it; and this you have the power to revoke at any moment.”

– Marcus Aurelius

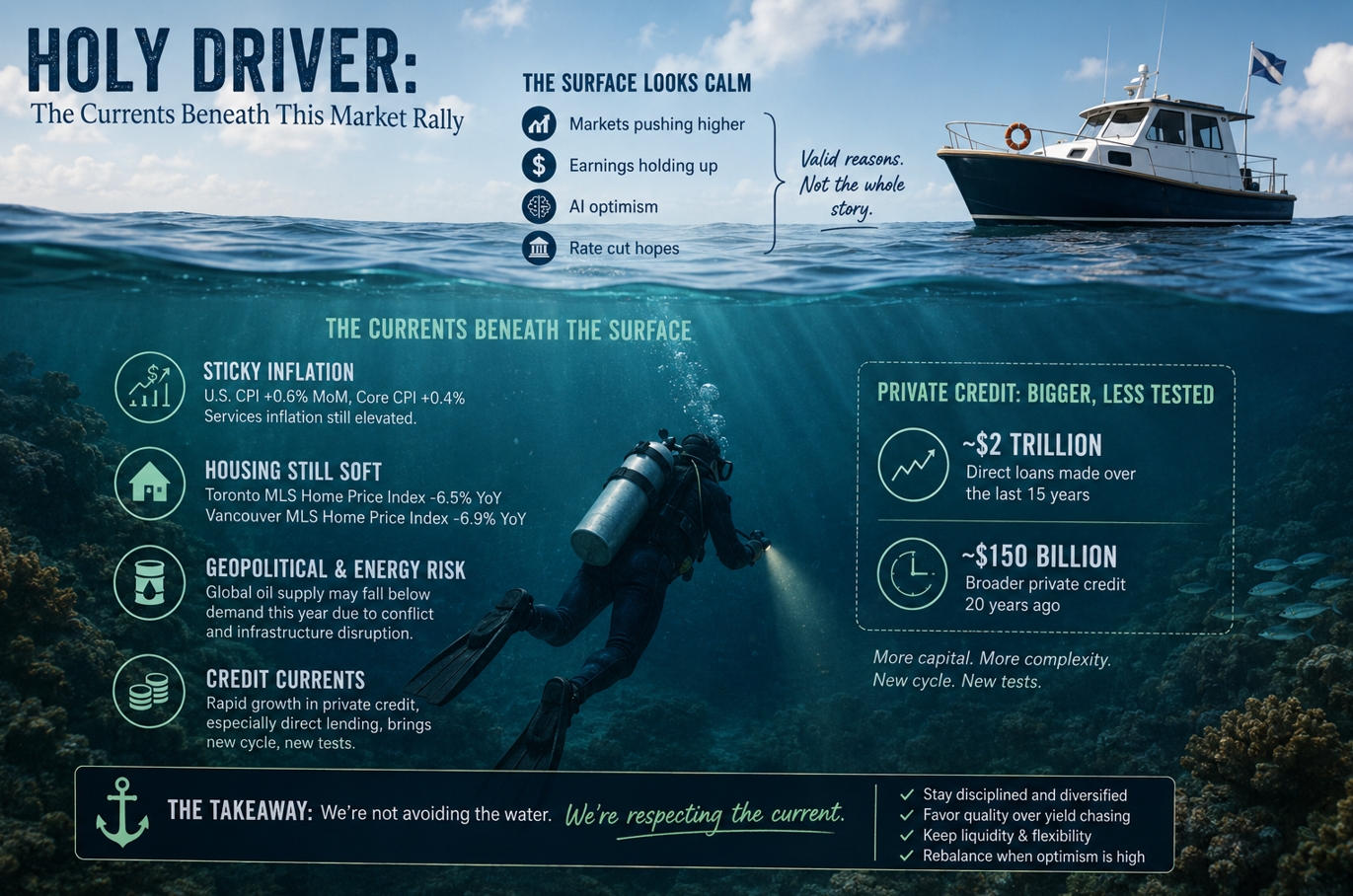

Holy driver: The currents beneath this market rally

Among the many specialized roles on our team, mine apparently includes being the one most likely to plan a vacation around a tank of air. Put more charitably, I am the resident scuba diver. Put less charitably, I occasionally pay good money to jump off a perfectly good boat.

With that in mind, I briefly considered calling this month’s note Holy Diver. Sensible heads prevailed, narrowly. Holy Driver is closer to the point anyway, because the real question today is not whether markets can keep floating. It is what, exactly, is driving them.

From the boat, the water can look perfectly calm. That is often true enough. It is also often beside the point. Under the surface, currents can be moving faster than expected, visibility can change, and the part you cannot see may matter more than the part you can. Markets feel a bit like that at the moment.

