With interest rates rising substantially from their lows, there has been increased attention to low-risk, fixed-income investments like Guaranteed Investment Certificates (GICs). Yet, there may be alternatives that produce a more favourable financial result, after factoring in the potential tax implications.

Consider the potential tax implications for a GIC returning four percent held in a non-registered account: after tax, this would yield two percent for an investor with a marginal tax rate of 50 percent. While this may provide comfort during volatile markets, there may be alternatives.

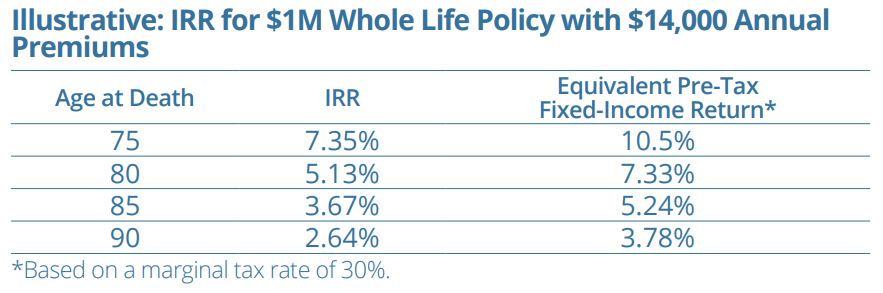

For high-net-worth investors, there may be an opportunity to use permanent life insurance as part of an investment strategy. At a basic level, many permanent life insurance products have fixed premiums and a guaranteed payout at death. (Note: for permanent life insurance, the insured has to qualify for insurance.) As such, it is possible to calculate a rate of return (IRR) on the premiums. Since proceeds upon death are paid tax free, the only variable is the age of death. Take, for example, a whole life policy for a non-smoking, healthy 50-year-old male who pays an annual premium of $14,000 for a $1 million policy:

Permanent life insurance may be a way to achieve fixed-income exposure. A participating whole life insurance policy (or “par policy”) allows you to share in the potential surplus earnings of the insurer. Your premiums go into a broader participating account that is professionally managed by the insurance company, which is used to pay insurance claims, expenses, taxes and other costs. The majority of the assets in the participating investment account are typically longerterm debt instruments, such as public and private fixed-income investments, bonds and mortgages. The account would also generally include some real estate and equity holdings. This provides the policy owner with access to a low-cost, widely diversified portfolio that is often difficult to replicate for individual investors

The Par Policy: Additional Benefits for HNW Investors In addition to the traditional benefit of holding life insurance — to support loved ones in the untimely event of the death of an income earner — there may be other benefits. The participating investment account is tax-sheltered for the policy owner, compared to a fixed income portfolio of investments that would be taxable. Based on the account’s performance, annual “policy dividends” are often issued to policyholders and these can be used to purchase additional paid-up insurance that would increase the policy’s death benefit coverage, which will be received tax-free by the beneficiary upon the death of the insured. This provides the policy with the potential to outperform the after-tax fixed-income component of a traditional balanced portfolio.

In the event of premature death, the par policy would have a high probability of outperforming the fixed-income component of a traditional investment portfolio (see the illustrative chart that shows an increasing IRR at a lower age for a whole life policy). The estate value may also be higher, as income, and any growth, would be earned on a tax-free basis inside the policy. Death benefits paid from the policy may not be subject to probate where the policy is owned outside of a corporation and certain specific beneficiaries have been named, such as a spouse or children (in provinces where applicable).

For business owners, there may be additional tax benefits through the use of the company’s capital dividend account, further enhancing the value of the estate. Corporations with active business income may also be able to offset the tax that can result from the passive income rules.

Be aware that funds must be committed to this strategy, so sufficient assets should be available after premiums are paid to cover lifestyle and other needs annually. If premium payments stop, the policy could lapse; or, if the policy is surrendered, the policy owner would be entitled to a surrender value. However, if funds are required, the cash value may be withdrawn or borrowed against. Annual policy dividends are not guaranteed, though many of the large life insurance companies have continued to pay these on a regular basis. Policy premium rates will vary by age and health; a medical examination is often required to determine premium payments.

If you are interested in learning more, we can run an insurance illustration for your particular situation.

The information contained herein has been provided for information purposes only. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information has been provided by J. Hirasawa & Associates and is drawn from sources believed to be reliable.

The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document. Wellington-Altus Private Wealth Inc. (WAPW) and the authors do not guarantee the accuracy or completeness of the information contained herein, nor does WAPW, nor the authors, assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact me for individual financial advice based on your personal circumstances. WAPW is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada.

©️ 2023, Wellington-Altus Private Wealth Inc. ALL RIGHTS RESERVED. NO USE OR REPRODUCTION WITHOUT PERMISSION