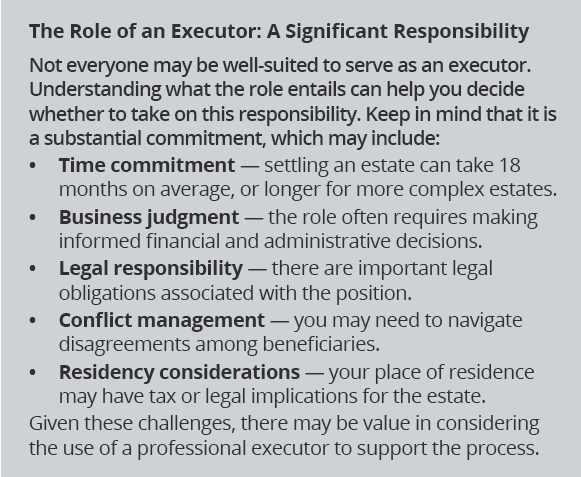

Estate Planning: Five Estate Executor Mistakes

Administering an estate can be a time-consuming and complex task, often made more challenging by emotionally difficult circumstances. All too often, executors can make mistakes that have the potential to lead to increased tax liabilities, conflict with or between beneficiaries or, worse yet, escalation to potential litigation. Equally concerning, the executor risks personal liability for these mistakes.

If you have been appointed to administer an estate, being aware of these potential pitfalls may help as you contemplate the role. As you plan for your own estate, carefully selecting your executor is important to prevent these and other mistakes.

Here are five common errors:

1. Overlooking directives in the will. Estate lawyers suggest that executors can sometimes ignore parts of the will, such as forgiving loans that were to be collected, perhaps due to a lack of knowledge or because it is easy or convenient. Others may choose to distribute assets differently than directed within the will, under the belief that they have a more ‘fair’ idea for this distribution. However, neither situation is within an executor’s authority, exposing them to potential liability.

2. Failing to communicate. Sometimes executors become so involved in the process that they neglect to communicate. One of the executor’s duties is to respond to reasonable enquiries from beneficiaries. Silence can often be misinterpreted as being secretive or suspicious, which can prompt estate disputes. Maintaining transparency and ongoing communication can go a long way in helping to prevent conflict.

3. Making distributions too early. If distributions are made too early, such as before taxes or other liabilities are paid, the executor may be held personally responsible. This can often happen when the executor succumbs to pressure from beneficiaries for distributions. However, any outstanding debts of the deceased must be paid before estate assets can be distributed to beneficiaries—and it is the job of the executor to identify these debts. Sometimes the executor overlooks the importance of determining whether there are unknown creditors, which often involves a time-consuming process of creating a public notice. Advertising for creditors can protect the executor should a creditor make a claim after the estate has been distributed.

4. Trying to keep costs low. Some executors may act too prudently in trying to limit estate expenses. However, this may lead to higher eventual costs. For example, if an executor decides to do the tax returns without the help of an accountant, they may miss eligible tax credits or deductions. In the past, advertising for creditors in the newspapers of multiple cities was very costly, so some executors avoided this process to save money, only to be caught by surprise when creditors eventually made claims.

5. Treating estate funds as their own. Given the assets often available within an estate, some executors may wrongly use estate funds for their own purposes, such as to make loans to themselves or family members. Others may make more honest mistakes, such as using funds to cover travel costs for family members to attend the funeral. If estate funds are used incorrectly, the executor may be held personally liable. Additionally, if the executor acts unreasonably or in their own self-interest, they may not be entitled to compensation from the estate.1

As you support others, be aware of the responsibilities and potential pitfalls that come with serving as an executor. For more perspectives, or for an introduction to an estate planning specialist who can provide greater insight, please call the office.

1. https://www.canlii.org/en/on/onca/doc/2016/2016onca521/2016onca521.html

The information contained herein has been provided for information purposes only. The information has been drawn from sources believed to be reliable. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document. Wellington-Altus Private Wealth Inc. (WAPW) does not guarantee the accuracy or completeness of the information contained herein, nor does WAPW assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact your financial advisor. Transactions of the type described herein may involve a high degree of risk, and the value of such instruments may be highly volatile. Such risks may include without limitation risk of adverse or unanticipated market developments, risk of issuer default and risk of illiquidity. In certain transactions prospective investors may lose their entire investment or incur an unlimited loss. This brief statement does not disclose all the risks and other significant aspects in connection with transactions of the type described herein, and prospective investors should ensure that they fully understand the terms of the transaction, including the relevant risk factors and any legal, tax, regulatory and accounting considerations applicable to them, prior to transacting. The information contained herein may include the opinions of representatives of third-party companies or organizations and may not necessarily reflect that of Wellington-Altus (WA) or its representatives. All third-party products and services referred to or advertised are sold by the company or organization named. While WA may have referral arrangements with some third-party companies or organizations, WA does not specifically endorse any of these products or services and is not liable for any claims, losses or damages however arising out of any purchase or use of third-party products or services. All insurance products and services are offered by life licensed advisors of Wellington-Altus Insurance Inc. or other insurance companies separate from WAPW.

© 2026, Wellington-Altus Private Wealth Inc. ALL RIGHTS RESERVED. NO USE OR REPRODUCTION WITHOUT PERMISSION. www.wellington-altus.ca

If you no longer wish to receive commercial electronic messages from Wellington-Altus Private Wealth Inc., please send an email to unsubscribe@wellington-altus.ca