Last Month in the Markets: April 1 – 30, 2026

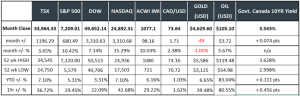

Index returns based on index value (source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis. Price returns are reflected)

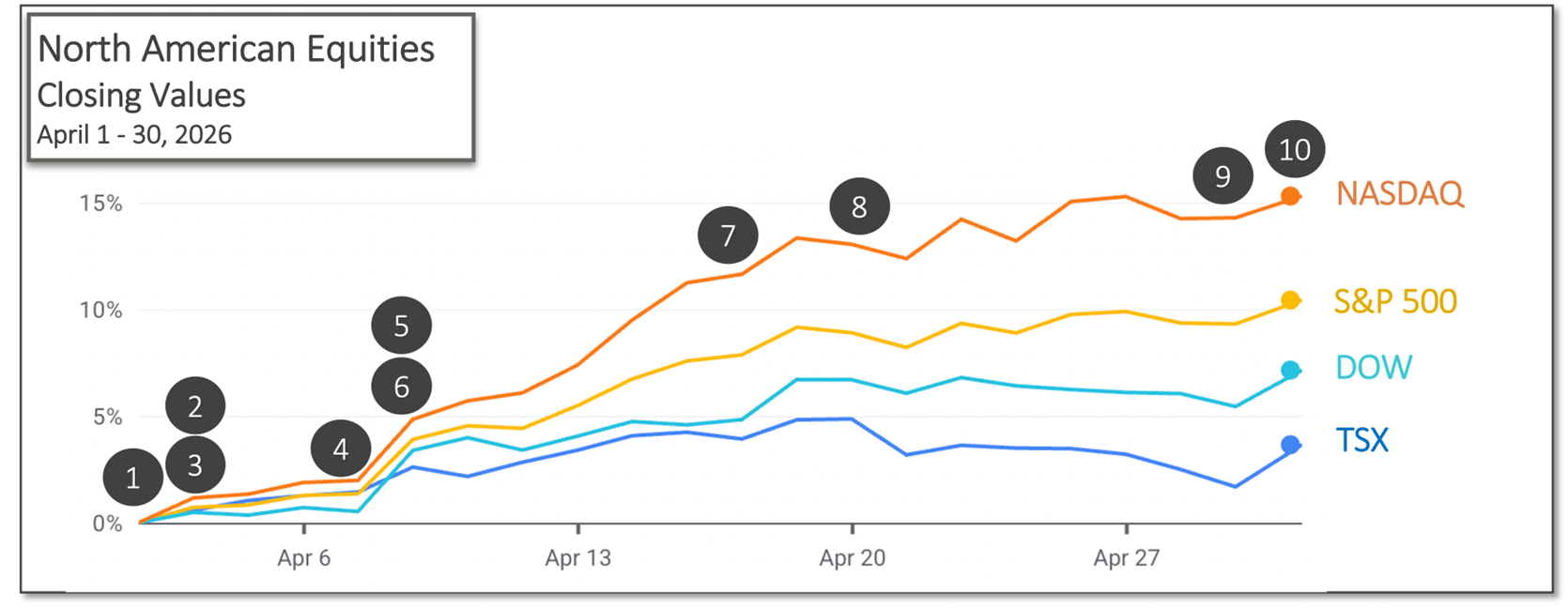

What happened in April?

Market performance in April occurred despite ongoing geopolitical uncertainty and elevated investor concerns surrounding global events. North American equity indexes rose between 3.5 per cent and 15 per cent during the month, bringing major U.S. indexes back into positive territory on a year-to-date basis. The TSX and NASDAQ both posted year-to-date gains of approximately 7.1 per cent.

Over the past year, returns across these major indexes have ranged from approximately 22 per cent to 42 per cent, representing strong performance despite periods of market volatility and uncertainty.

