Germany’s Synthetic Fuel Miracle

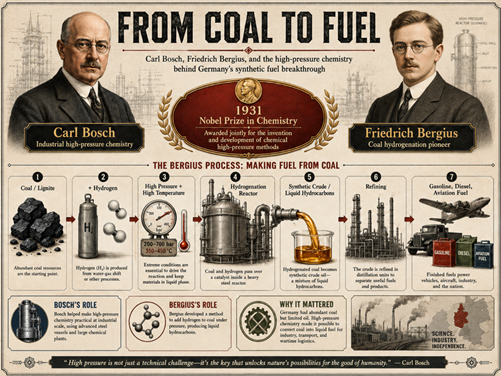

Germany had no oil, but it had coal. Ingeniously, its chemists learned to squeeze gasoline out of stone. Twenty-eight-year-old Friedrich Bergius used high pressure to wring liquid fuel from crushed brown coal. Carl Bosch, the engineer who had already built the factories that turn air into fertilizer and feed half the world, scaled it into a full plant. What marvels: liquid from rock, fertilizer from thin air. No wonder the two shared the Nobel Prize in Chemistry in 1931.

source: ChatGPT

Here’s the enduring lesson: humanity applies ingenuity and capital to overcome scarcity, and the world grows richer for it. With few exceptions, that is the entire story of economic history.

Why the Oil Crisis Never Became a Catastrophe

Markets are relearning that lesson now in the Strait of Hormuz. Remember the forecasts—global recession, famine and $200 crude? A fifth of the world’s liquefied gas went offline and a fifth of its oil had nowhere to sail. The experts swore the market was underpricing the catastrophe.

With peace pending, West Texas crude round-tripped from a $118 spike to $76 in under three months. Wood Mackenzie (one of the best in the business) put $200 oil on the table as a worst case possibility in late May. Jeff Currie, first called for $200 oil in 2008 while with Goldman Sachs. Now with Abaxx, he has been warning about “tank bottoms” and the disconnect between price and supply. How did they get it so wrong—or did they?

source: ChatGPT

The Market’s Oldest Lesson: Supply Responds

The truth is they didn’t get it wrong—at the G7 President Donald Trump himself confirmed that the strategic reserves would be functionally empty in four weeks. He warned that “bedlam” would have ensued. Early analysis of the terms of the deal he signed at Versailles favours the idea that Trump (and the world) needed the deal more than Iran. So the better read here is that oil analysts were right to warn of the impending disaster and that Trump pulled back rather than risk those forecasts coming true. This outcome was always the base case.

Let’s be clear, it may be too early to declare the Iran War resolved and the Strait of Hormuz re-opened. Increasingly though, it looks like economics 101 prevailed: cheap supply, racing toward a price that had risen too far. It is the force that, eighty years ago, buried Bergius’s miracle.

By 1940, the Luftwaffe flew on fuel squeezed from coal. Miraculous as it was, Bergius’s synthetic fuel lacked the high octane that American AV Gas provided the RAF. The Battle of Britain was won by imported, higher octane and more abundant fuel. That battle foreshadowed synthetic fuel’s own demise. As the war ended and the Persian Gulf opened, crude came ashore at two dollars a barrel—and the miracle was abandoned overnight. History has a way of repeating.

source: ChatGPT

The Shortages That Still Matter

If a cheaper barrel could bury a fuel that powered a war machine, OPEC quotas could cap a panic. And they did. While the commentariat warned the rebuild would take years, investors capped West Texas at $118 and Brent near $126—never near $200. OPEC+ lifted quotas, the UAE pumped, the U.S. drained its reserves, and China (the largest importer) simply declined to buy. Qatar says much of its capacity is back within weeks. The shortage summoned its own cure, right on schedule. What’s the lesson for investors?

Bet on abundance: over any horizon that matters, supply comes and the shortage breaks. But the gap between the expert predictions and the price is the opportunity—and the lesson isn’t to dismiss every shortage. While one lasts, prices rise and capital is drawn in. The challenge for investors is to find the shortages that persist, where real excess demand is genuinely limited by supply. Let’s look at some that we’ve talked about before: copper, rare earth metals, Bitcoin and AI compute.

Copper’s cure comes slowly, throttled by decade-long mine lead times. Rare earth metals are similar shortages that will require years of investment (and gov’t support) to remedy. Their persistent shortage is the opportunity. The two worth dwelling on are stranger: the shortage that can never be cured, and the one we are choosing not to.

Bitcoin: Scarcity That Can’t Be Solved

Bitcoin is the shortage that can never be solved. Bitcoin breaks the pattern we’ve been discussing. Supply is fixed at twenty-one million, enforced by its own code; no amount of capital or genius will mint the twenty-one-million-and-first coin. Bergius wrung oil from rock; but no one will ever wring another Bitcoin from anything. It is the anti–synthetic fuel: scarcity that ingenuity can’t defeat. Now, scarcity alone doesn’t guarantee higher prices. That requires demand to bid prices higher. Lately Bitcoin bulls have been patiently waiting for demand to return. If history holds, the bulls patience will be rewarded this fall.

AI Compute: The Bottleneck Investors Are Watching

AI compute is a purer and more persistent supply shortage. Demand for AI is near-unlimited; chip supply is throttled to a trickle. The twist is that the throttle is a choice of one company. Taiwan Semiconductor (TSMC) could flood the market and kill prices. They have seen bubbles and are actively managing only incremental supply increases to prevent the inevitable bust. If they doubled output, Nvidia could sell $1.5 trillion more chips. They won’t. That discipline is what is preventing a bubble in the near term.

So what’s the takeaway? How does an engineered shortage align with a long-term bet on abundance. TSMC is acting like OPEC, throttling supply to attempt to keep prices high indefinitely. History teaches this effort is probably doomed to failure. Follow the money as capital flows to solve for the shortage.

Following Capital to the Next Opportunity

SpaceX’s IPO is exhibit A. While controversial, Elon Musk is one of the geniuses of our day. He has plans to solve the AI compute shortage by end-running TSMC and building Terafab; a vertically integrated semiconductor facility which targets the leading edge TSMC owns today. On June 12th, SpaceX completed the largest IPO in history: ~$75 billion raised at a $2 trillion valuation, with captive demand baked in through newly-absorbed xAI. Capital is flooding the bottleneck, exactly as the abundance thesis predicts. Like all shortages, AI compute is a race against time. TSMC is still in charge—for now. Betting on abundance requires acknowledging timing. For investors that’s the opportunity.

source: ChatGPT

Why Timing Matters More Than Scarcity

Abundance is the destination, not the trade. The money is made in the meantime—in shortages real enough to draw capital and stubborn enough to resist it for years. Copper and rare earths take years to cure; Bitcoin’s can’t be cured at all; AI compute’s won’t be, until TSMC decides otherwise or Terafab rewrites the script. Each is a bet on how long the cure is delayed, not whether it arrives.

That’s the discipline: rent the shortage, don’t marry it. Ride it while demand outruns supply, and never mistake a long delay for a permanent reprieve. Bergius proved both halves of the law—he wrung oil from rock, then watched a two-dollar barrel bury his miracle the moment the chokehold lifted. TSMC’s chokehold won’t hold if Musk is successful with Terafab. The crisis is never permanent. The only question that ever pays is when.

Glen