Last Month in the Markets: May 1 – 29, 2026

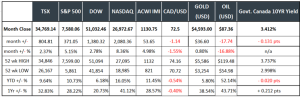

Index returns based on index value (source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis. Price returns are reflected)

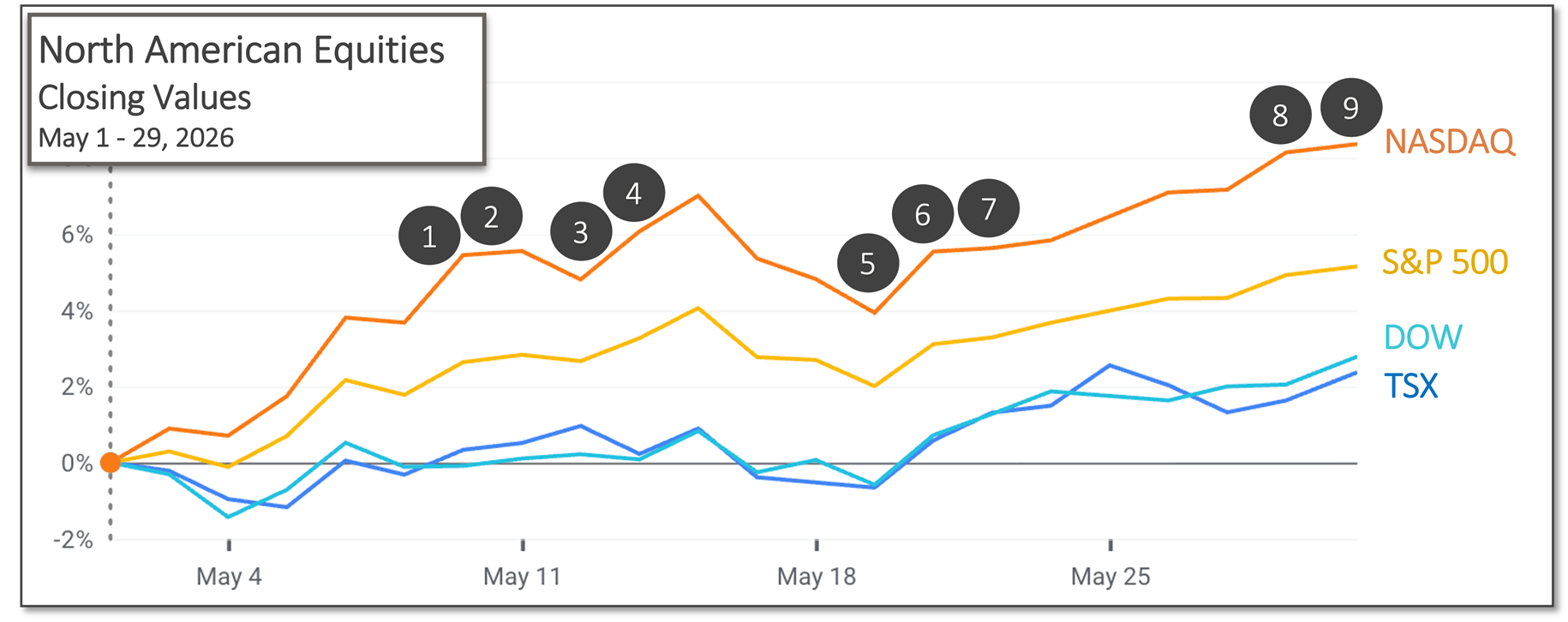

What happened in May?

Just prior to the start of May, the Bank of Canada, the U.S. Federal Reserve, and the European Central Bank all maintained their policy interest rates as inflationary pressures associated with higher energy prices continued to emerge. Markets have generally been anticipating potential interest rate reductions, and higher interest rates can create headwinds for economic growth and equity markets. Despite this backdrop, equity markets delivered strong gains during the month.

Investor optimism surrounding a potential easing of tensions in the Middle East contributed to stronger North American equity market performance. During the final two weeks of May, oil prices declined approximately 17 percent while major equity indexes reached new record highs. Strong first-quarter earnings results from many S&P 500 companies also supported market performance.

Gold and oil prices moved in opposite directions as negotiations related to Middle East tensions progressed. Expectations for increased oil shipments through the Strait of Hormuz contributed to a decline of approximately $18 USD per barrel in benchmark oil prices during the final two weeks of May.

What’s ahead for June and beyond?

Central banks have indicated that recent increases in inflation may delay potential interest rate cuts. The Bank of Canada and the Federal Reserve are next scheduled to announce interest rate decisions on June 10 and June 17, respectively.

Geopolitical developments in the Middle East remain an important factor influencing energy markets, inflation expectations, and overall investor sentiment. Elevated oil prices could continue to place upward pressure on inflation if supply disruptions persist.

Close attention to the U.S./Iran war and its effect on global oil prices, local inflation and interest rates will provide a measure of understanding for the trajectory of equity portfolios. On June 1, Iran suspended negotiations with the U.S. based on cease-fire violations and Israel’s continued attacks on Lebanon. Iran has vowed to fully block the Strait of Hormuz. Immediately following Iran’s announcement, the price of oil jumped 7 percent. It is unlikely that any further negotiations will be straightforward and will likely lead to additional volatility in markets.

