Volatile markets often prompt investors to review their portfolios and asset allocations. While market volatility is rarely enjoyable, it can open the door to valuable opportunities – especially for tax-savvy investors. One such opportunity is the “triggering” or “harvesting” of capital losses.

How Tax-Loss Harvesting Works – and Why It Matters

For income tax purposes, a capital loss generally occurs when an investor disposes of capital property for an amount that is less than what the capital property was originally acquired for. Consider, for example, an investor who purchased one share of ABC Co. for $100/share. Following a market downturn, one share of ABC Co. now trades at $80/share. If the investor were to sell their ABC Co. share, they would realize or trigger a capital loss of $20 ($100 – $80).

Tax-loss harvesting is a tax strategy whereby an investor sells or otherwise disposes of a non-registered investment or other capital property with the intention of realizing a capital loss for tax purposes as described above. Once a capital loss has been realized by the investor, these losses can be used to generate a tax benefit.

The main benefit of capital losses for income tax purposes is that they can be used to offset capital gains realized by the investor. To continue our example, suppose that the investor also held one share of XYZ Co. in their portfolio. The investor purchased one share of XYZ Co. at a price of $100/share. Due to its defensive nature, XYZ Co. appreciated during the market downturn and now trades at $120/share. If the investor were to sell their XYZ Co. share, they would realize a capital gain of $20/share ($120 – $100).

When it comes time to prepare the investor’s income tax return, they will need to include the realized capital gain on the sale of XYZ Co. However, they may also include the harvested loss on the sale of their ABC Co. share. Essentially, the loss on the ABC Co. share can be used to offset the gain on the XYZ Co. share leaving the investor with no additional income or taxes as a result of these transactions.

Capital losses in excess of capital gains for the year can be carried back three taxation years to offset past capital gains, or carried forward indefinitely to offset future capital gains.

When Should You Consider Tax-Loss Harvesting?

Below are some of the more common circumstances that might warrant implementing this strategy:

- The investor reported significant capital gains in one or all of the three immediately preceding tax years. For example, if the investor realized capital losses in 2025, they could carry back these losses to the 2024, 2023, or 2022 taxation years.

- The investor anticipates a significant capital gain in the current year or a future taxation year.

- Consulting with their advisor, the investor has determined a need to rebalance or change portfolio allocations.

When a Loss Isn’t a Loss: The Superficial Loss Rules

A common question is “So, why don’t I just sell my ABC Co. shares at a loss and repurchase them right after the sale? This way I get the tax benefit of the capital loss but still own my ABC Co. shares”. This type of planning is prevented by specific rules known as the “superficial loss” rules.

Exposure to Superficial Loss Rules

The superficial loss rules state that if an investor has not truly disposed of the property or has disposed of the property to an “affiliated person”, the loss may be suspended or altogether denied.

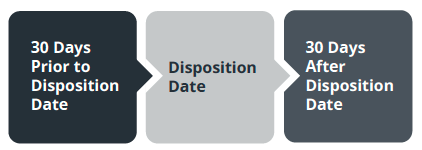

For the tax-loss harvesting to be effective, the investor or person affiliated with the investor cannot acquire the same or “identical property” in the period that starts 30 days before the disposition date of the property and ends 30 days after, and still hold the identical property at the end of that period.

Who are “Affiliated Persons”?

The following persons are considered “affiliated” with an investor for income tax purposes:

- An individual and a spouse or common-law partner

- A corporation and the person who controls the corporation, including their spouse or common-law partner

- A partnership and the “majority-interest partner”, and

- A trust and a “majority-interest beneficiary” including the spouse or common-law partner of such a beneficiary

Note: an individual is NOT affiliated with parents, grandparents, siblings, children, or grandchildren.

What are “Identical Properties”?

Identical properties per the Canada Revenue Agency are “properties which are the same in all material respects, so that a prospective buyer would not have a preference for one as opposed to another”.1 To determine if properties might be considered “identical properties” you need to consider the inherent attributes, rights, or qualities of the properties. Some examples include:

- Shares of a corporation with the same rights

- Debt issued by a debtor with identical rights(callable/putable, priority, etc.) irrespective of principal amount

- Convertible shares and the share into which they can be converted, and

- Index funds that track the same underlying index, but are offered by different financial institutions

Tax-loss harvesting can be a powerful tool in a volatile market, but the rules are complex, and timing is critical. Be sure to speak with your Wellington-Altus advisor and tax professional to determine if this strategy aligns with your specific circumstances.

1 Canada Revenue Agency, Archived IT-387R2 “Meaning of Identical Properties”, September 12, 2002.