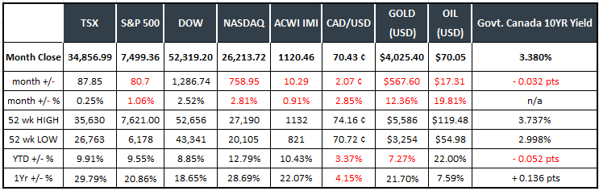

Last Month in the Markets: June 1 – 30, 2026 Index returns based on index value (source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis. Price returns are reflected)

Index returns based on index value (source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis. Price returns are reflected)

What happened in June?

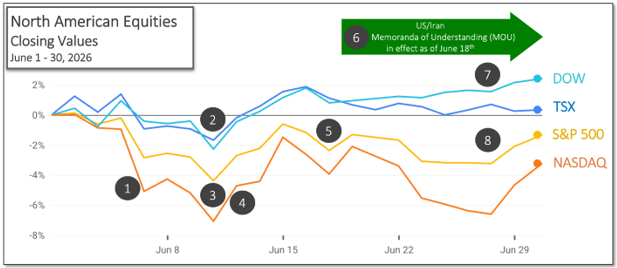

Geopolitical tensions in the Middle East remained a key influence on global markets during June. Developments involving the U.S., Iran, Israel, Gaza, and Lebanon contributed to periods of heightened uncertainty, particularly in energy markets. Concerns surrounding shipping through the Strait of Hormuz, a key global oil transit route, led to temporary increases in oil prices during the month. However, as tensions eased, oil prices retreated approximately 30 per cent from their June 3 intraday high, ending the month near where they finished in late February.

Against this backdrop, equity market performance was relatively muted. The TSX finished the month with little change, the S&P 500 declined approximately 1 per cent, the Dow gained 2.5 per cent, and the NASDAQ posted a modest decline. While June itself produced mixed results, it followed a particularly strong second quarter. As a result, major North American equity indexes remained well ahead for both the quarter and the first half of 2026, despite ongoing geopolitical uncertainty and evolving expectations for interest rates.

What’s ahead for July and beyond?

The future of the Canada-United States-Mexico Agreement (CUSMA) remains an important area of focus following recent comments from U.S. officials regarding North American trade policy. Bilateral discussions continue as Canada, the United States, and Mexico evaluate potential paths forward, and developments may have implications for trade, business investment, and economic growth.

Geopolitical developments in the Middle East are also expected to remain an important influence on energy markets, inflation expectations, and investor sentiment. Although crude oil prices have largely returned to pre-conflict levels, elevated energy costs may continue to work their way through supply chains and inflation data over the coming months.

As always, investors will continue to monitor economic fundamentals, including inflation, employment, interest rates, GDP growth, and corporate earnings, alongside geopolitical developments, all of which have the potential to influence market performance.

Events that influenced markets in June included: (source: Bloomberg https://www.bloomberg.com/marketsand ARG Inc. analysis)

(source: Bloomberg https://www.bloomberg.com/marketsand ARG Inc. analysis)

1. June 5 – Canadian and U.S. employment growth strengthened

Canadian employment increased by 88,000 and the unemployment rate fell by 0.3 percentage points to 6.6 per cent. This was the strongest monthly employment gain since November 2025, with full-time employment increasing by 154,000 positions in May. CBC and LFS StatsCan’s Labour Force Survey

According to the Bureau of Labor Statistics’ Employment Situation Summary, nonfarm payroll employment increased by 172,000 and the unemployment rate was unchanged at 4.3 per cent. Job gains were concentrated in leisure and hospitality, local government, and health care, while employment in financial activities declined.

Stronger employment data generally reflects economic resilience but may also influence expectations for future interest rate decisions, particularly if labour market strength contributes to ongoing inflationary pressures. CNBC and jobs and rates

2. June 10 – Bank of Canada held rates unchanged

The Bank of Canada maintained its policy interest rate at 2.25 per cent. The Bank noted that employment growth has been uneven while inflation has increased alongside higher energy prices. Ongoing trade discussions and tariffs also remain factors influencing the economic outlook and future monetary policy decisions. BoC release CBC and BoC

3. June 10 – U.S. inflation continued to trend higher

U.S. consumer inflation continued to trend higher during May. According to the Bureau of Labor Statistics, the Consumer Price Index (CPI) increased 0.5 per cent on a seasonally adjusted basis following a 0.6 per cent increase in April. On a year-over-year basis, the all-items index increased 4.2 per cent, up from 2.8 per cent in April. Energy prices increased 3.9 per cent during May and accounted for a significant portion of the monthly increase. CNBC and CPI

U.S. producer prices also continued to rise. The Producer Price Index increased 6.5 per cent year over year in May, representing the largest annual increase since November 2022. BLS and PPI

4. June 11 – European Central Bank raised policy rates

In response to rising inflation in the Eurozone, the European Central Bank raised its three benchmark rates by 0.25 percentage points. The Bank reiterated its objective of maintaining inflation at approximately 2 per cent over the medium term, consistent with the goals of many major central banks. ECB rate hike

5. June 17 – Federal Reserve maintained policy rates

The U.S. Federal Reserve Chair Kevin Warsh announced that the federal funds target range would remain at 3.5 to 3.75 per cent. This marked his first interest rate announcement and accompanying press conference as Chair. Fed announcement

Alongside its decision, the U.S. Federal Reserve released an updated Summary of Economic Projections (SEP), which included higher inflation projections and removed the anticipated rate cut from this year’s “dot plot.” While the decision to leave rates unchanged was widely expected, the updated projections provided additional insight into the U.S. Federal Reserve’s evolving outlook for inflation and monetary policy.

Committee members remain divided regarding the future path of interest rates, reflecting continued uncertainty surrounding inflation and broader economic conditions.

6. June 18 – United States and Iran announced a Memorandum of Understanding

Following several days of negotiations, the United States and Iran announced a Memorandum of Understanding intended to reduce hostilities over the following 60 days. BBC and MOU

7. June 22 – Canadian inflation moved above 3 per cent

Canada’s Consumer Price Index increased 3.2 per cent year over year in May, up from 2.8 per cent in April. This represented the highest annual inflation rate since late 2023. Gasoline prices increased more than 33 per cent over the past year and were a significant contributor to the higher inflation reading. StatsCan CPI release CBC and CPI

8. June 25 – Canadian employment and wages continued to grow

Canadian payroll employment increased by 22,000 in April and was up 78,100 positions compared to one year earlier. Job vacancies remained near 500,000. Average weekly earnings increased 1.0 per cent during April to $1,346 and were 3.8 per cent higher than one year earlier. StatsCan release

9. June 25 – U.S. inflation moved above 4 per cent while import prices continued to rise

The U.S. Federal Reserve’s preferred inflation measure, the Personal Consumption Expenditures (PCE) Price Index, increased 0.4 per cent in May and 4.1 per cent over the previous 12 months. Core PCE, which excludes food and energy prices, increased 3.4 per cent year over year. PCE release CNBC and PCE

U.S. import prices rose 1.9 per cent during May following increases of 2.0 per cent in April and 0.9 per cent in March. Compared to one year earlier, import prices increased 6.7 per cent, the largest annual increase since August 2022. Imported fuel prices rose 12.5 per cent during May and have increased 47.0 per cent since February. IPI release