As markets advanced during April, volatility levels moderated compared to recent months, which can be an encouraging sign for investors. The VIX volatility index also declined during the month. VIX volatility index

(source: Bloomberg https://www.bloomberg.com/markets and ARG Inc. analysis)

Events that influenced markets in April included:

1. April 1 – Oil prices rose following comments on Iran

Comments from U.S. President Donald Trump regarding heightened tensions involving Iran contributed to increased volatility in energy markets. West Texas Intermediate (WTI) crude oil prices rose approximately 14 per cent following the announcement. Crude oil prices

2. April 2– Canada’s trade deficit widened

Canada’s merchandise trade deficit widened from $4.2 billion in January to $5.7 billion in February. Canada’s trade surplus with the U.S. narrowed to $1.7 billion in February from $4.9 billion in January. StatsCan release

3. April 2 – U.S. labour market showed improvement

The Bureau of Labor Statistics’ Employment Situation Summary reported that 178,000 jobs were added in March, following a decline of 133,000 jobs in February and exceeding analyst expectations. The unemployment rate changed little at 4.3 per cent. CNBC and jobs

4. April 9 – U.S. inflation remained above target

The U.S. Federal Reserve’s preferred inflation measure, the Personal Consumption Expenditures (PCE) price index, rose 2.8 per cent year-over-year, while Core PCE, which excludes food and energy, increased 3.0 per cent in February. PCE release CNBC and PCE

5. April 10– Canadian employment data improved modestly

The Canadian economy added approximately 14,000 jobs in March, representing an improvement from February’s loss of 84,000 jobs. Statistics Canada’s Labour Force Survey reported that the unemployment rate remained unchanged at 6.7 per cent. CBC and LFS

6. April 10 – U.S. inflation reflected higher energy prices

The Bureau of Labor Statistics reported that the Consumer Price Index (CPI) rose 0.9 per cent in March and 3.3 per cent year-over-year. Energy prices were a significant contributor to the increase, with gasoline prices rising 21.2 per cent during the month. BLS and CPI

7. April 17 – Progress in negotiations contributed to lower oil prices

Negotiations between the U.S. and Iran showed signs of progress, contributing to a decline in oil prices. Increased oil shipments through the Strait of Hormuz helped push oil prices below $84 per barrel, down approximately 25 per cent from early April highs.

8. April 20– Canadian inflation increased

Statistics Canada reported that the Consumer Price Index (CPI) increased 2.4 per cent year-over-year in March, up from 1.8 per cent in February. Higher gasoline prices were a major contributor to the increase.

9. April 29 – Central banks held rates unchanged

Canadian, American, and European institutions held their policy interest rates unchanged.

- The Bank of Canada maintained its target for the overnight rate at 2.25 per cent, with the Bank Rate at 2.50 per cent and the deposit rate at 2.20 per cent. BoC release

- The U.S. Federal Reserve maintained the federal funds target range at 3.5 to 3.75 per cent. Fed FOMC

- The European Central Bank maintained the interest rates on the deposit facility, the main refinancing operations and the marginal lending facility at 2.00 per cent, 2.15 per cent and 2.40 per cent respectively. ECB release

10. April 30 – U.S. GDP growth strengthened

U.S. Gross Domestic Product (GDP) grew at an annualized rate of 2.0 per cent in the first quarter of 2026. This represented an increase from the previous quarter’s 0.5 per cent growth rate, supported by increased government spending and stronger exports, despite moderating consumer spending. BEA GDP release

What’s ahead for May and beyond?

Central banks have indicated that recent increases in inflation may delay potential interest rate cuts. The Bank of Canada and the U.S. Federal Reserve are next scheduled to announce interest rate decisions on June 10 and June 17, respectively.

Geopolitical developments in the Middle East remain an important factor influencing energy markets, inflation expectations, and overall investor sentiment. Elevated oil prices could continue to place upward pressure on inflation if supply disruptions persist.