Events that influenced markets in May included:

(source: Bloomberg https://www.bloomberg.com/markets and ARG Inc. analysis)

1. May 8 – S&P 500 delivered strong revenue and earnings growth

Much of the increasing value of the S&P 500 can be attributed to a solid earnings season. 89 percent of companies have reported, and 84 percent of them have reported a positive earnings-per-share surprise and 80 percent have reported a positive revenue surprise. Compared to one year ago, the blended earnings growth rate is 27.7 percent, the highest growth rate for quarterly earnings in nearly five years. FactSet Earnings Insight

2. May 8 – U.S. employment increased and Canadian jobs declined

American nonfarm employment moved up by 115,000 in April and the unemployment rate was unchanged at 4.3 percent. It was only the second consecutive monthly increase over the last year. “Job gains occurred in health care, transportation and warehousing, and retail trade. Federal government employment continued to decline” according to the Employment Situation Summary.

Canadian employment and the employment rate fell slightly in April. The economy lost 18,000 jobs, and the employment rate dropped 0.1 percent to 60.5 percent. In March, 14,000 jobs were added, however 112,000 jobs have been lost so far in 2026. The unemployment rate rose 0.2 percent to 6.9 percent. Full-time employment fell 47,000, while part-time employment edged up by 29,000. StatsCan release CBC and jobs

3. May 12 – U.S. inflation grew almost 4 percent over the last year

After rising 0.9 percent in March, the U.S. Consumer Price Index (CPI) rose again in April by 0.6 percent. Nearly half of the increase in month-to-month inflation is attributed to the rising price of energy. Over the last 12 months, the all-items index increased 3.8 percent. The year-over-year inflation rate in March was 3.3 percent. The energy index increased 17.9 percent for the 12 months ending April, and the food index has increased 3.2 percent over the last year. BLS release CNBC and CPI

4. May 13 – Bank of Canada highlighted risks related to tariffs and geopolitical developments

The Bank of Canada released its Summary of deliberations from its interest rate announcement of April 29 when it left interest rates unchanged. Broadly, the Bank highlighted geopolitical developments and energy prices as factors that could influence inflation, economic growth, and employment trends. The Summary of deliberations noted that the outlook for growth and inflation remains highly dependent on developments in global trade and energy markets. The “outlook for growth and inflation in Canada was highly conditional on US tariffs remaining unchanged and on lower oil prices, which would depend on developments in the war in the Middle East.”

5. May 13 – U.S. producer inflation continued to increase

The U.S. Producer Price Index (PPI), representing wholesale, not consumer prices, rose 1.4 percent in April, up from a 0.7 percent increase in March. On a year-over-year basis the PPI rose 6.0 percent, the largest increase since December 2022. BLS PPI release

6. May 19 – Canadian consumer prices moved further above target

Canada’s Consumer Price Index (CPI) increased 2.8 percent on a year-over-year basis in April, up from March’s increase of 2.4 percent. Energy prices, which have risen 19.2 percent over the past year, drove much of the increase. Additionally, one year ago, the consumer carbon tax was removed, and as of April that effect no longer reduces the result of the consumer inflation calculation. When gasoline is excluded, the CPI rose 2.0 percent in April, down from 2.2 percent in March. StatsCan CPI release

7. May 20 – Fed released its meeting minutes from latest “hold”

The Federal Reserve released meeting minutes from its interest rate decision of April 29. Committee members discussed maintaining rates at their current levels longer than previous predictions and suggested that raising rates may be necessary if inflation remains above its 2 percent target. Equity markets remained resilient despite discussion of a potentially longer period of restrictive monetary policy. Fed minutes

8. May 21 – Magnificent 7 remained significant contributors to S&P 500 performance

Much of the performance success of the S&P 500 can be attributed to the Magnificent 7 (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla) who reported earnings growth of 63.2 percent in the first quarter versus 17.4 percent for the other 493 companies. The Magnificent 7 comprise only about 35 percent of the market capitalization of the S&P 500 but continue to remain a significant contributor to overall index performance. FactSet Earnings Insight Mag 7 market cap

9. May 28 – U.S. consumer inflation continued to increase

U.S. consumer inflation continued to trend higher according to the Federal Reserve’s preferred inflation indicator, the Personal Consumption Expenditures (PCE) price index. In April, the index increased 0.4 percent, excluding food and energy. Core PCE rose 0.2 percent. For the same month one year ago, the PCE price index increased 3.8 percent. Excluding food and energy, the PCE rose 3.3 percent compared to one year ago. Consumer inflation was last at this year-over-year level in November 2023. BEA PCE release CNBC and PCE

10. May 28– American GDP slowed after revised estimate

For the first quarter of this year, the advance estimate for Gross Domestic Product (GDP) has been revised downward to an annual growth rate of 1.6 percent. BEA GDP release

11. May 29 – Canadian GDP reflects continued economic softness

Canadian Gross Domestic Product (GDP) remained near the threshold commonly associated with a technical recession, defined as two consecutive quarters of declining economic growth. In the first quarter of 2026, GDP declined 0.1 percent following a 1.0 percent annualized contraction in the fourth quarter of 2025. CBC and GDP