The surface has been hard to argue with. Equity markets have continued to push higher, artificial intelligence (AI) remains the favourite guest at every investment dinner party, and investors have been rewarded for leaning optimistic. There are legitimate reasons for that. Corporate earnings have held up, and by early May, 84% of S&P 500 companies that had reported first-quarter results had beaten earnings expectations. At the same time, the index was trading at a forward price-to-earnings ratio of 21.0, above both its five- and ten-year averages.

That tells us two things at once. Markets are not rising for no reason, but they are no longer inexpensive either. When investors are paying more for future earnings, the margin for error moves lower. Calm water is still calm water, but you probably want to check the current before jumping in.

Inflation is one of those currents. It is not the crisis it was in 2022, but it has also not gone quietly back to its room. Recent U.S. inflation data showed headline CPI rising 0.6% month-over-month and core inflation rising 0.4%. That matters because inflation does not need to be spectacular to be inconvenient. It only needs to be sticky enough to make central banks cautious and households grumpy.

Canada is not falling apart either, but it is hardly carefree. Some industry data has shown signs of stabilization, while housing remains soft in key markets. Toronto’s MLS Home Price Index was down 6.5% year-over-year, while Vancouver’s was down 6.9%. Affordability, job-market concerns, and trade uncertainty are still very much part of the backdrop.

That leaves central banks in an awkward position. Markets would very much like a neat little script where inflation fades, rate cuts arrive, and everyone gets back to enjoying themselves. The problem is that inflation, energy prices, trade frictions, and consumer confidence do not always follow the script. Markets love clean narratives. Economies, inconsiderately, keep behaving like economies.

Geopolitics adds another current. Energy is not just a price on a screen. It’s a physical system. Oil, natural gas, refined products, shipping routes, refinery inputs, fertilizer, and industrial supply chains all need to function in the real world before they show up politely in a spreadsheet. The risk is less abstract when global oil supply may fall below demand this year because conflict could disrupt the physical infrastructure that moves energy through the world.

That is a distinction that matters. A barrel of oil that becomes more expensive is one problem. A barrel that is delayed, rerouted, not refined, or not available where it is needed is another. Markets can reprice assets instantly. They are less elegant when the issue is physical availability rather than market pricing.

The same surface-versus-current idea applies to credit. One of the lessons of 2008 is that the most important risks do not always begin in the economic data everyone is watching. They can build quietly under the surface: lending standards, leverage, liquidity assumptions, asset values, and structures that seem stable until they are asked to prove it. This is not 2008, and private credit is not subprime mortgages in a new wetsuit. That said, some of the patterns are similar, and we find the reminder useful.

Private credit deserves attention because so much capital has moved into areas that offer attractive income and, at least on paper, less visible volatility. The focus here is really direct lending, a subset of private credit, which expanded rapidly after the Global Financial Crisis as banks pulled back and investors searched for yield. Over the past 15 years, roughly $2 trillion of direct loans have been made, while the broader private credit sector was only about $150 billion 20 years ago. That does not make the asset class bad. It does mean parts of it may be meeting their first proper credit cycle with a lot more passengers on board.

The uncomfortable part about private markets is that calm can be manufactured for a while. If something does not trade every day, it does not have to embarrass anyone every day. That may reduce reported volatility, but it does not eliminate risk. Liquidity still matters. Underwriting still matters. Leverage still matters. The price paid still matters. These things always matter most right after investors have temporarily decided they matter less.

So where does that leave us?

Not on shore, watching everyone else swim. Strong markets can stay strong longer than skeptics expect, and being reflexively negative has rarely been a useful personality trait, let alone an investment strategy. But when markets have been this good for this long, discipline becomes more important, not less.

For portfolios, that means staying diversified, but with intent. It means not chasing income just because it comes wrapped in a smoother-looking package. It means favouring quality of cash flow over clever structure, keeping liquidity available because you miss it most when it is gone, and rebalancing when optimism is high rather than waiting for the market to politely ring a bell.

The market still has drivers: earnings, AI, liquidity expectations, and the hope that central banks will eventually provide relief. Those may continue to support returns. But beneath the surface, inflation, energy disruption, credit quality, and valuation risk are moving too.

We are not avoiding the water. We are respecting the current.

Highlights from the 2026 Spring Economic Update

The federal government released its 2026 Spring Economic Update on April 28, setting out its fiscal and policy direction ahead of the fall budget. The headline number was better than expected: the projected 2025–26 deficit has been revised down to $66.9 billion from $78.3 billion in Budget 2025, largely due to stronger revenues and higher personal and corporate tax receipts. That is encouraging, particularly given that the Update also includes $37.5 billion in new measures over six years focused on affordability and cost-of-living support.

