Planning Ahead: Six Ways to Minimize Taxes on Your Estate

It is tax season once again. While many of us focus on reducing this year’s tax bill, it’s also a good time to consider how to manage future tax obligations. After all, as the old saying goes, “nothing is certain but death and taxes.” Planning ahead can help preserve more of your hard-earned wealth for your heirs, rather than the tax authorities.

In Canada, unlike the U.S., there is no estate tax in the traditional sense. Instead, you are deemed to have disposed of your assets at fair market value at death, and your estate is subject to tax on any accrued gains. For many estates, the greatest tax exposure comes from registered accounts such as Registered Retirement Savings Plans (RRSPs) or Registered Retirement Income Funds (RRIFs), capital gains in non-registered accounts and appreciated assets like vacation properties or other real estate.

Here are six ways to help minimize taxes on your estate:

1. Defer Taxes — In some cases, the tax liability on appreciated assets can be so significant that estates are forced to liquidate assets, such as a business or family cottage. Deferring taxes can help avoid this. A spousal rollover allows assets to transfer to a surviving spouse, spousal trust or certain eligible beneficiaries (i.e., disabled child, financially dependent child) on a tax-deferred basis, with the associated tax liabilities being deferred until your spouse dies or assets are sold.

2. Use Exemptions — Tax exemptions can provide meaningful savings.

For example:

- Principal Residence Exemption (PRE): If you own more than one property over time, careful planning around which property is designated as your principal residence, and for which years, can help reduce overall capital gains tax.

- Lifetime Capital Gains Exemption (LCGE): Business owners may be able to shelter gains on qualified business shares or certain farm or fishing property.

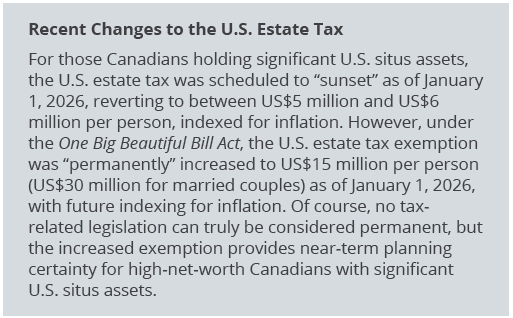

3. Don’t Overlook Foreign Estate Taxes — If you own assets outside Canada, or if your beneficiaries live in a country with an estate tax, planning is important. Many Canadians own U.S. assets. U.S. “situs” property, which includes U.S. real estate and shares in U.S. corporations, may be subject to the U.S. estate tax. (For dual citizens, U.S. citizens residing in Canada or Canadian citizens considered residents of the U.S., U.S. estate tax may apply to worldwide assets.)

There may be strategies to minimize potential U.S. estate tax, including disposing of U.S. situs assets before death, using joint ownership for U.S. property (which may help defer or reduce exposure, depending on ownership structure) or using a Canadian holding company, trust or partnership to own the U.S. situs assets. It’s also important to note that tax law can change (see inset for recent changes to the U.S. estate tax law).

4. Freeze Taxes — Business owners may choose to freeze the value of their business for tax purposes today, while transferring future growth to the next generation. By using an estate freeze, you can continue to control the business and lock in your future tax obligations, while the other party benefits from any increases in the value of the business (but is also liable for the future taxes on the growth).

5. Plan on Giving — Leaving a legacy through charitable donations can create a lasting impact while reducing taxes. Properly structured gifts may significantly reduce tax in the year of death and the preceding year. In the year of death, the maximum donation amount increases to 100 percent of net income (up from the 75 percent limit in a normal year). Gifts made during your lifetime, such as contributions to family members or charitable causes, can also reduce the size of your taxable estate while providing immediate benefits.

5. Plan on Giving — Leaving a legacy through charitable donations can create a lasting impact while reducing taxes. Properly structured gifts may significantly reduce tax in the year of death and the preceding year. In the year of death, the maximum donation amount increases to 100 percent of net income (up from the 75 percent limit in a normal year). Gifts made during your lifetime, such as contributions to family members or charitable causes, can also reduce the size of your taxable estate while providing immediate benefits.

6. Use an RRSP/RRIF Drawdown Strategy — Registered retirement accounts often represent one of the largest tax liabilities at death. A proactive drawdown strategy may help reduce this exposure. Instead of withdrawing only the required minimum amounts, some retirees choose to gradually withdraw additional funds during lower-income years, smoothing income over time and potentially paying tax at lower marginal rates. This approach can also allow assets to be reinvested in more tax-efficient vehicles, such as a Tax-Free Savings Account (TFSA), or support gifting strategies. However, be aware that higher withdrawal amounts may have other consequences, such as potentially triggering the OAS claw back.

Plan Ahead

Estate tax planning can significantly affect what you leave behind. Professional advice can help ensure your strategy is structured properly, allowing you to preserve more of your estate for the people and the causes you care about.

Note: Tax minimization is only part of the planning equation. There may be planning techniques, including the use of insurance, to help fund estate taxes and avoid the forced sale of assets. For a deeper discussion, please call.

The information contained herein has been provided for information purposes only. The information has been drawn from sources believed to be reliable. Graphs, charts and other numbers are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. This does not constitute a recommendation or solicitation to buy or sell securities of any kind. Market conditions may change which may impact the information contained in this document. Wellington-Altus Private Wealth Inc. (WAPW) does not guarantee the accuracy or completeness of the information contained herein, nor does WAPW assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Before acting on any of the above, please contact your financial advisor. Transactions of the type described herein may involve a high degree of risk, and the value of such instruments may be highly volatile. Such risks may include without limitation risk of adverse or unanticipated market developments, risk of issuer default and risk of illiquidity. In certain transactions prospective investors may lose their entire investment or incur an unlimited loss. This brief statement does not disclose all the risks and other significant aspects in connection with transactions of the type described herein, and prospective investors should ensure that they fully understand the terms of the transaction, including the relevant risk factors and any legal, tax, regulatory and accounting considerations applicable to them, prior to transacting. The information contained herein may include the opinions of representatives of third-party companies or organizations and may not necessarily reflect that of Wellington-Altus (WA) or its representatives. All third-party products and services referred to or advertised are sold by the company or organization named. While WA may have referral arrangements with some third-party companies or organizations, WA does not specifically endorse any of these products or services and is not liable for any claims, losses or damages however arising out of any purchase or use of third-party products or services. All insurance products and services are offered by life licensed advisors of Wellington-Altus Insurance Inc. or other insurance companies separate from WAPW.

© 2026, Wellington-Altus Private Wealth Inc. ALL RIGHTS RESERVED. NO USE OR REPRODUCTION WITHOUT PERMISSION. www.wellington-altus.ca

If you no longer wish to receive commercial electronic messages from Wellington-Altus Private Wealth Inc., please send an email to unsubscribe@wellington-altus.ca