That said, a smaller deficit does not mean government debt is falling. It simply means the debt is growing more slowly than previously forecast. Federal debt is estimated at $1.33 trillion and is projected to rise to $1.63 trillion by the end of the decade. The more relevant measure is the debt-to-GDP ratio, which is projected at 41.5% in 2026–27 and expected to remain broadly stable through 2030–31. That stability is positive, but it depends on continued economic growth, manageable interest costs, and spending discipline. In other words, the fiscal picture is better than feared, but still far from fiscally disciplined.

From a planning perspective, the Update was relatively quiet. Personal and corporate tax rates remain unchanged, with no change to capital gains inclusion rates. The government also proposed targeted measures, including reduced CPP contributions beginning in 2027, permanent capital gains relief for qualifying sales to employee ownership trusts, extended Home Buyers’ Plan repayment flexibility, and expanded access to the Disability Tax Credit.

The new Canada Strong Fund is the most ambitious and controversial initiative, intended to attract private-sector investment into strategic Canadian industries such as clean growth, critical minerals, advanced manufacturing, and economic security. It is being presented as a sovereign wealth fund, but the comparison is imperfect. Traditional sovereign wealth funds (such as the one established in Norway) are often built from surplus national wealth, such as resource profits, and are designed to preserve and grow that wealth over time. Canada’s fund is being launched in the opposite fiscal context: the federal government is still running sizeable deficits and total debt is projected to keep rising. Put more plainly, this is not excess national wealth being invested for the future; it is a government-led investment strategy being introduced while Ottawa is already borrowing heavily. The fund may still help direct capital toward important long-term projects, but the bar should be high. To justify the risk, it will need clear governance, measurable return expectations, and discipline strong enough to prevent strategic investment from becoming political spending by another name.

Click here to read the Wellington-Altus 2026 Spring Economic Statement commentary.

Gold Seal Insights

Tanya’s Tips: Tax-Efficient Estate Planning

Tanya’s Tips: Tax-Efficient Estate Planning

Life insurance is often thought of as basic family protection, but for high-net-worth families it can play a much more strategic role. As wealth grows, the issue is often not whether there will be enough money, but whether there will be enough liquidity in the right place, at the right time, and without forcing the sale of important assets. Taxes at death, capital gains on private company shares or real estate, probate fees, and the equalization of inheritances can all create pressure on an estate. Insurance can help provide tax-free liquidity when it is most needed, allowing families to preserve investments, private businesses, cottages, farms, or other illiquid assets rather than selling them under pressure.

Joint last-to-die insurance is one common strategy. Rather than insuring each spouse separately, the policy pays out after the second death, which is often when the largest estate tax liability arises. This can be particularly useful where Registered Retirement Savings Plans (RRSPs) or Registered Retirement Income Funds (RRIFs) are expected to be taxed in the final estate, where a family wants to leave a tax-efficient legacy, or where one child may inherit a business or property while other beneficiaries need to be equalized fairly. In corporate planning, insurance may also create additional flexibility through the capital dividend account, allowing proceeds to potentially flow to shareholders or beneficiaries on a tax-efficient basis where available.

The key is that insurance should not be viewed in isolation. It is one tool within a broader estate plan, and its value depends on the family’s assets, tax exposure, liquidity needs, succession goals, and charitable intentions. Used properly, it can help convert a future tax problem into a planned funding strategy. Used poorly, it becomes just another expensive product with a glossy brochure and a suspiciously cheerful illustration. For high-net-worth families, the question is not simply “do we need insurance?” but whether insurance can help protect the estate plan from being disrupted at the worst possible time.

As part of our ongoing planning process, we regularly review whether your estate plan has the right liquidity, tax efficiency, and structure to support your long-term goals. Please reach out to us if you would like to revisit your estate plan and discuss whether any updates may be appropriate.

Ryan Archambault named to Kelowna Chamber of Commerce Top 40 Under 40

Congratulations to Ryan Archambault of Gold Seal Financial Group on being named one of the Kelowna Chamber of Commerce’s Top 40 Under 40 for 2026, recognizing outstanding young leaders for their business excellence, community involvement, and positive impact in the Central Okanagan.

Welcome Lindsey Ramsay to the Gold Seal Financial Group!

We are pleased to welcome Lindsey Ramsay to Gold Seal Financial Group as an Investment Associate. Lindsey brings a strong client-service mindset, excellent attention to detail, and a practical understanding of the operational side of wealth management. In her role, she will help support the day-to-day client experience, account administration, and the many moving pieces involved in delivering organized, responsive, and high-quality service. As our team continues to grow, Lindsey’s thoughtful and dependable approach will be a valuable addition for both our clients and our team.

Noteworthy Links

- Canadian home sales rose in April but remain 4 percent below last year

- Kevin Klein: It’s time to face facts about land rights in Canada

- Norway’s Sovereign Wealth Fund: About the Fund

- Carney and Smith sign pipeline deal that raises Alberta’s carbon price regardless

Picture of the month

Source: Visual Capitalist